- PE 150

- Posts

- What GPs, AI Investors, and Energy Markets Are Telling Us This Week

What GPs, AI Investors, and Energy Markets Are Telling Us This Week

This week we examine how the rise of new private equity products is reshaping GP operations.

Good morning, ! This week we examine how the rise of new private equity products is reshaping GP operations, the acceleration of funding in robotic and physical AI, and China’s oil demand as a key pressure point in the evolving Middle East landscape.

Juniper Square shares how Avanath Capital Management modernized operations as fund complexity increased — replacing fragmented processes with a more connected operating model across fund accounting, reporting, and investor servicing. See how one GP reduced friction, improved visibility, and strengthened the investor experience with infrastructure built to scale. Read the Avanath story →

DATA DIVE

Operational Implications for GPs in the New Private Markets

The dispersion between private credit and private equity is no longer just an asset allocation discussion—it is an operating model decision. Private credit delivers ~7–10% returns at materially lower volatility, while buyout and venture strategies push 15–18% returns with significantly higher dispersion. This bifurcation forces GPs to institutionalize multi-strategy platforms and align underwriting, risk, and reporting frameworks across fundamentally different return profiles.

Operationally, this means building credit servicing capabilities, portfolio monitoring cadence (monthly vs quarterly), and integrated risk systems—capabilities historically absent in traditional PE shops. The rise of credit is not additive; it is transformative.

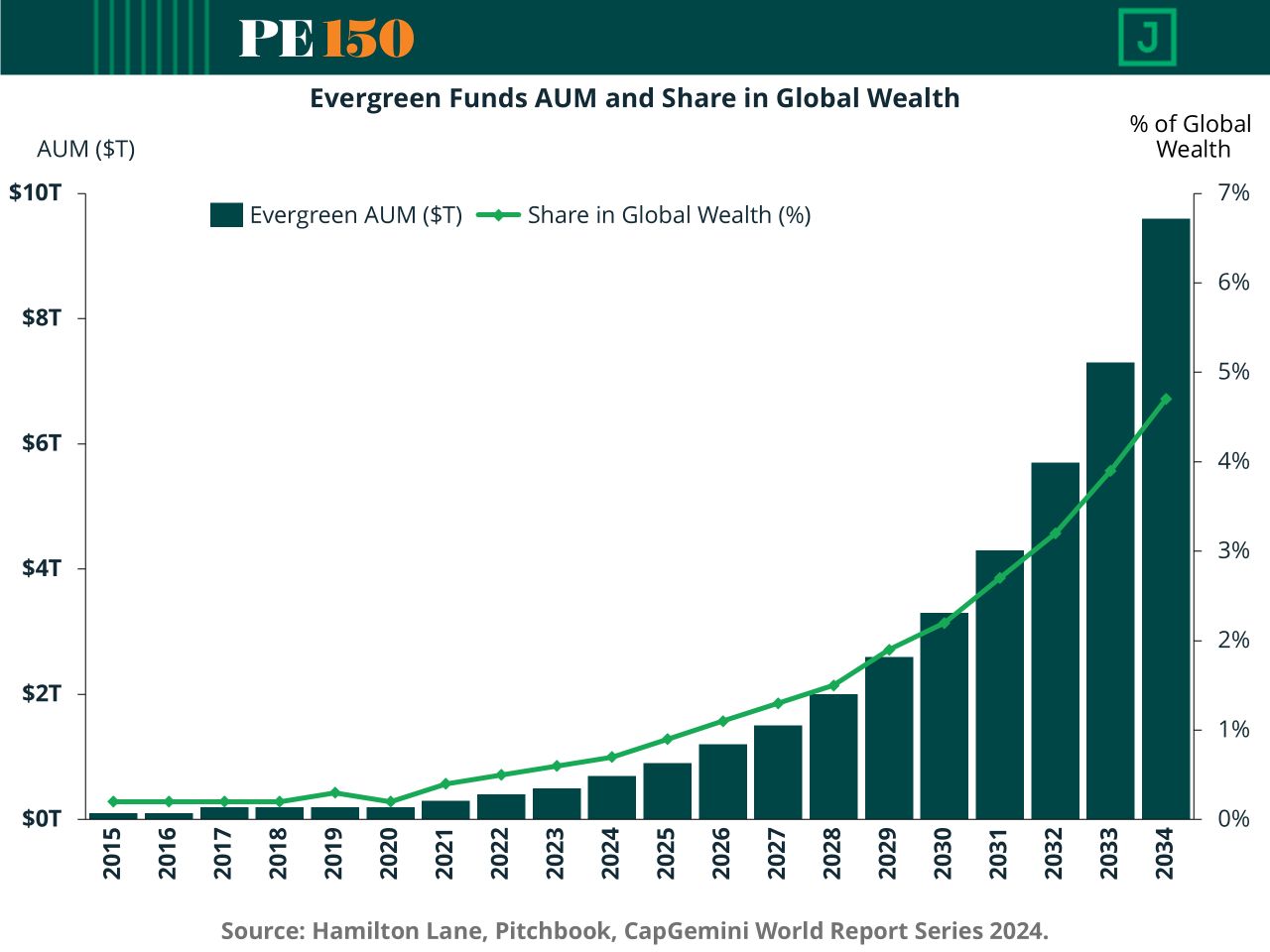

Evergreen AUM scaling toward ~$10T and ~5% of global wealth signals a shift from episodic fundraising to continuous capital management. For GPs, this introduces a permanent operating reset:

Cash management becomes real-time, not vintage-based

NAV production shifts from quarterly to frequent cycles

Liquidity engineering (interval/tender mechanics) becomes core infrastructure

Critically, performance is now driven as much by capital deployment efficiency (~90% invested vs ~30% in drawdown models) as by asset selection.

Bottom Line for GPs

The convergence of evergreen structures, continuation vehicles, and private credit requires GPs to evolve from deal-centric organizations into platform operators. The competitive edge is shifting toward:

Capital continuity management

Liquidity design and governance

Integrated multi-product operating models

Product innovation has already scaled—operational maturity is now the bottleneck.

TREND TO WATCH

Scale Over Science

Private equity has seen this movie before—and it’s entering the third act.

Robotics investing is shifting from lab experiments to factory floors. Deal value nearly doubled to $27.7B in 2025, even as deal count stayed relatively flat. Translation: fewer bets, bigger checks.

The capital isn’t spraying evenly. Healthcare robotics, industrial automation, and defense applications are pulling ahead—segments where ROI is measurable and immediate. Meanwhile, logistics robotics is losing altitude, down 28.5% YoY.

The real tell: mega-rounds and platform plays. Investors are backing companies that look less like startups and more like future incumbents.

Exits remain soft, but strategic M&A is picking up, with corporates buying instead of building.

Bottom line: This is no longer venture tourism. It’s PE-style consolidation, with winners scaling fast—and everyone else quietly becoming features. (More)

PRESENTED BY JUNIPER SQUARE

How one GP modernized operations for a more complex fund structure

As firms expand into new fund structures, increase investor counts, and face heightened reporting expectations, the operating model either scales with them or becomes the constraint.

Avanath Capital Management reached that inflection point. As their platform grew, so did the complexity across fund accounting, reporting, and investor servicing. Rather than adding more manual processes or stitching together additional systems, they modernized their infrastructure with Juniper Square.

See how Avanath:

Unified fund and investor data on a single platform

Reduced reconciliation and reporting friction

Increased visibility across teams

Strengthened the investor experience through connected operations

The outcome wasn’t just efficiency; it was operational resilience.

Supporting our sponsors supports our free newsletters. Please support our sponsors!

COMPLIANCE CORNER

The 401(k) Unlock

Private equity just got a foot in the retirement door—now comes the compliance bill.

New DOL guidance is easing prior restrictions, replacing “extreme caution” with a facts-and-circumstances approach to fiduciary prudence. Add the August 2025 Executive Order, and the message is clear: private markets are welcome in defined contribution plans.

But access comes with strings. ERISA fiduciary duties, prohibited transaction rules, and litigation risk remain fully intact.

For sponsors, the focus is process over outcome—with heavy documentation on fees, valuation, liquidity, and conflicts.

For managers, this means retooling: ERISA-friendly structures, fee transparency, and independent valuation frameworks are no longer optional.

Bottom line: The door is open—but it’s guarded. Winning allocations will require institutional-grade compliance, not just performance. (More)

LIQUIDITY CORNER

Liquidity Is Improving. Cash Isn’t Flowing.

Stat: Distributions have remained below 15% of NAV for four straight years, while roughly 32,000 unsold assets worth $3.8 trillion sit on PE balance sheets

Context: On paper, 2025 looked like a recovery. Buyout value rose 44% to $904 billion and exits climbed 47% to $717 billion. But beneath the rebound, capital is not recycling. Holding periods have stretched to about seven years, and returns are increasingly tied to operational execution rather than multiple expansion. LPs are still waiting for cash, and many rely on those distributions to fund new commitments, creating a feedback loop that slows fundraising and deal velocity.

Strategic Takeaway: The constraint is no longer deal activity. It is cash conversion. GPs who cannot manufacture liquidity through secondaries, continuation vehicles, or structured solutions risk becoming capital bottlenecks. In this cycle, DPI is strategy, not an outcome. (More)

MACROVIEW

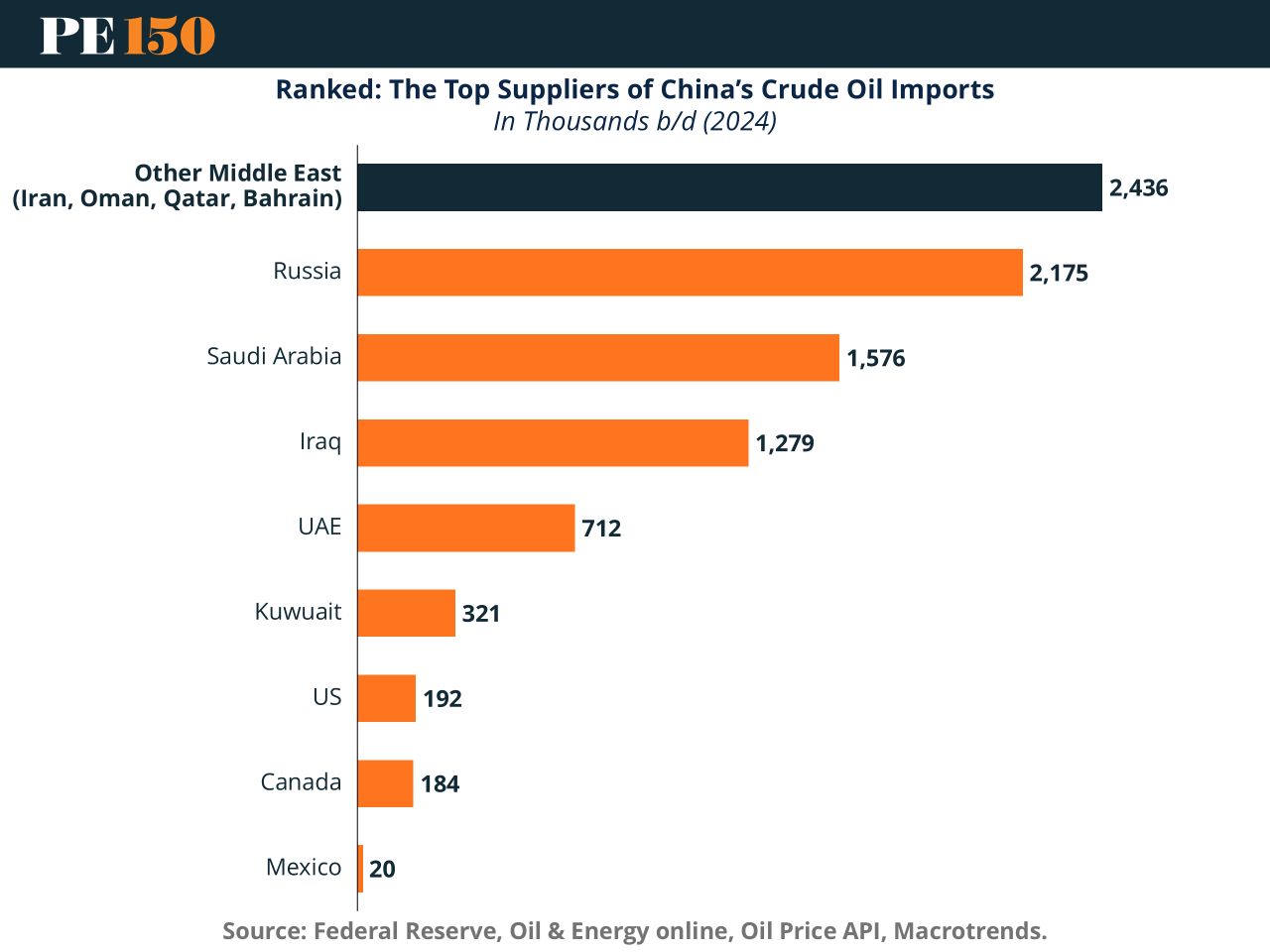

China’s Oil Dependency Is the World’s Pressure Point

China now anchors global oil demand, importing over $500B in crude in 2024—roughly one-fifth of global flows. While Beijing is diversifying suppliers, shifting toward Russia, Malaysia, and Brazil, its energy system remains structurally exposed to Middle Eastern supply and USD pricing.

Russia’s discounted oil has become critical, but so has opaque supply from Iran—quietly reinforcing China’s energy security. This creates a strategic tension: any disruption in Middle Eastern flows could disproportionately impact China’s growth via higher input costs and currency pressure.

Markets should watch this closely. Oil is no longer just a commodity—it’s a macro lever shaping China’s industrial outlook and global economic stability. (More)

Read the Avanath story to see how one GP modernized operations for a more complex fund structure. Read the story →

Supporting our sponsors supports our free newsletters. Please support our sponsors!

"Success is walking from failure to failure with no loss of enthusiasm."

Winston Churchill