- PE 150

- Posts

- Consumer PE Down 68% Since Peak — What Comes Next

Consumer PE Down 68% Since Peak — What Comes Next

This week we're breaking down where real asymmetric edge actually comes from in private equity.

Good morning, ! This week we're breaking down where real asymmetric edge actually comes from in private equity (and why infrastructure keeps winning), the great consumer reset reshaping dealmaking post-2021, how secondaries are evolving into core portfolio infrastructure—not just a liquidity outlet, and the macro ripple effects of an energy-driven shock on PE underwriting and capital allocation.

Juniper Square helps PE GPs deliver a modern investor experience without giving up operational control — combining purpose-built software and fund administration services in one connected model. As investor expectations rise and fund structures grow more complex, firms need fewer handoffs, fewer failure points, and a stronger system of record behind every LP interaction. Book a demo →

DATA DIVE

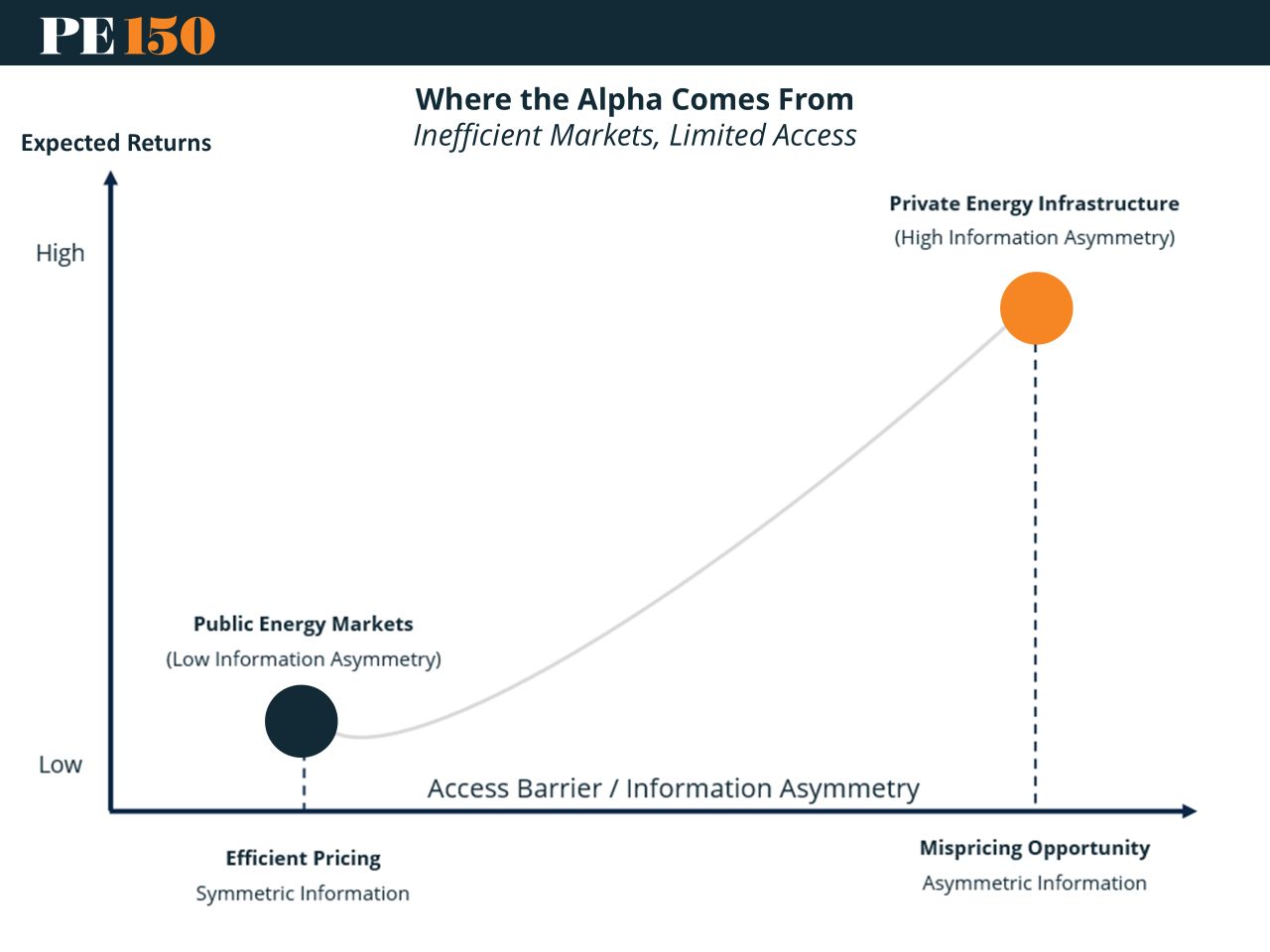

The Anatomy of Asymmetry

Private equity loves the word “asymmetric.” Most use it loosely. This framework sharpens it.

There are five layers where real edge compounds: Structural, Informational, Time Horizon, Complexity, and Behavioral. Miss one, and you’re just buying beta with better branding.

Structural sets the payoff (limited downside, open upside). Informational separates insiders from tourists. Time Horizon rewards those willing to sit still while others churn. Complexity filters out lazy capital. And Behavioral—arguably the hardest—ensures you don’t sabotage your own thesis.

Why it matters: when all five align, returns don’t add—they multiply.

The punchline: infrastructure (especially energy) checks all five boxes. Which helps explain why sponsors keep showing up… even when it’s hard, slow, and deeply unsexy.

TREND TO WATCH

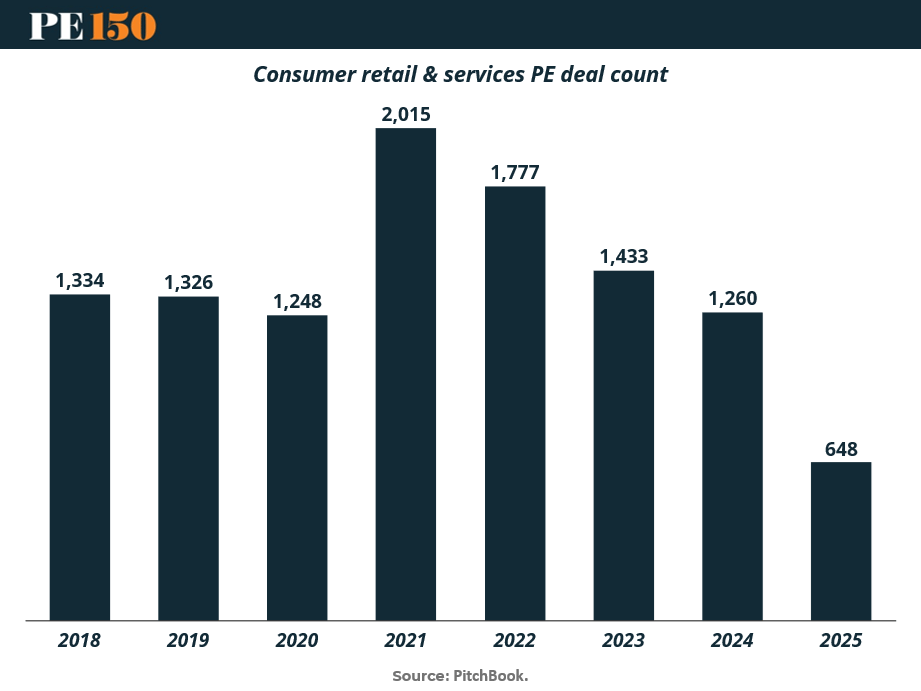

The Great Consumer Reset

Consumer PE isn’t bouncing back — it’s resetting. After a frothy peak of 2,015 deals in 2021, activity has slid to 1,260 in 2024, with 2025 tracking ~648. That’s not a dip; it’s a rewrite.

What changed? Start with the obvious: higher cost of capital has crushed the leverage playbook. Add demand volatility in discretionary spending and persistent exit bottlenecks, and suddenly yesterday’s growth stories look…optimistic.

The twist: capital hasn’t left — it’s gotten picky. Sponsors are crowding into defensive subsectors, leaning into operational value creation, and targeting smaller control deals where pricing finally makes sense.

The bottom line: this is less comeback, more recalibration. The winners won’t be the firms that scaled fastest in 2021 — but those that can underwrite durability and execute in a world where financial engineering no longer does the heavy lifting. (More)

PRESENTED BY JUNIPER SQUARE

Stop adding more tools or service providers. Get the best of both with a fund operations partner.

The LP experience can make or break fundraising because investors remember how it feels to work with your firm: onboarding, responsiveness, reporting, and the confidence they have in the numbers.

That experience is only as strong as the operating model behind it. When fund and investor data live across disconnected systems, delays and inconsistencies show up fast.

Juniper Square is the fund operations partner for PE GPs, combining software + fund administration services built on a common data foundation. That means fewer failure points, clearer visibility across investor workflows, and a modern investor experience powered by a single source of truth.

Book a demo to see how a fund operations partner

COMPLIANCE CORNER

Intensifying SEC Focus on Conflicts of Interest in Private Equity

The SEC's enforcement on conflicts of interest involving general partners, their funds, and portfolio companies is more stringent than ever. Private equity firms face a complex landscape of disclosure, governance, valuation, fee allocation, and transaction oversight requirements amid heightened scrutiny. Recent SEC actions reflect zero tolerance for undisclosed or mismanaged conflicts, especially regarding fee offsets, affiliated transactions, and valuation methods.

Conflicts of interest affect many areas in private equity—from management fees and expense allocation to co-investments and portfolio company transactions. Missteps or unclear disclosures risk substantial enforcement penalties, reputational harm, and loss of LP trust.

Key 2025 shifts include updated supervisory guidance for registered closed-end funds of private funds (CE-FOPFs) stressing strong conflict disclosures and board oversight. Certain investment caps are lifted, but transparency requirements increase.

In summary, conflicts management can no longer be a back-office function. Robust, documented conflicts protocols integrated into investment and portfolio management must lead. Investing in compliance programs, disclosures aligned with evolving regulations, and proactive regulator engagement on issues is crucial for survival and success in today's regulatory environment. (More)

MACROVIEW

Energy Shock Reshapes the Macro Outlook

The escalation in the Middle East has triggered a classic energy-driven supply shock, pushing oil and gas prices higher while unsettling global markets. Unlike past crises, the global economy enters this episode with more anchored inflation and tighter monetary policy, reducing the risk of a 1970s-style spiral—but not eliminating it.

Central banks are now navigating a sharper trade-off: higher inflation versus weaker growth. The likely outcome is a prolonged pause in rate cuts rather than renewed tightening, with bond markets already pricing in a higher-for-longer environment. Rising yields are tightening financial conditions and could weigh on investment and housing.

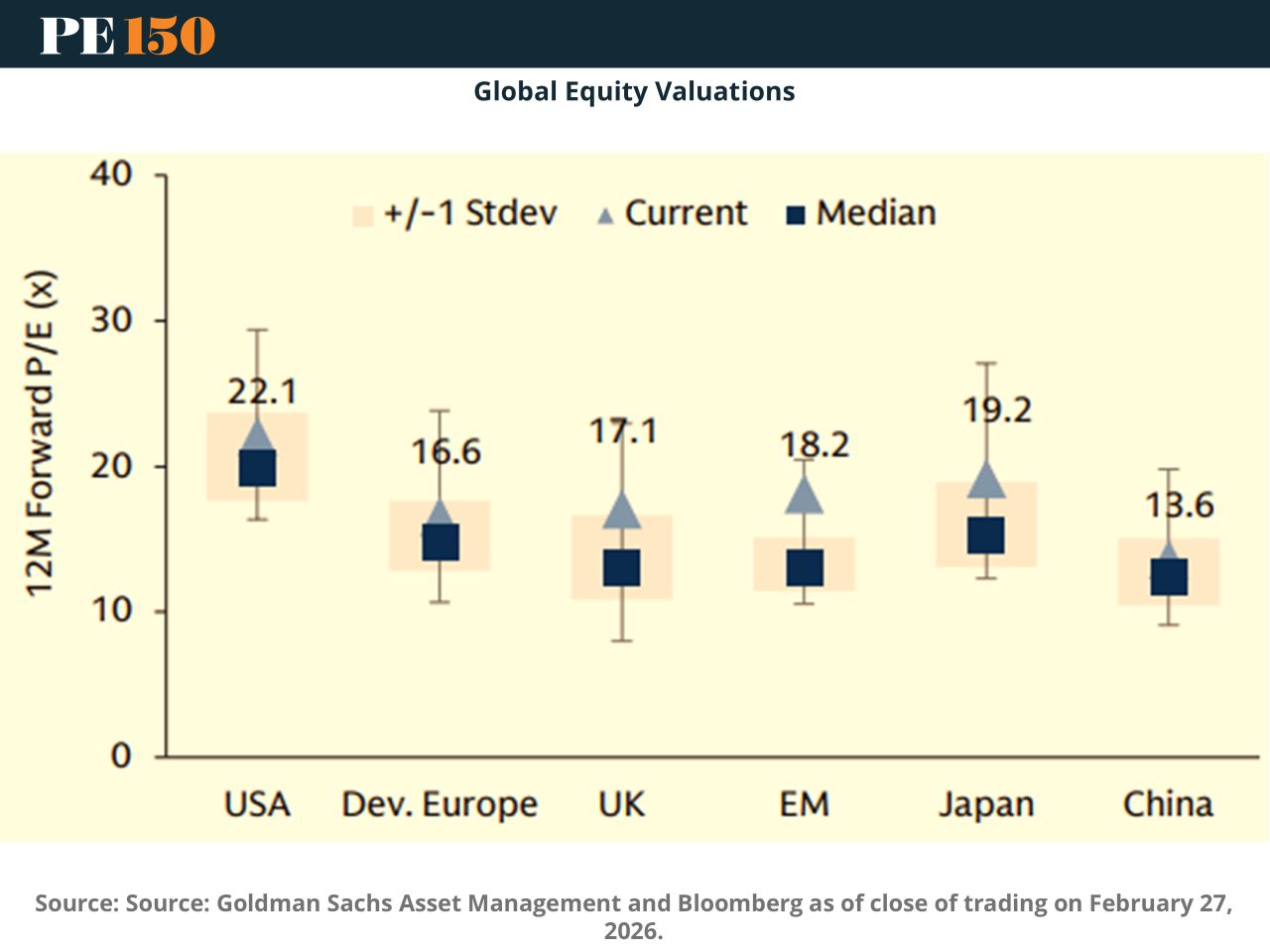

Meanwhile, regional divergence is widening. Energy exporters appear more resilient, while Europe and Asia face greater exposure to imported costs. Equity markets reflect this split, with valuation gaps likely to matter more in a riskier macro regime.

The key variable remains duration: a short shock is manageable; a prolonged one risks broader stagflationary pressure. (More)

LIQUIDITY CORNER

Secondaries Go From Outlet to Operating System

Liquidity stress is no longer cyclical. It is structural. Large LPs that once relied on time as a buffer are now actively engineering outcomes. Even historically patient institutions are using secondaries as a “pressure valve” as distributions slow, holding periods stretch, and exit visibility deteriorates

The shift is not just about cash. It is about control. LPs are using secondaries to rebalance exposure across vintages, reduce concentration risk, and reposition portfolios into more attractive entry points. In parallel, transaction timelines have compressed to a matter of days, forcing investors to price assets with imperfect and fragmented data

The strategic takeaway

Secondaries are no longer a fallback for distressed sellers. They are becoming core portfolio infrastructure. GPs that treat them as optional liquidity tools risk falling behind LPs who now view them as a primary mechanism for pacing, pricing, and portfolio construction in an unpredictable exit environment (More)

See how PE GPs deliver a modern investor experience with a connected operating model. Book a demo →

"Innovation distinguishes between a leader and a follower"

Steve Jobs