- PE 150

- Posts

- Private Equity Exits in 2025: Navigating Uncertainty with Strategic Flexibility

Private Equity Exits in 2025: Navigating Uncertainty with Strategic Flexibility

How evolving liquidity tools, longer holds, and operational excellence are reshaping the modern exit landscape

I. Introduction: The Exit Market Regains Its Footing

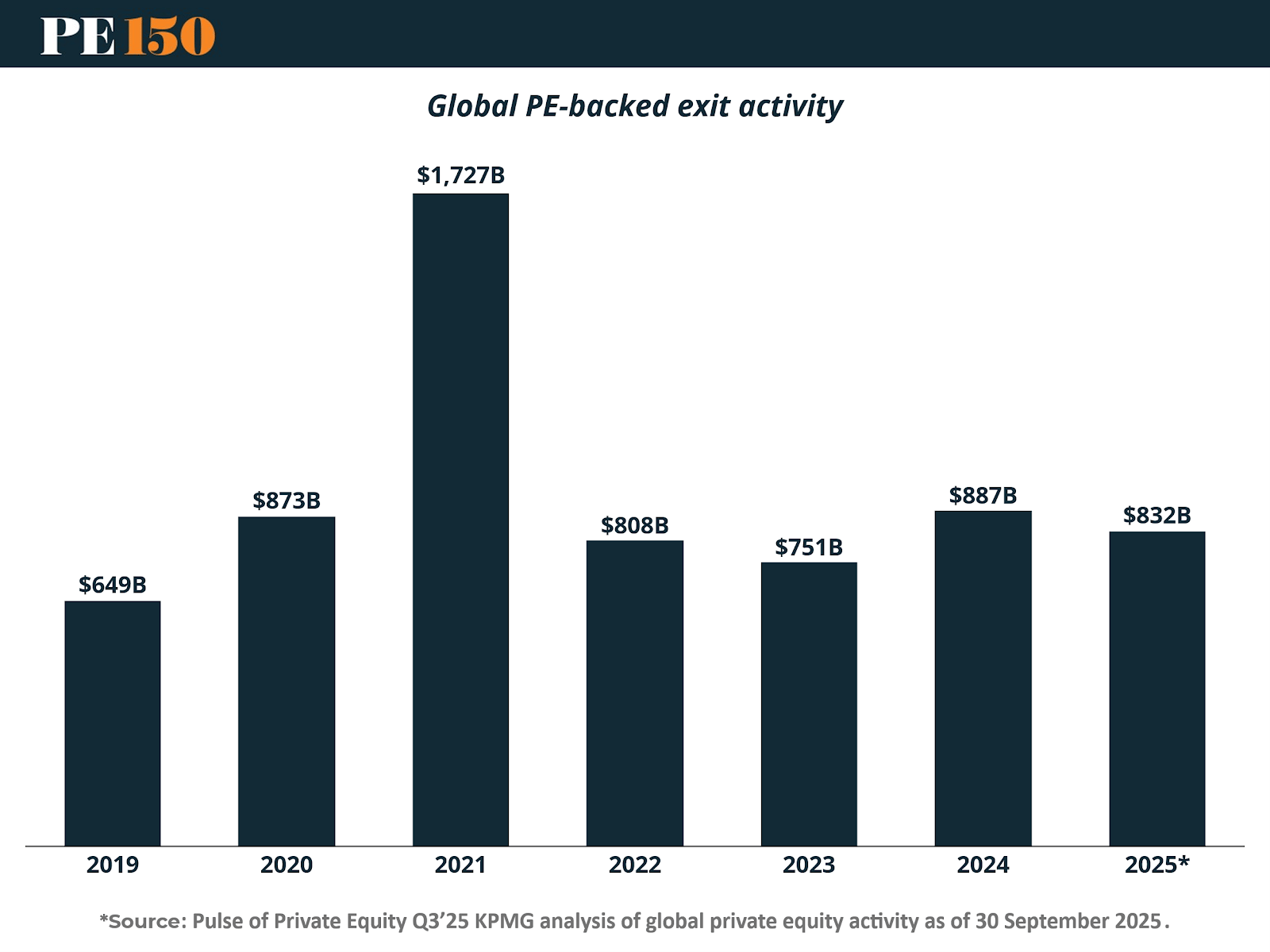

After two years of contraction, the private equity exit market is showing its first signs of stabilization. As the chart below illustrates, global PE-backed exits are set to surpass 2024 levels, reaching an estimated $832 billion in 2025—a modest but meaningful recovery from the trough of 2023. While still well below the record-breaking $1.7 trillion peak in 2021, this rebound signals a gradual reopening of liquidity channels and renewed buyer confidence in select sectors.

The recovery, however, remains uneven. Trade sales continue to dominate, driven by strategic acquirers seeking growth through consolidation, while public listings remain largely constrained by volatile valuations and persistent macro uncertainty. Many sponsors are pursuing partial realizations or structured liquidity rather than full exits, balancing the need for distributions with the desire to preserve upside in quality assets.

The forces shaping this shift are both cyclical and structural. A slower pace of interest rate cuts, diverging regional growth trajectories, and ongoing geopolitical friction continue to weigh on valuation multiples. At the same time, the return of M&A appetite from corporates and financial sponsors has begun to reanimate the exit landscape—albeit selectively and at more disciplined price levels.

Despite these headwinds, the amount of capital still waiting on the sidelines remains immense. With over $2.6 trillion in global dry powder, sponsors are under pressure to deliver realizations and reset fund cycles. This tension—between abundant capital and constrained exit routes—has pushed the industry to innovate around liquidity. Continuation funds, NAV financing, and minority recaps have emerged as mainstream tools, blurring the line between exit and ownership.

In this environment, the definition of success is evolving. For many firms, it’s no longer just about achieving the highest multiple or fastest close—it’s about timing, credibility, and creativity. The firms that thrive in 2025 will be those that can engineer liquidity without compromising long-term value, treating exits as a continuum rather than a finish line.

This report explores how that evolution is taking shape—where exit activity is re-emerging, how sponsors are rethinking timing and readiness, and which innovative strategies are setting the tone for the next cycle of private equity liquidity.

II. Anatomy of the Rebound: What’s Driving the Recovery

As EY’s Pete Witte noted during our expert discussion, “we’ve had a number of false starts. Deployment has accelerated, but exit momentum has been choppy.” This helps explain why the market’s recovery is visible, but not yet fully institutionalized.

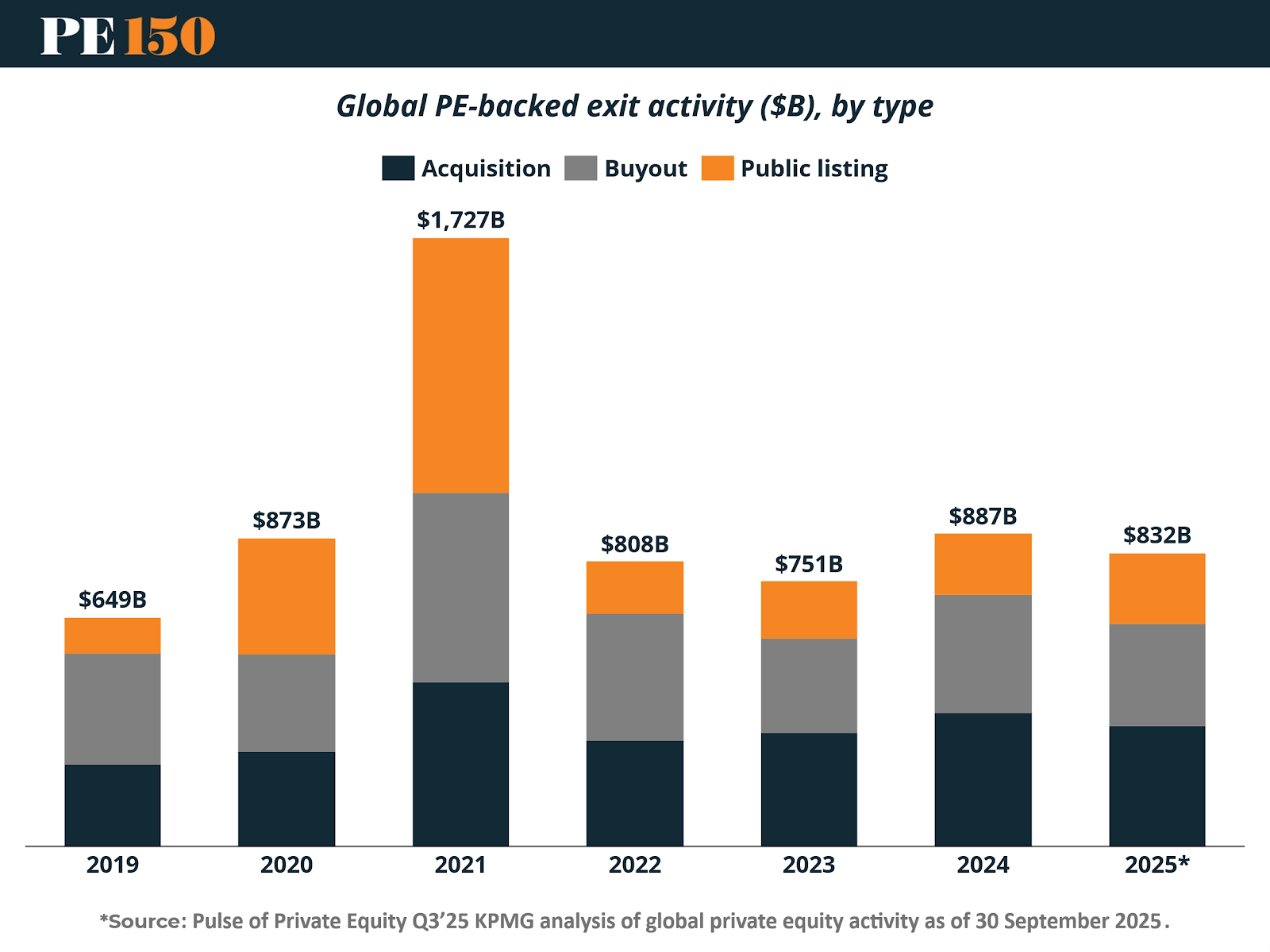

The return of exit activity in 2025 is not just about higher totals—it’s about where that recovery is coming from. As shown in the chart below, acquisitions and sponsor-to-sponsor transactions now make up the bulk of private equity exit value, with public listings remaining a small slice of the market.

The composition of exits underscores a deeper structural shift in how liquidity is achieved. Strategic acquisitions and secondary buyouts have taken center stage, supported by healthier corporate balance sheets and record levels of undeployed private capital. In contrast, public listings have yet to re-emerge as a viable path, constrained by volatile equity markets and valuation uncertainty. The brief post-pandemic boom in IPOs during 2021—when exit values reached nearly $1.7 trillion—has given way to a far more selective environment.

Witte also cautioned that the recovery remains fragile:

“We need to see how the next three to six months unfold before there’s conviction behind a sustained recovery.”

What’s driving this pattern is a pragmatic recalibration rather than exuberant recovery. Corporates are prioritizing synergy-driven M&A, often targeting proven assets with predictable cash flows. Sponsors, meanwhile, are leaning on each other for liquidity—recycling assets through secondary buyouts, continuation vehicles, and structured exits that preserve exposure while delivering partial realizations.

This evolving mix of exit types reflects a broader normalization of the market. The age of quick flips and IPO-fueled windfalls has been replaced by one of disciplined execution, creative structuring, and longer hold periods. As one senior dealmaker put it, “Liquidity today is engineered, not discovered.”

While total exit value is projected to reach roughly $830 billion in 2025, that figure masks a more nuanced truth: the market is active again, but in different ways. The recovery is being led not by risk-on exuberance, but by strategic recalibration—private equity’s version of patient capital in motion.

III. The 2025 Deal Landscape: Where the Biggest Exits Are Happening

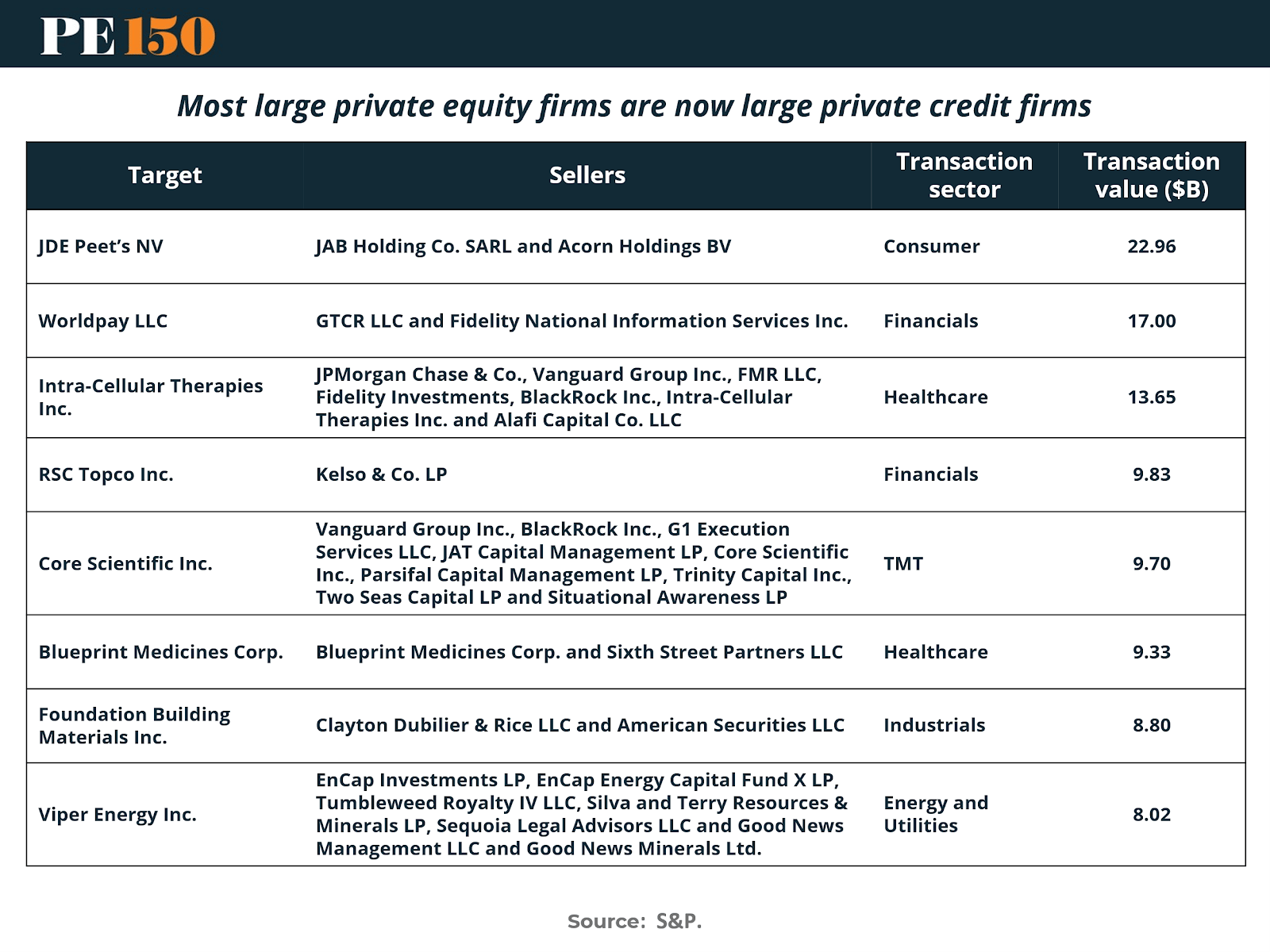

The rebound in private equity exits in 2025 has been driven by a handful of high-profile transactions that underscore where liquidity is returning first. As the table below highlights, the largest completed exits of the year span a diverse range of sectors—from consumer and financials to healthcare and energy—reflecting a gradual normalization of deal flow across the market.

The top deal so far, JDE Peet’s NV’s $22.9 billion sale, marked a significant consumer-sector transaction and signaled renewed appetite for established branded assets with defensible cash flows. In financials, Worldpay’s $17 billion sale to GTCR and Fidelity National Information Services reinforced the attractiveness of payments infrastructure and technology-enabled financial services—areas where sponsors continue to see structural growth.

Healthcare has also remained a standout. Transactions such as Intra-Cellular Therapies ($13.7 billion) and Blueprint Medicines ($9.3 billion) demonstrate sustained investor confidence in biopharma innovation, despite broader valuation volatility. Similarly, Core Scientific’s $9.7 billion exit in the technology and digital infrastructure segment reflects rising sponsor focus on AI-related compute capacity and energy efficiency—two themes increasingly shaping deal pipelines.

Importantly, the diversity of sectors represented—consumer, financials, healthcare, industrials, and energy—suggests that the recovery is not narrowly concentrated. Instead, it points to selective optimism where fundamentals remain resilient and capital intensity supports long-term growth narratives.

While these headline deals illustrate the top end of the market, they also reflect broader trends shaping 2025 exits:

Scale and defensibility matter — acquirers are prioritizing resilient EBITDA and stable margins.

Sponsor syndication remains high — many transactions involve multi-investor exits, reflecting shared ownership structures across fund vintages.

Sector rotation is underway — investors are shifting from pure tech growth stories to real-asset and infrastructure-adjacent opportunities.

Together, these transactions provide a snapshot of the re-emerging liquidity landscape—one still cautious, but increasingly active where fundamentals align.

IV. Exit Strategies in Flux: What’s Most Attractive Now?

With IPO windows still largely shut and valuations swinging between optimism and caution, private equity sponsors are rethinking how best to exit portfolio companies.

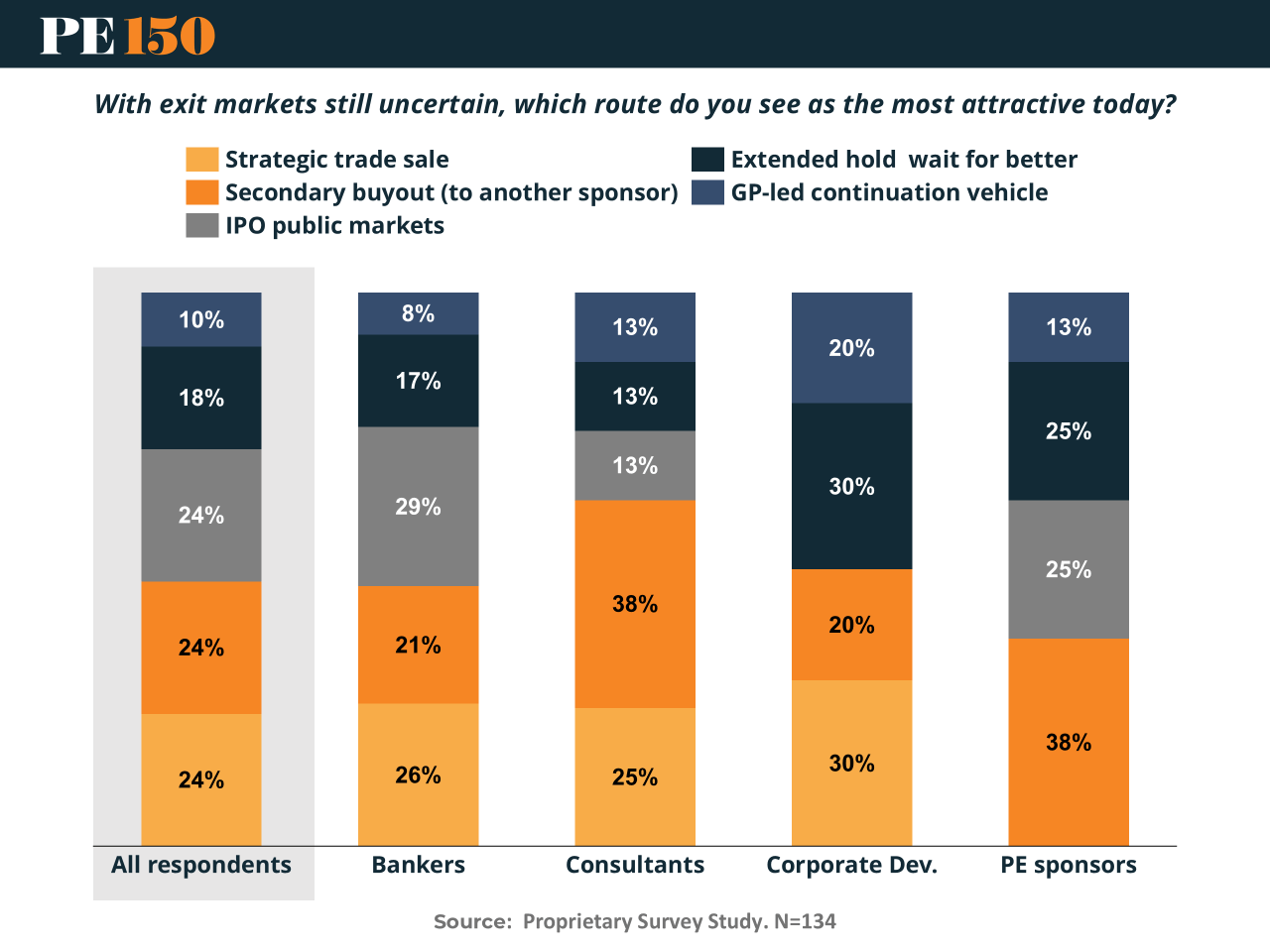

According to one of our microsurveys in this round, conducted among 134 market participants spanning bankers, consultants, corporate development teams, and PE sponsors, sentiment is sharply divided in today’s uncertain environment.

The headline finding: there is no single “go-to” exit path right now. The data show an unusually even split across options, underscoring the lack of a clear, dominant route.

Secondary buyouts (sales to another sponsor) and strategic trade sales tied for the top spot among all respondents, each at 24%. Both routes reflect a market leaning on sponsor-to-sponsor deal flow and on corporate buyers still willing to pay for synergies, even amid mixed valuations.

According to Peter Witte, buyer behavior has shifted in a notable way:

“Corporates are acting with more confidence, even with uncertainty still elevated. Both PE and strategics have realized uncertainty won’t go away, so they must move forward despite it.”

IPO / public markets also accounted for 24%, higher than expected given the slowdown—suggesting that some market participants still believe the IPO window could reopen selectively, especially for top-tier growth companies.

Extended holds (18%) and GP-led continuation vehicles (10%) represent smaller shares overall, though both continue to gain traction as sponsors look to avoid forced exits.

Looking deeper at the dynamics by group, PE sponsors stand out: nearly four in ten (38%) favor secondary buyouts, far ahead of any other option. This reflects the robust pipeline of dry powder across private equity, where funds remain eager to deploy capital—even if that means buying from fellow sponsors.

On the other side, corporate development executives lean more toward strategic sales (30%), reflecting corporates’ appetite for bolt-on acquisitions in sectors where growth is easier to buy than build.

The Bigger Picture

This fragmented set of preferences highlights a broader truth: exit markets are in transition. IPOs remain choppy, trade buyers are selective, and the rise of continuation funds shows GPs experimenting with new ways to retain control of prized assets.

Rather than one clear trend, the industry is operating in a multi-path era, where sponsors weigh all tools in the toolbox.

The real takeaway: flexibility is the new norm. For GPs, the ability to pivot between a secondary, a trade sale, or a continuation vehicle—depending on sector, buyer appetite, and capital needs—matters more than ever in 2025.

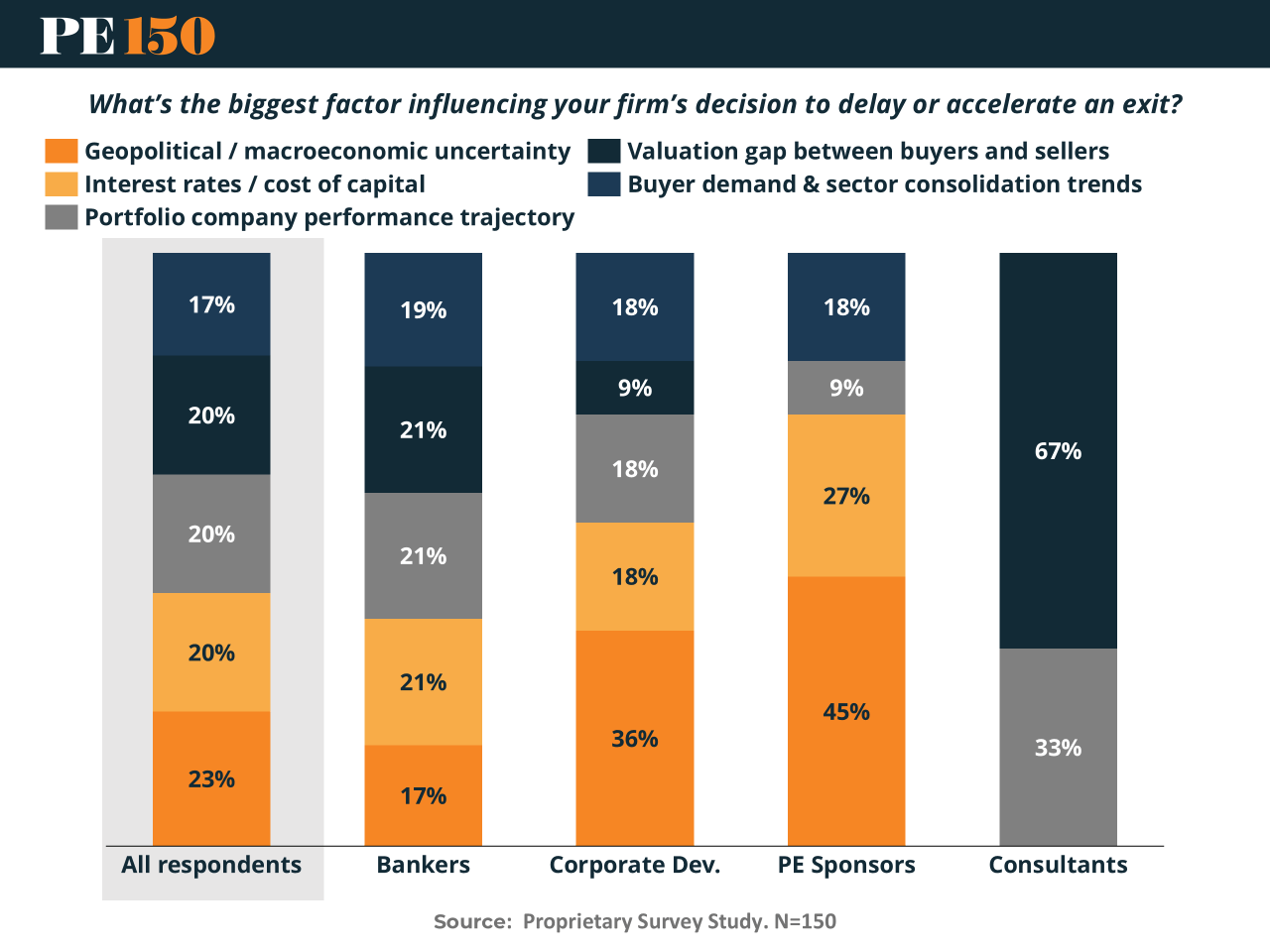

V. Timing the Exit: What’s Driving Hold vs. Sell Decisions

If the previous section addressed how firms are exiting, this one explores when. In today’s uncertain deal environment, timing an exit has become as strategic as the route itself.

Based on data from this round of microsurveys, there’s no single trigger shaping the sell-or-hold calculus, but the split across respondent groups reveals what each segment fears (or watches) most.

Across all respondents, the top influences are remarkably even: geopolitical and macroeconomic uncertainty (23%), interest rates / cost of capital (20%), and portfolio company performance trajectory (20%). That balance highlights how multiple headwinds, from capital costs to global volatility, are weighing equally on exit timing.

Sponsors vs. Strategics: Two Different Realities

For private equity sponsors, the picture is more concentrated. Nearly half (45%) cite macroeconomic uncertainty as the biggest factor influencing exit timing—a reflection of how tightly returns are linked to public market sentiment and debt conditions. Another 27% point to interest rates and capital costs, underscoring how higher financing costs continue to slow leverage-dependent transactions.

By contrast, corporate development teams are less macro-driven and more market-driven. 36% identify buyer demand and sector consolidation as their top influence, suggesting that strategic acquirers are timing exits—and acquisitions—around windows of competitive advantage rather than macro cycles.

Bankers remain evenly split, with roughly one-fifth selecting each factor—mirroring their role as intermediaries navigating between buyer appetite, sponsor timing, and valuation dynamics.

Consultants See a Clear Pattern

Consultants tend to take a more fundamental view: two-thirds (67%) cite portfolio company performance as the key determinant of exit timing. In a world where exit multiples are harder to defend, performance clarity and EBITDA resilience may matter more than external timing signals.

A Market in Wait Mode

The takeaway: the exit clock is still ticking—but more slowly.

For most firms, the “go” or “no-go” decision on a sale is a delicate balance between macro conditions, company-level performance, and market readiness.

While macro factors like rates and geopolitics dominate sponsor thinking, strategics and consultants are turning inward—focusing on execution quality, sector positioning, and buyer preparedness.

The message for 2025: timing is no longer about catching the market—it’s about controlling the controllables.

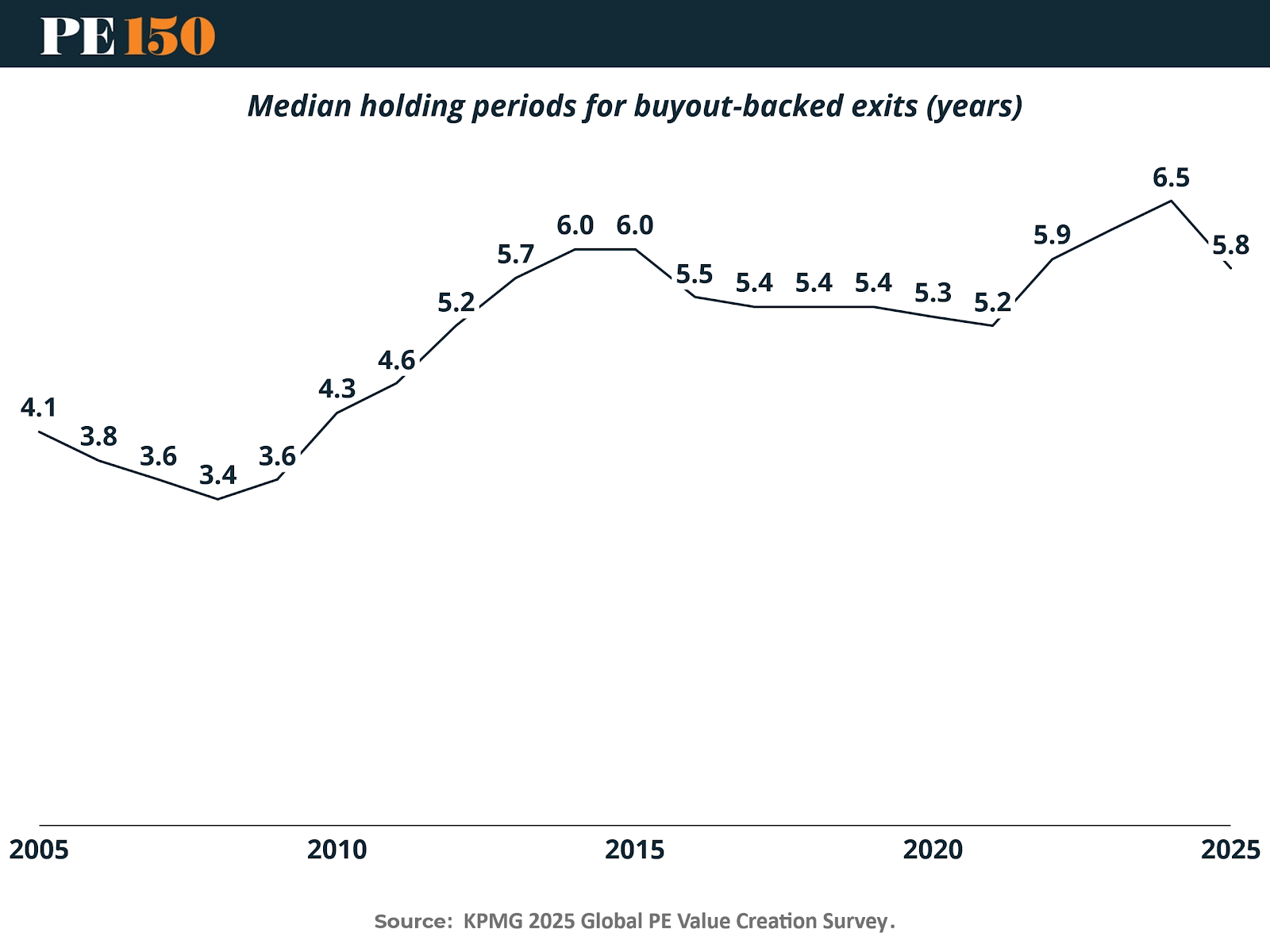

VI. Longer Holds, Shifting Playbooks: The Changing Nature of Exit Readiness

The lengthening of holding periods across private equity is more than a byproduct of market volatility—it’s a structural sign that the traditional value creation model no longer fits today’s exit environment.

Over the past decade, the median holding period for buyout-backed assets has risen from 3–4 years to nearly 6 years, as sponsors extend ownership to build sustainable performance stories and defensible valuations.

What’s behind the slowdown? Traditional levers like SG&A optimization, one-off cost reduction, and footprint expansion are delivering diminishing returns in a high-cost, low-growth world. As multiple expansion fades and geopolitical complexity rises, firms must now earn their exits operationally rather than financially.

This shift is reshaping exit readiness. PE firms are investing more heavily in data quality, AI-enabled performance analytics, and talent depth to demonstrate credible, repeatable value creation. According to market surveys, 70% of respondents plan to increase investment in operational AI by at least 25% in the next 12–18 months, while one in four firms now balance growth and efficiency equally when driving EBITDA improvement.

The result is that exits are taking longer—but becoming more robust.

As Witte emphasized, the challenge is concentrated in a specific cohort:

“The six-to-seven-year cohort is where the real friction is.”

Buyers are rewarding firms that can prove both resilience and scalability, not just financial engineering. The best-prepared exits in 2025 are emerging from sponsors who modernized their operating playbooks early—linking technology, governance, and human capital to long-term equity stories.

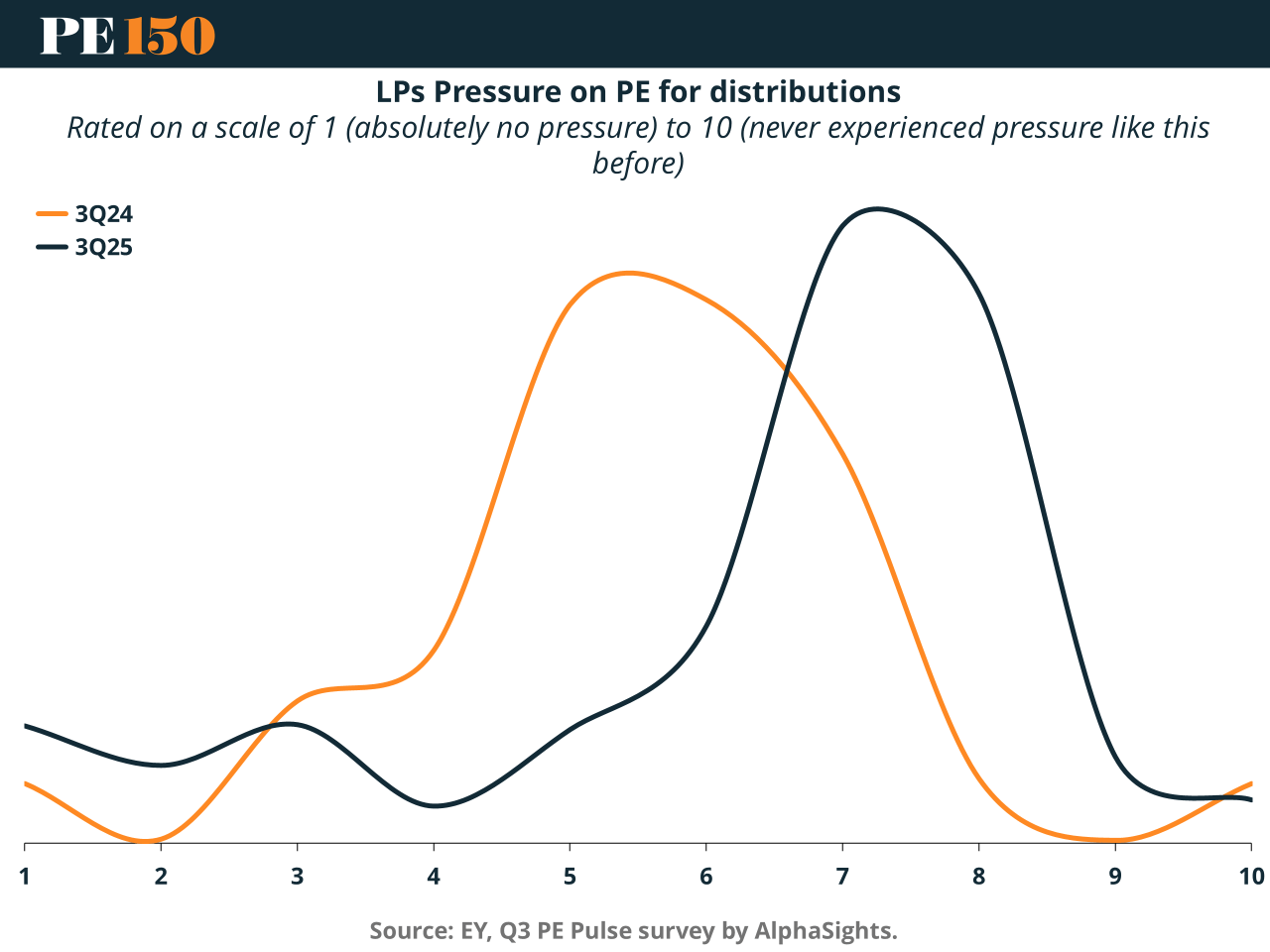

VII. Liquidity Stress Intensifies: LP Pressure and the Search for Alternatives

The extension of holding periods across the private equity landscape has not only redefined exit readiness—it has also created a growing liquidity strain throughout the ecosystem. As portfolio companies remain in funds for longer, capital recycling has slowed, leaving many general partners (GPs) balancing investor expectations against constrained exit options.

According to market data from S&P Global and EY, global PE firms are now holding assets for an average of nearly six years, with the US and Canada exceeding seven. The drivers are well known: high entry valuations from the pre-pandemic era, the sharp rate hikes of 2022–2024, and persistent valuation mismatches between buyers and sellers. The result has been a backlog of mature assets that are difficult to exit at target multiples—stretching fund life cycles and intensifying LP pressure for distributions.

Rising LP Pressure on Distributions

This pressure is becoming measurable. EY’s Peter Witte notes that over the past year, the proportion of GPs ranking LP pressure between six and eight on a ten-point scale has surged, reflecting mounting calls for liquidity. Institutional investors—pension funds, endowments, and sovereign wealth vehicles—are eager to recycle capital into new vintages after several years of limited realizations. While 2025 exit volumes are recovering, reaching roughly US$470 billion year-to-date (up 40% from 2024), they remain below the levels required to restore balance between deployments and distributions.

A partial reopening of the IPO window has offered some relief. More than US$18 billion in PE-backed IPO proceeds were raised in Q3 2025, led by healthcare and financial infrastructure names. Yet these transactions remain concentrated in a few resilient sectors, insufficient to offset the broader backlog of un-exited assets.

The Secondaries Market as a Pressure Valve

Against this backdrop, the private equity secondaries market has taken on new significance. With global secondaries dry powder surpassing US$220 billion, GP-led transactions—particularly continuation vehicles—have emerged as a pragmatic way to return liquidity to LPs without forcing discounted exits. Roughly US$155 billion in secondaries deals closed in 2024, and fundraising momentum has carried into 2025, with more than 200 active funds in market.

Witte framed this as part of a broader structural evolution:

“Secondary trading is the clear direction of travel. Many assets will live large parts of their lifecycle in the private markets.”

Even so, supply continues to exceed available capital. As S&P Global Market Intelligence observes, the secondaries market “has become an essential but insufficient outlet”—able to relieve only part of the liquidity tension. For many sponsors, the challenge is balancing the desire to maintain exposure to quality assets with the need to demonstrate cash returns.

EY’s latest survey results reinforce this reality:

“Half of firms would accept a 5–10% haircut, and a quarter would accept 10–20%.”

Valuation Gaps and Macro Headwinds

Macroeconomic conditions remain a key obstacle. Despite recent declines in base rates, the repricing of risk since 2022 has compressed expected returns and widened valuation gaps. Buyers are reluctant to meet sellers’ legacy pricing, while GPs resist markdowns that would erode performance metrics. Public-market volatility further limits large-scale exits, leaving the industry in a holding pattern until valuations realign.

Outlook: Gradual Thaw Ahead

Looking ahead, the remainder of 2025 may mark the beginning of a measured recovery in liquidity conditions. As inflation stabilizes and financing costs ease, sponsors are expected to regain confidence to transact—particularly in sectors with resilient cash flows and disciplined leverage. Meanwhile, secondaries activity will continue serving as a release valve, enabling LPs to rebalance and reinvest.

In this environment, liquidity is no longer assumed; it must be engineered. Through continuation vehicles, NAV financing, and creative recapitalizations, PE firms are adapting to a new normal—one defined not by quick exits, but by flexible, data-driven portfolio management.

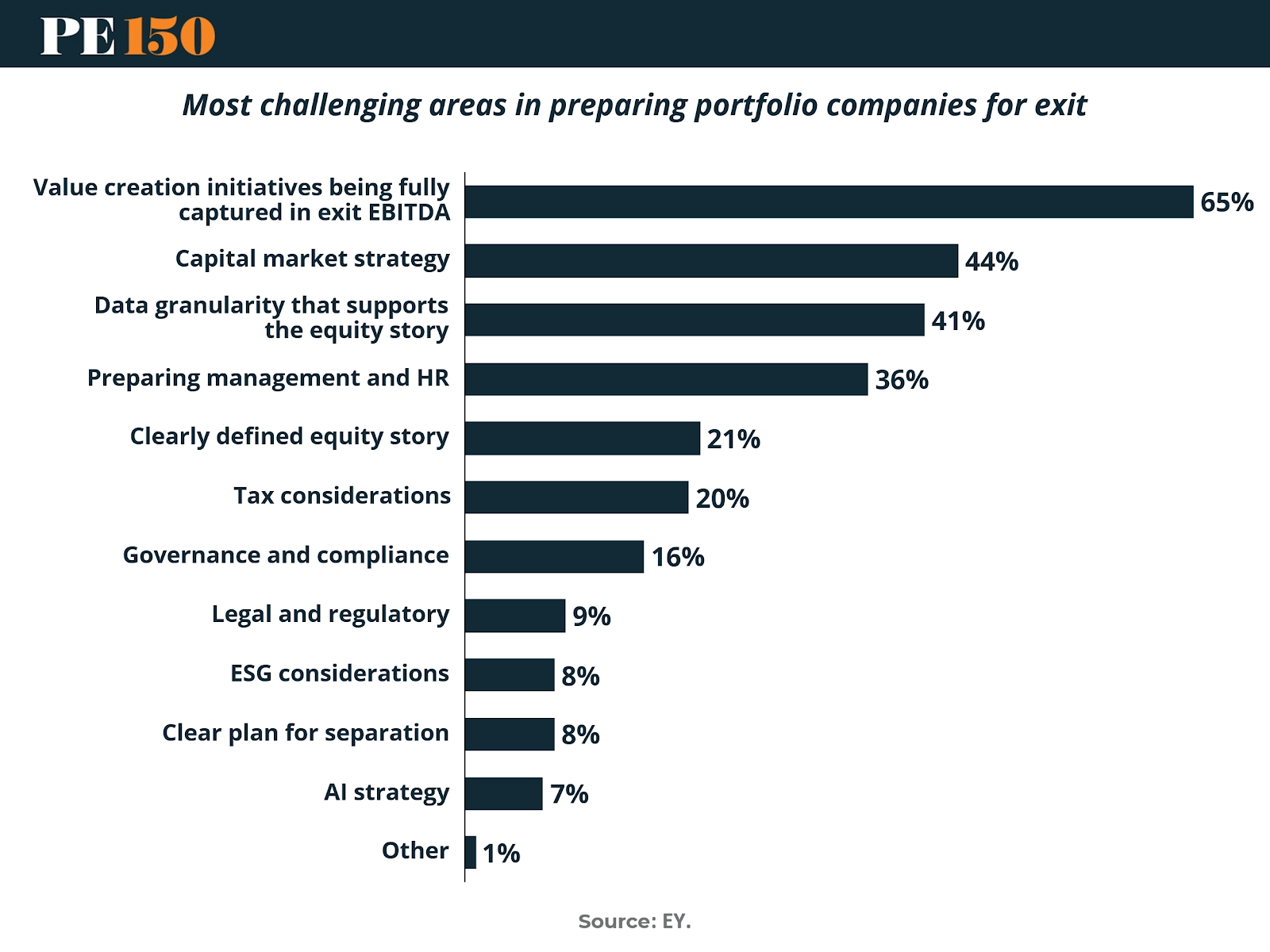

VIII. Critical Exit Challenges: Readiness Under Pressure

Even when market conditions align, many firms struggle with the fundamentals of exit readiness. According to data from EY’s 2025 Exit Readiness Survey, the most persistent roadblock lies in demonstrating and documenting value creation.

65% of respondents cited challenges in fully capturing value creation initiatives in exit EBITDA, making it the single largest obstacle to a successful sale. This finding underscores a critical truth: in today’s slower exit environment, where buyers are scrutinizing every assumption, credibility around financial uplift has become a make-or-break factor.

The next two hurdles reinforce the same theme. 44% of participants point to capital market strategy, reflecting how volatile conditions and shifting investor expectations have complicated valuation narratives. Meanwhile, 41% report insufficient data granularity to support their equity story — a gap that directly undermines buyer confidence and due diligence readiness.

The finance function is at the center of this challenge. Under heightened scrutiny from both sponsors and potential acquirers, finance teams are being pushed to deliver cleaner data, faster closes, and defensible performance metrics that align with the fund’s value creation thesis.

Talent and management readiness also feature prominently: 36% of respondents flagged preparing management and HR as a top-three challenge, highlighting the growing importance of leadership credibility and operational depth in exit valuation.

Secondary issues — from tax (20%) and governance (16%) to ESG (8%) and AI strategy (7%) — round out the picture of increasingly complex deal preparation requirements.

The message is clear: exit readiness is no longer just about timing or market windows—it’s about proving value, with precision and transparency. In an era where buyers have more leverage and data-driven diligence dominates, firms that can substantiate their equity story with granular, verifiable performance data will command the premium.

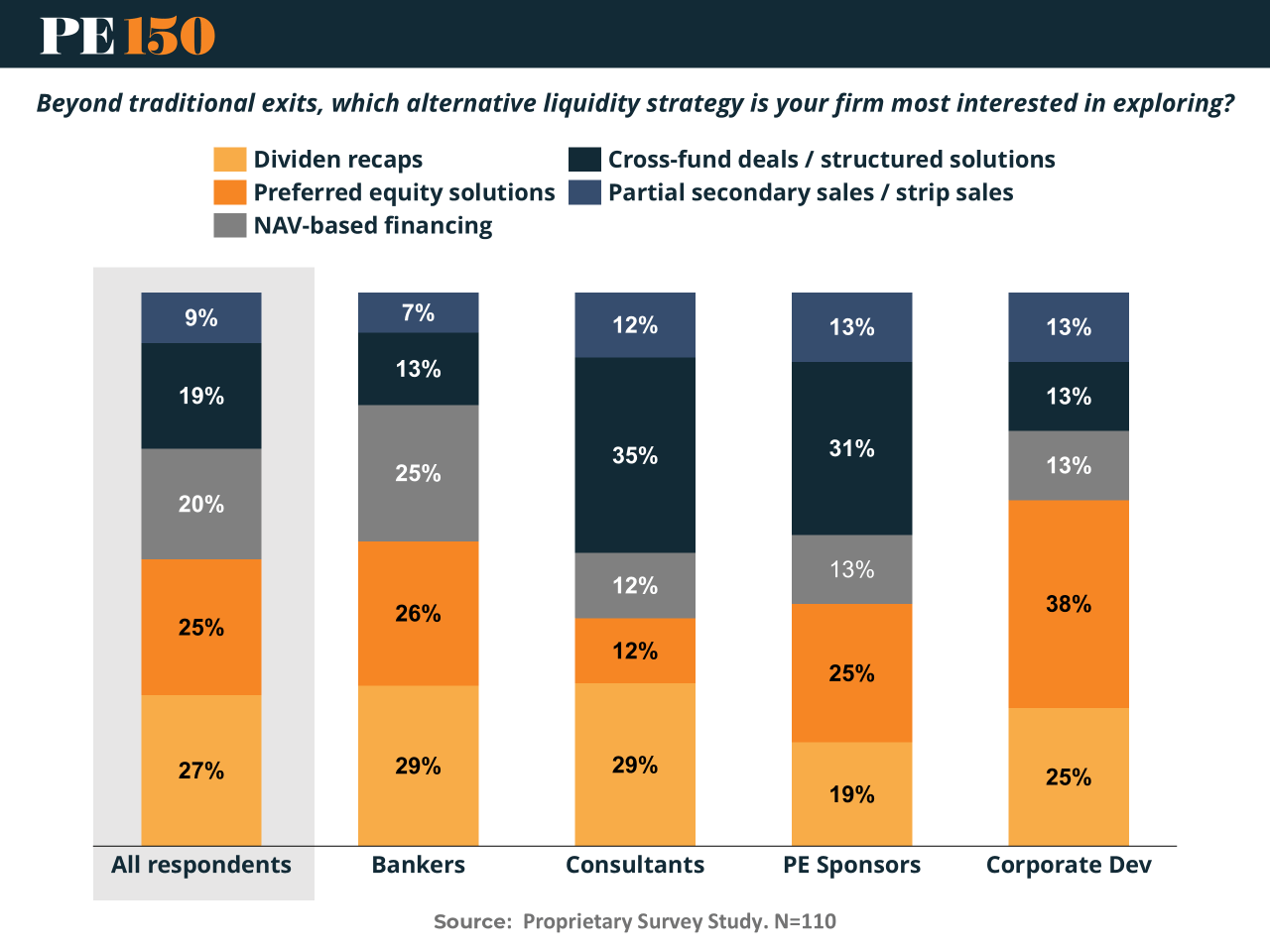

IX. When Traditional Paths Stall, Creative Liquidity Steps In

With exit markets still lagging their pre-2022 pace, firms are getting more creative in unlocking value without selling assets outright. Alternative liquidity tools—once niche—are quickly becoming mainstream instruments for maintaining momentum in stagnant markets.

The New Playbook for Liquidity

The landscape is fragmented, but dividend recapitalizations (27%) and preferred equity solutions (25%) lead the way. These mechanisms allow sponsors and corporates to extract value from portfolio companies without waiting for M&A or IPO conditions to improve.

NAV-based financing (20%), once a specialist instrument, has emerged as a credible third option. Firms now use fund-level NAV loans to extend holds, finance bolt-on acquisitions, or backstop distributions when LP pressure mounts.

However, Witte cautioned that these tools rarely disappear once adopted:

“Once these vehicles are introduced, they tend to become permanent features—even if their usage is cyclical.”

Structured and secondary strategies follow close behind—cross-fund deals (19%) and partial secondary or strip sales (9%)—illustrating a willingness to trade complexity for flexibility.

How Different Players See It

Bankers gravitate toward dividend recaps (29%) and preferred equity (26%), consistent with their role in arranging credit solutions.

Consultants report greater diversification: 35% cite cross-fund or structured deals as the most active area, reflecting growing advisory work in GP-led transactions and fund restructurings.

PE sponsors increasingly favor cross-fund deals (31%), using internal portfolio liquidity to extend ownership or seed continuation vehicles.

Corporate development teams prioritize preferred equity (38%), emphasizing capital flexibility over leverage-heavy solutions.

A Market Redefining “Exit”

The message is clear: liquidity is no longer synonymous with sale.

Between preferred equity, NAV financing, and continuation vehicles, firms are assembling an arsenal of interim liquidity levers to bridge the gap between uncertain exit markets and growing investor expectations.

What was once a toolkit for distressed situations has become a strategic liquidity stack—a defining feature of the modern PE cycle, allowing sponsors, corporates, and advisors alike to reshape timelines, optimize returns, and stay agile in a slower deal environment.

X. Conclusion: The Era of the Adaptive Exit

The story of 2025’s exit market is not one of revival or retreat—it’s one of reinvention. As traditional paths like IPOs and trade sales remain uneven, private equity and corporate players alike are proving that agility, not timing, now defines success. Exit strategies are fragmenting, timelines are stretching, and liquidity is being reimagined through creative mechanisms like preferred equity, NAV financing, and continuation vehicles.

Beneath the surface, a deeper transformation is unfolding. Firms are moving away from quick multiple expansion toward operational credibility—anchoring value in data integrity, performance resilience, and management depth. The best-prepared sellers are those who treat exit readiness as a continuous discipline, not a final step.

The market’s message is clear: in a cycle where macro volatility and capital costs blur the old playbook, flexibility has become the ultimate differentiator. The winners of this era won’t be those who exit first, but those who exit best—on their own terms, with evidence-backed value and a story buyers can trust.

Sources and References:

EY - What Can Private Equity Do Now to Finish Strong?

KPMG - Global Report on the Pulse of Private Equity, Q3 2025

KPMG - Value Creation in Private Equity: Five Capabilities for Achieving Operational Alpha

S&P Global Market Intelligence - Private Equity Exit Count Grew in Q3 as Transaction Sizes Shrank

S&P Global Market Intelligence - Private Equity Exits Tilted Toward Trade Sales in H1 2025

Premium Perks

Since you are an Executive Subscriber, you get access to all the full length reports our research team makes every week. Interested in learning all the hard data behind the article? If so, this report is just for you.

|