- PE 150

- Posts

- The Five Layers of Asymmetry

The Five Layers of Asymmetry

In investing, “asymmetric” is often used casually to describe opportunities with significant upside.

Introduction: What “Asymmetric” Actually Means

In investing, “asymmetric” is often used casually to describe opportunities with significant upside. But true asymmetry is more exacting. It refers to situations where potential gains materially exceed potential losses, and where the probability-weighted expected value is decisively positive.

A lottery ticket, for example, offers enormous upside but a negative expected value. That is not asymmetry—it is simply speculation with unfavorable odds.

Genuine asymmetry arises when multiple structural advantages align simultaneously. The framework outlined here identifies five distinct layers:

Structural Asymmetry

Informational Asymmetry

Time Horizon Asymmetry

Complexity Asymmetry

Behavioral Asymmetry

When these layers converge within a single asset class, their effects compound multiplicatively rather than add linearly. Energy infrastructure today provides a clear example of this dynamic in practice.

1. Structural Asymmetry: Limited Downside, Expansive Upside

Structural asymmetry begins with the shape of the payoff: downside is constrained, while upside remains open-ended.

Most traditional equity portfolios—especially those heavily weighted toward index funds—are broadly symmetric. For instance, the S&P 500 trading at roughly 20–22x earnings may deliver 8–10% annual returns under favorable conditions, but it also carries meaningful downside risk during recessions or valuation compression. Gains and losses are largely proportional.

Energy infrastructure, however, operates under a fundamentally different structure. The United States is entering a generational surge in power demand. Data centers, AI-driven compute expansion, reshoring of manufacturing, transportation electrification, and industrial growth all converge on a single constraint: electricity generation and grid capacity.

Electricity demand is not discretionary—it is essential and relatively non-cyclical. This creates a natural floor for demand, even during economic slowdowns.

At the same time, the scale of the required infrastructure buildout introduces substantial upside potential.

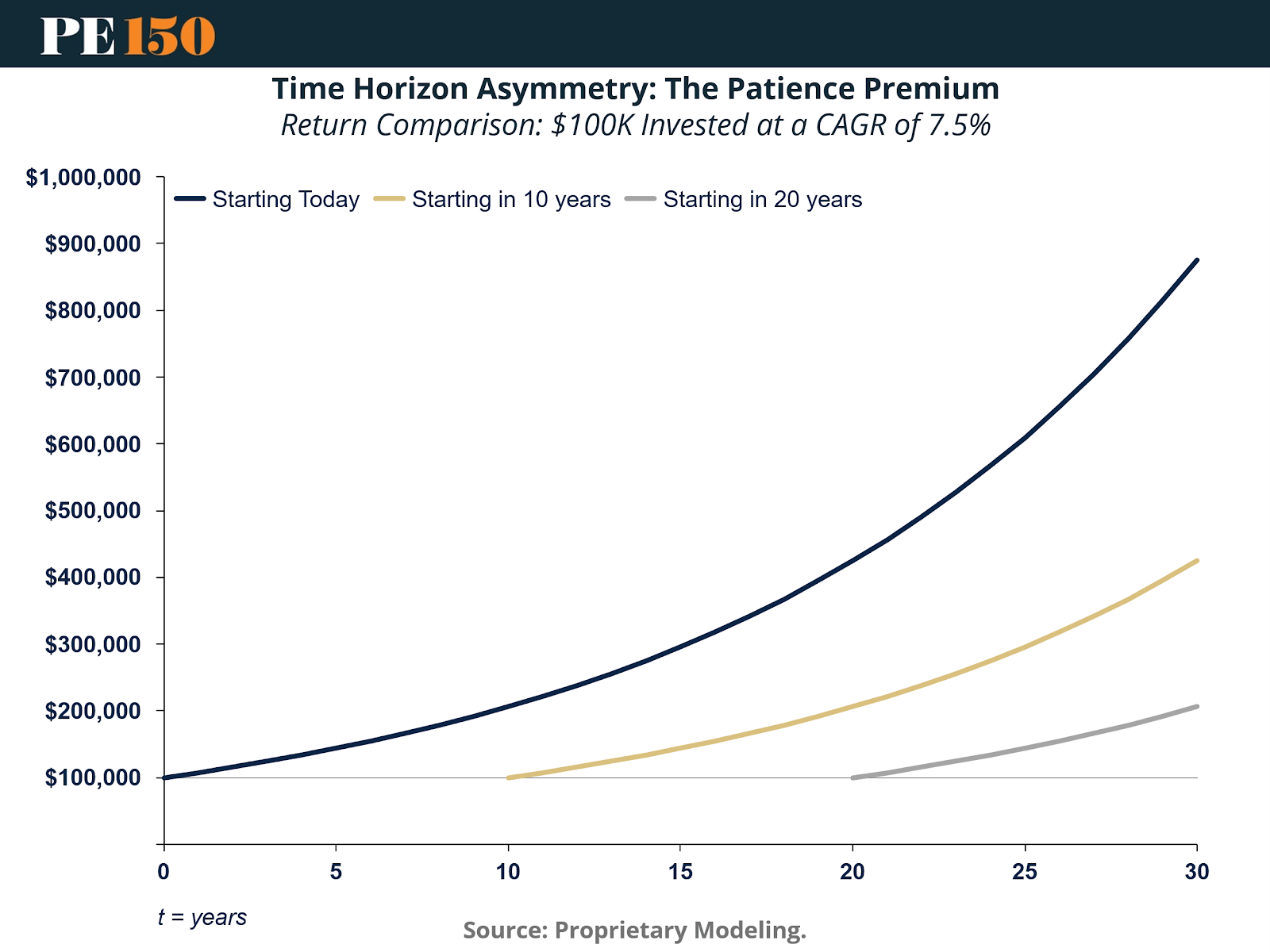

The compounding example underscores a core principle of asymmetry: early positioning in structurally advantaged environments dramatically amplifies outcomes. A $100,000 investment compounding at 7.5% over 30 years grows to nearly $900,000. Delaying entry by ten years roughly halves the terminal value; delaying by twenty years reduces it to about one quarter.

Energy infrastructure today resembles the “start early” curve. Investors who position themselves at the outset of a multi-decade expansion capture compounding across the full cycle. Those who wait for greater certainty risk entering later, when much of the structural advantage is already reflected in valuations.

In this case, the payoff profile is driven by necessity-based demand and early exposure to a long-duration buildout cycle.

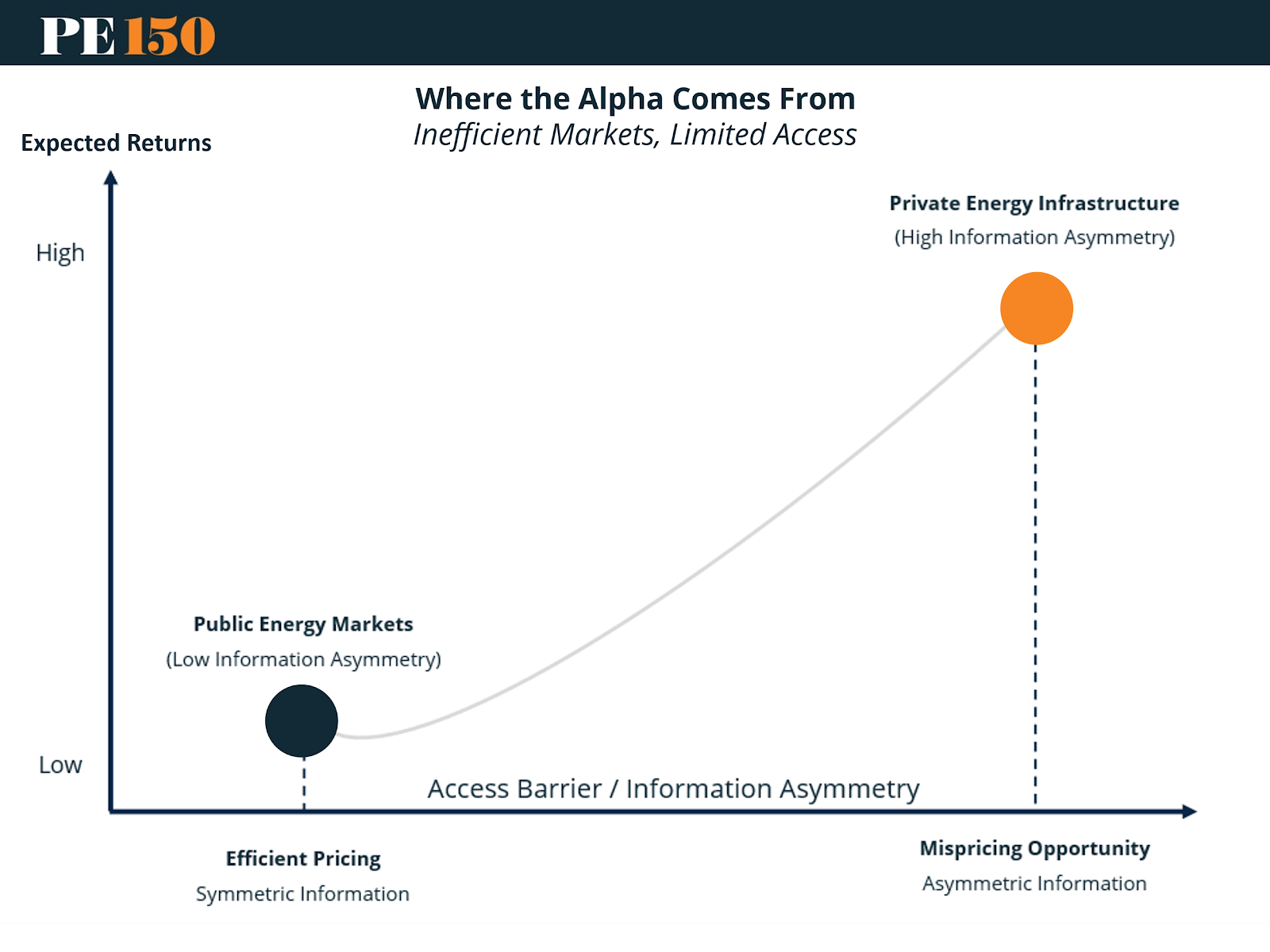

2. Informational Asymmetry: Inefficient Markets and Restricted Access

The second layer of asymmetry centers on market efficiency. Public energy equities are extensively covered and highly efficient. Thousands of analysts, institutional investors, and algorithmic systems continuously process the same data, driving prices toward consensus in real time.

In such environments, informational edge is minimal. Opportunities for excess return are quickly arbitraged away.

Private energy infrastructure markets operate under a fundamentally different paradigm. Barriers to entry are high, and evaluating opportunities requires domain-specific expertise across multiple dimensions, including:

Permitting timelines

Interconnection queue positioning

Off-take agreements

Utility relationships

Local and state regulatory frameworks

Consider the U.S. interconnection queue: thousands of gigawatts of proposed generation capacity are awaiting approval, yet only a small fraction ultimately reach commercial operation. Determining which projects will successfully navigate regulatory, engineering, and economic hurdles demands specialized operational insight.

This is where informational asymmetry emerges. Access is constrained—not just by capital, but by relationships, expertise, and execution capability. Unlike public markets, exposure cannot be obtained with a simple transaction through a brokerage account.

The underlying dynamic is straightforward: as barriers to access increase and information becomes less evenly distributed, the potential for mispricing expands. Public energy markets, characterized by transparency and informational symmetry, tend to offer lower expected returns. Private energy infrastructure, where information is fragmented and execution is complex, occupies the opposite end of the spectrum—where inefficiencies, and therefore opportunity, are greater.

In this context, inefficiency is not incidental; it is structural. It arises from friction—permitting complexity, regulatory nuance, and operational challenges. These frictions discourage marginal capital and, in doing so, preserve opportunities for those with the capability to navigate them.

3. Time Horizon Asymmetry: The Patience Premium

Modern capital markets are governed by short feedback cycles. Quarterly earnings, daily price volatility, and near-term performance benchmarking heavily influence decision-making.

Energy infrastructure operates on an entirely different timeline.

Power generation assets require years to develop. Transmission projects can take a decade or more. Nuclear and next-generation energy systems often extend across political cycles. Meanwhile, revenue streams are typically secured through long-duration contracts.

This disconnect between short-term capital and long-duration assets creates time horizon asymmetry.

Investors willing to commit capital over 7–10 years are, in effect, acquiring patience at a discount. Illiquidity—often penalized in public markets—becomes an advantage. While public equities fluctuate with macro headlines and sentiment shifts, contracted infrastructure assets tend to generate stable, predictable cash flows with limited correlation to daily market noise.

The compounding principle discussed earlier reinforces this dynamic: sustained exposure to structurally advantaged investments drives disproportionate outcomes. Exiting too early forfeits the steepest portion of the compounding curve.

Time horizon asymmetry ultimately rewards investors who align their investment duration with the intrinsic lifecycle of the asset.

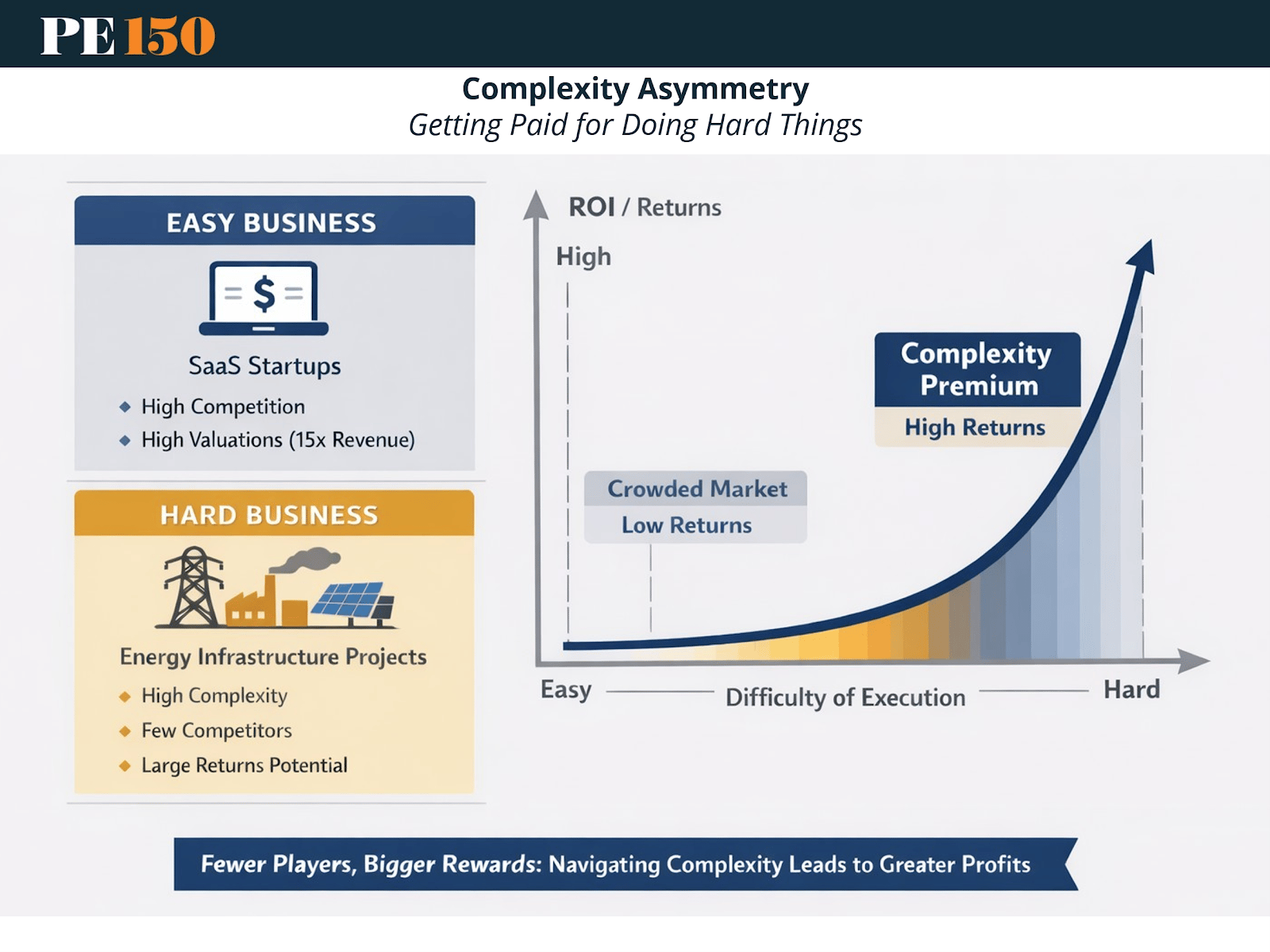

4. Complexity Asymmetry: Getting Paid for Difficulty

Complexity is frequently mispriced because it deters participation.

Energy infrastructure is inherently challenging to execute. Developers must navigate multiple layers of coordination and constraint, including:

Federal, state, and local permitting

Environmental impact assessments

Community and stakeholder engagement

Utility negotiations

Grid engineering requirements

Structured project financing

Each layer introduces friction—and each layer reduces the pool of capable participants.

In contrast, simpler business models, such as software companies, are easier to evaluate and scale. That accessibility attracts capital, increases competition, expands valuations, and ultimately compresses expected returns.

Complex projects behave differently. Their operational and regulatory difficulty discourages marginal capital, limiting competition.

As a result, returns often scale with execution difficulty. “Easy” businesses attract abundant capital and tend to trade at premium valuations, leading to lower forward returns. “Hard” businesses—like infrastructure development—require specialized capabilities and attract fewer qualified operators. This scarcity creates a complexity premium.

That premium exists because the difficulty is real and costly. However, for investors who can underwrite and manage that complexity, the payoff can be significant. Assets acquired at discounted valuations may re-rate meaningfully once execution risk is resolved and projects become operational.

In this framework, complexity functions as a moat—protecting returns by limiting competition.

5. Behavioral Advantage: Discipline in Private vs. Public Markets

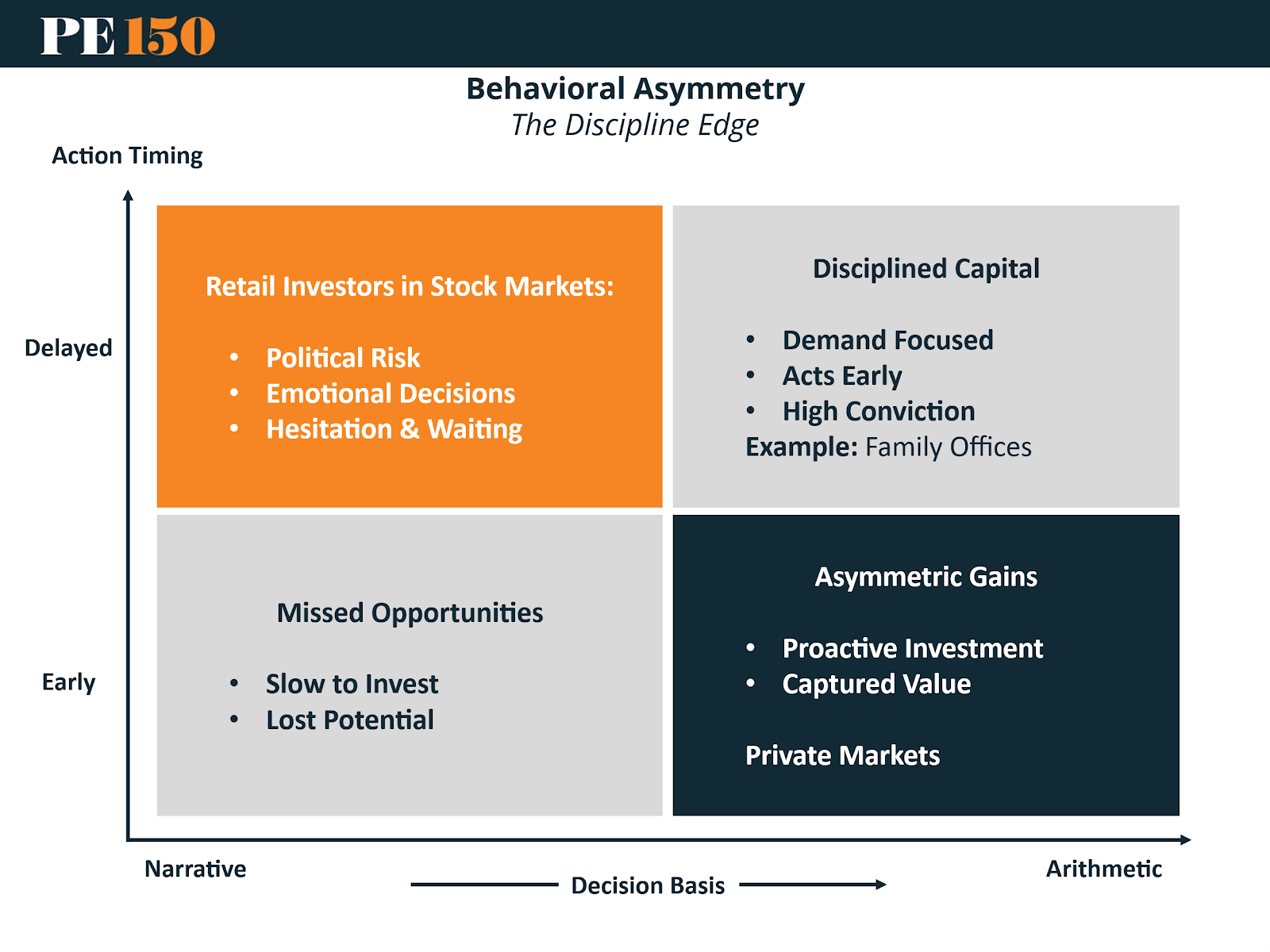

The final dimension of asymmetry determines whether the theoretical advantages of an investment actually translate into realized returns. This is where behavior becomes decisive.

Public markets are highly susceptible to narrative volatility. Prices move not only on fundamentals, but on sentiment, headlines, and short-term expectations. Investors are constantly exposed to noise—macroeconomic data releases, policy speculation, and shifting market narratives—which can distort decision-making and encourage reactive behavior. As a result, even when underlying fundamentals remain intact, capital allocation is often delayed or misdirected.

Private markets operate differently. The absence of continuous price discovery reduces exposure to daily sentiment swings. Investors are less influenced by short-term narratives and more anchored to the underlying economics of the asset—cash flows, demand drivers, and long-term value creation. This structural separation from market noise creates a behavioral advantage.

Behavioral asymmetry emerges when investors prioritize fundamental arithmetic over narrative-driven reactions. In public markets, the constant flow of information creates pressure to act—or not act—based on incomplete or transient signals. In private markets, the longer feedback loop allows decisions to be made with a focus on long-duration outcomes rather than short-term fluctuations.

This difference has practical consequences. Many investors can identify attractive opportunities, but fail to allocate capital due to discomfort with uncertainty or the absence of consensus. Public markets amplify this hesitation through volatility and visibility. Private markets, by contrast, reward investors who can commit capital with conviction and maintain discipline over extended periods.

Ultimately, the advantage lies in alignment. Private market structures naturally support long-term thinking, reduce behavioral interference, and enable investors to capture opportunities that require decisiveness before broad consensus emerges.