- PE 150

- Posts

- Energy Shock, Central Banks and the New Macro Regime

Energy Shock, Central Banks and the New Macro Regime

The conflict in the Middle East has introduced a fresh negative supply shock into an already unsettled global economy.

Gaston Brizuela Bosio

March 31, 2026 • Estimated Reading Time: 4 minutes

A supply shock meets a still-fragile global economy

The conflict in the Middle East has introduced a fresh negative supply shock into an already unsettled global economy. At the centre of the disruption lies energy: the interruption of flows through the Strait of Hormuz, attacks on gas infrastructure, and mounting logistical frictions across shipping and aviation have all tightened global commodity markets. The immediate result has been a rise in the price of oil, natural gas, jet fuel and a range of petrochemical byproducts. But the broader macroeconomic significance is not confined to energy alone. The shock is now feeding into inflation expectations, sovereign bond yields and the policy calculus of the world’s major central banks.

What makes the present episode especially consequential is that it arrives after half a decade of repeated disturbances: the pandemic, the Russia-Ukraine war, the tariff shock of 2025, and now a new energy and transport dislocation. Each shock has exposed the vulnerability of global supply chains, yet each has also shown that the world economy retains a notable capacity for adaptation. The question now is whether this latest disturbance remains a temporary relative-price shock or evolves into something more persistent and macroeconomically corrosive.

Why this shock is serious, but not a replay of the 1970s

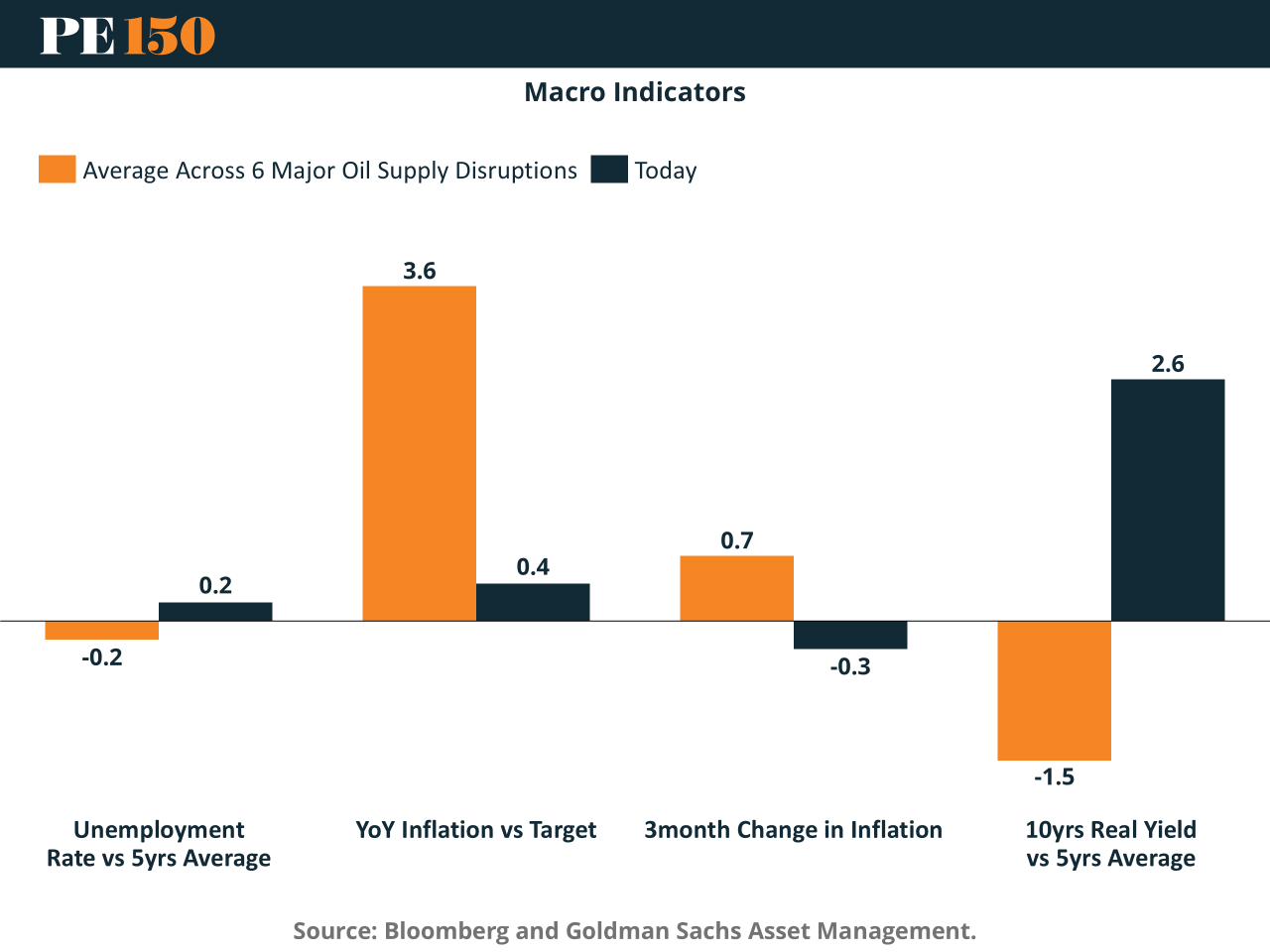

There are good reasons to resist simplistic comparisons with the 1970s oil crises. The global economy is materially less oil-intensive than it was then. Advanced economies use far less oil per unit of output, energy efficiency has improved markedly, and the production structure of many rich countries is now more service-oriented. In addition, several major economies entered this episode without the kind of wage-price spiral that characterised the 1970s.

The macro backdrop also appears more balanced than in previous oil-supply disruptions. Inflation, while still above target in several jurisdictions, had been moderating before the current shock. Labour markets, though not weak, no longer look as overheated as they did in the immediate post-pandemic period. At the same time, real interest rates are already restrictive rather than deeply negative. That matters. In earlier oil disruptions, policymakers often faced the shock with looser monetary settings and more visibly overheating economies. Today, they confront it with tighter policy and greater anti-inflation credibility.

Even so, the present shock remains dangerous. A sustained rise in energy prices operates like a tax on real incomes. It erodes household purchasing power, compresses margins for energy-intensive firms and raises costs across transport, chemicals, agriculture and manufacturing. In short, it weakens real demand even as it lifts headline inflation. That is the essence of a stagflationary impulse.

Central banks are forced into a harder trade-off

The world’s major central banks have responded with caution, holding policy rates steady while acknowledging greater uncertainty. That is unsurprising. Monetary authorities cannot produce more oil or reopen a shipping corridor. What they can do is prevent a temporary energy shock from becoming embedded in core inflation, wage settlements and medium-term inflation expectations.

For the Federal Reserve, the dilemma is especially delicate. Higher oil prices will push up headline inflation, but the US economy remains less exposed than Europe or Japan because America is a major producer of oil and gas. That reduces, though does not eliminate, the growth damage. Even so, bond markets have already adjusted to a higher-for-longer policy outlook. Investors increasingly suspect that the Fed will delay rate cuts rather than rush to cushion growth.

The European Central Bank faces a harsher trade-off. Europe is more exposed to imported energy costs, especially in gas markets, and therefore more vulnerable to an externally generated inflation shock. Yet tighter policy would compound the loss of household purchasing power and further weaken already soft growth. The Bank of England faces a similar problem, with the additional risk that energy-driven price increases bleed into domestic wage and price-setting behaviour. The Bank of Japan, meanwhile, must weigh imported inflation against the danger that tighter policy strengthens the yen only modestly while undermining activity.

The broad pattern is clear: central banks are not pivoting to renewed tightening yet, but the path to monetary easing has become much narrower.

Bond markets are signalling a regime shift

The response of government bond markets has been telling. Yields have risen sharply across the United States and Europe, reflecting not only higher expected inflation but also an increase in term premia and geopolitical risk compensation. This is a critical point. Markets are not merely repricing next month’s inflation print; they are reassessing the medium-term policy regime.

Higher long-dated yields tighten financial conditions in their own right. They raise mortgage costs, discourage business investment and put pressure on equity valuations. If sustained, that tightening could do part of the central banks’ work for them. But it also increases the risk that a supply-driven inflation shock is accompanied by a broader deterioration in domestic demand. What begins as an energy shock can therefore mutate into a more general macro slowdown.

China’s rebound may prove vulnerable

China offers a partial offset to the gloom. Recent data on retail sales, industrial production and fixed-asset investment suggest that the economy had begun to stabilise before the conflict intensified. That matters because firmer Chinese demand can lend support to global trade and manufacturing at a time when advanced economies are losing momentum.

Yet China is also highly exposed to imported energy costs. A prolonged rise in oil and gas prices would raise production costs, squeeze exporters and complicate Beijing’s effort to engineer a durable recovery. The improvement in activity may therefore prove real but fragile.

Valuations still leave room for differentiation

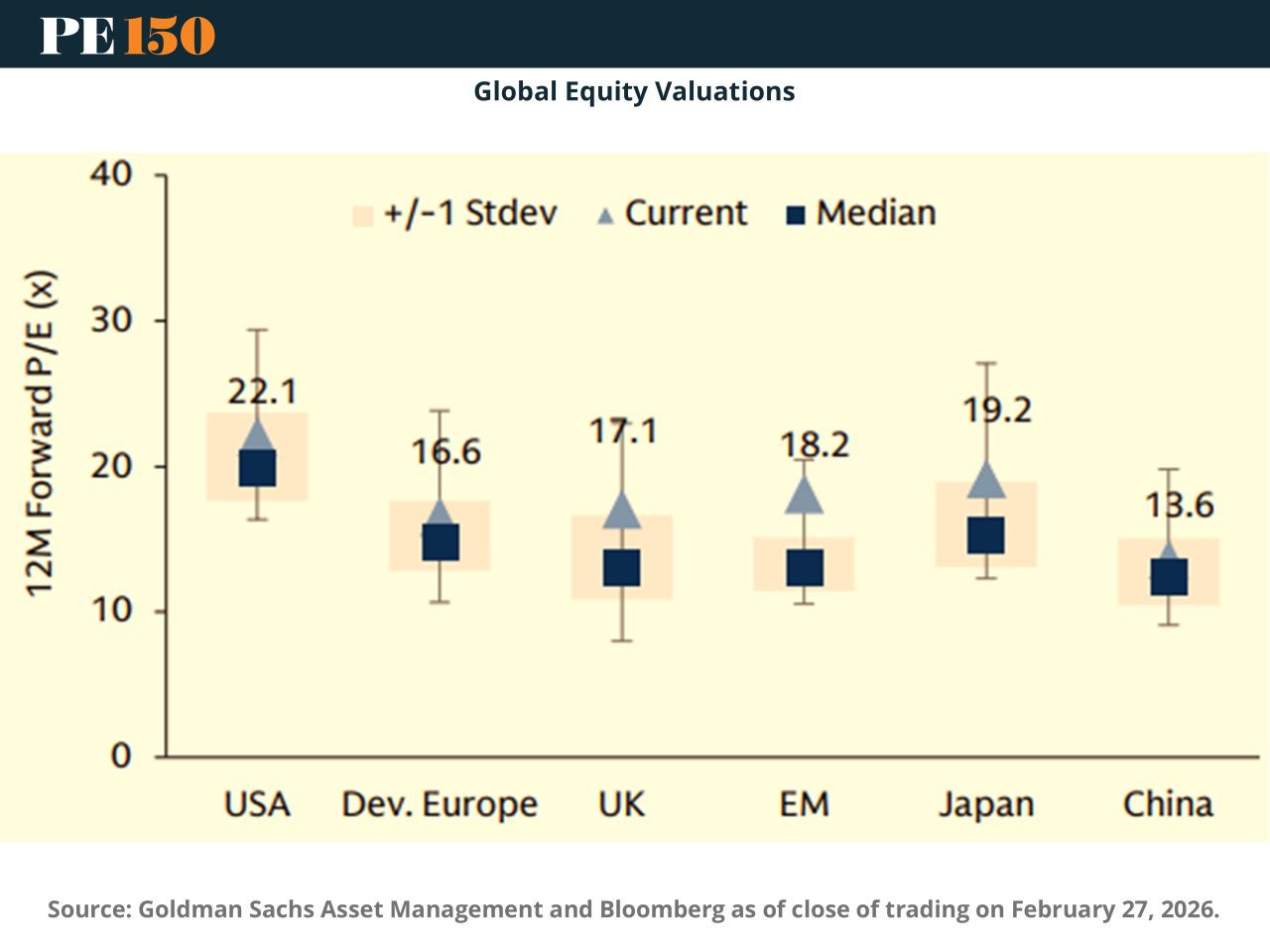

Equity markets now face a more discriminating environment. Global valuations suggest that the United States still trades at a premium, while Europe, the UK, emerging markets and China remain cheaper on a forward price-to-earnings basis. In a world of higher geopolitical risk and tighter financial conditions, those valuation gaps will matter more. Markets with lower starting valuations may prove more resilient, especially if the energy shock fades. But if it persists, geography and energy dependence will shape performance more than broad risk appetite alone.

The central macro conclusion is straightforward. This is a serious global supply shock, not yet a macroeconomic catastrophe. The world economy is more resilient than in past oil crises, but it is not immune. Much depends on duration. A short disruption would leave a scar; a prolonged one could reshape inflation, policy and growth well into 2026.

Sources & References

Deloitte. (2026). Weekly Global Economic Update. https://www.deloitte.com/us/en/insights/topics/economy/global-economic-outlook/weekly-update.html

Goldman Sachs. (2026). Market Monitor. https://am.gs.com/cms-assets/gsam-app/documents/insights/en/2026/market_monitor_032026.pdf?view=true