- PE 150

- Posts

- China’s Oil Gravity: Demand Dominance, Supply Diversification, and Geopolitical Fault Lines

China’s Oil Gravity: Demand Dominance, Supply Diversification, and Geopolitical Fault Lines

Demand Power Meets Supply Strategy — China Reshapes the Global Oil Map

Gaston Brizuela Bosio

March 24, 2026 • Estimated Reading Time: 3 minutes

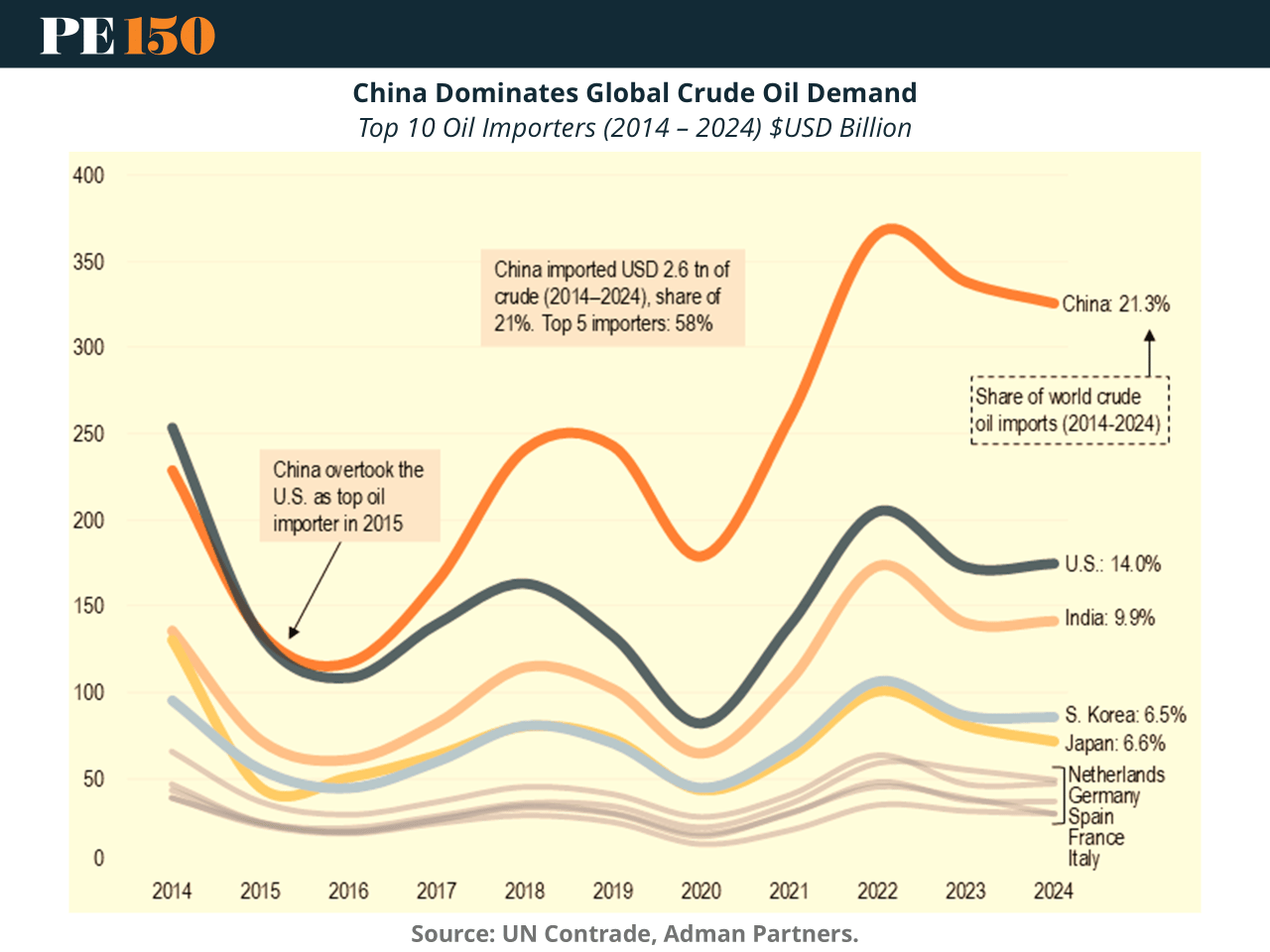

China has become the central node in the global oil system. Over the past decade, it has accounted for roughly one-fifth of global crude imports, overtaking the U.S. in 2015 and maintaining that lead ever since. This is not merely a trade statistic—it is a structural macroeconomic reality. Global oil flows, pricing dynamics, and even geopolitical alignments increasingly orbit around Chinese demand.

In 2024, China imported $503.4 billion of crude oil, nearly doubling (+92.8%) from 2020 levels. Despite a slight year-over-year contraction (-2.1%), the scale remains unprecedented. Oil is China’s second-largest import category, underscoring a critical vulnerability: growth remains energy-intensive and externally dependent.

Concentration vs Diversification: A Managed Dependency

The global oil market is defined by concentration on both sides. A handful of exporters—Saudi Arabia, Russia, the UAE, Canada, and the U.S.—supply a disproportionate share of global crude. Simultaneously, China stands as the single largest demand center.

However, China has been actively engineering diversification within this concentration. In 2024:

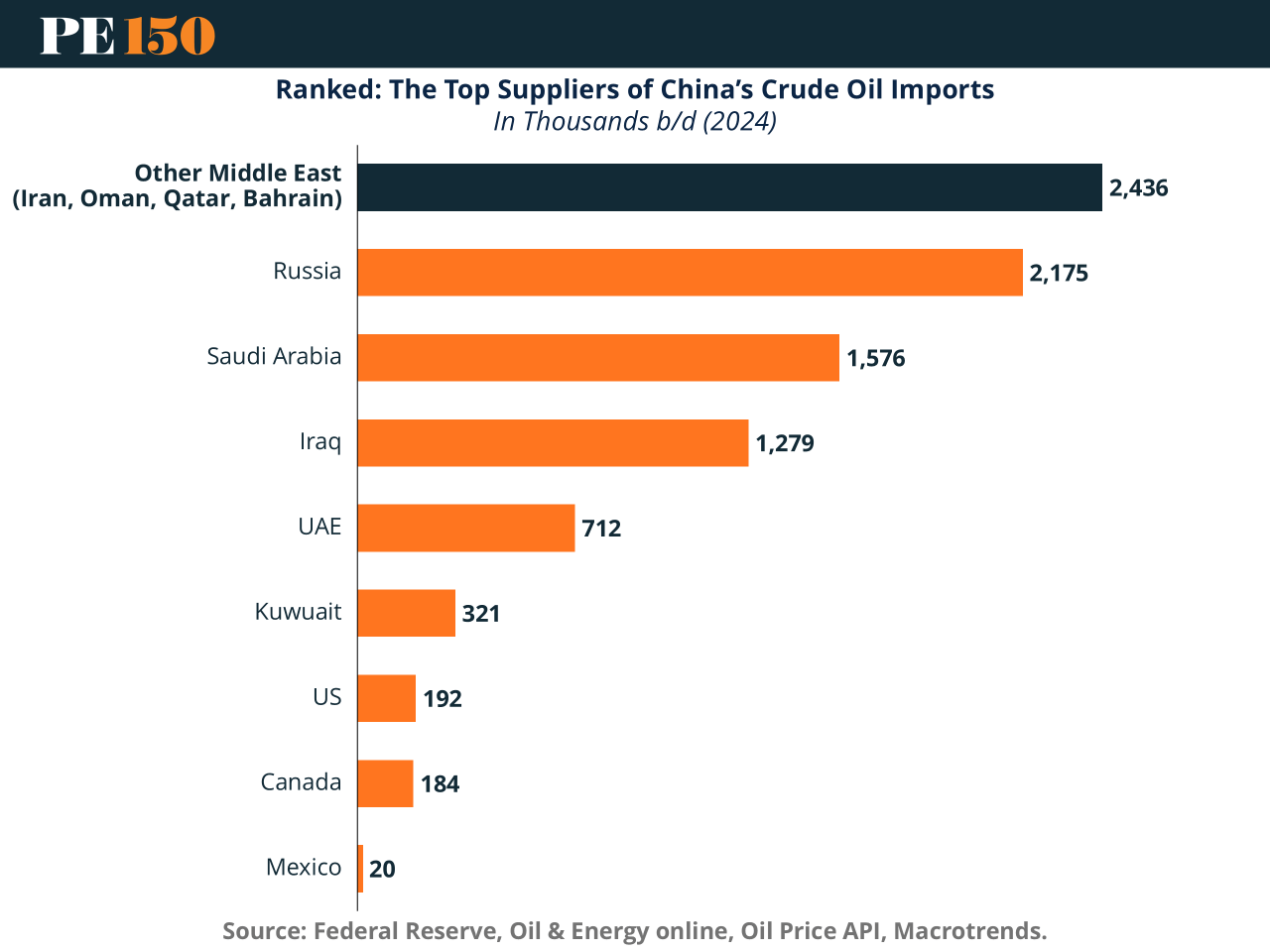

The top five suppliers (Russia, Malaysia, Saudi Arabia, Iraq, UAE) accounted for 52.4% of imports

Russia alone supplied 18.8% ($94.8B)

Middle Eastern sources still contributed ~34.8%, but with declining marginal importance

OPEC’s share fell to 35.3%, down from 40.1% in 2020

This is not accidental. It reflects a deliberate policy to reduce exposure to any single geopolitical bloc—particularly OPEC pricing power.

At the same time, China’s import bill is structurally exposed to USD-denominated pricing. With the yuan depreciating by 1.7% in 2024, the real cost of oil rises domestically, tightening financial conditions and reinforcing imported inflation pressures.

Russia, Discounts, and Strategic Realignment

Russia has emerged as China’s anchor supplier, exporting roughly 2.2 million barrels per day. The post-Ukraine war environment has accelerated this relationship, as Russian Urals crude trades at a $5–$10 discount relative to benchmarks.

This creates a mutually reinforcing macro dynamic:

China secures discounted energy inputs, supporting industrial margins

Russia secures a stable buyer amid Western sanctions

Beyond Russia, Middle Eastern suppliers remain critical. Saudi Arabia (~1.6 mb/d) and Iraq (~1.3 mb/d) are major contributors, while a broader category labeled “Other Middle East” (including Iran) supplies an even larger combined volume.

Notably, Iran exports up to ~90% of its crude to China, often via opaque or discounted channels. This makes Iran less a marginal supplier and more a shadow cornerstone of China’s energy system.

The Declining Role of the United States

Despite being a major global producer, the U.S. accounts for only ~4.6% of China’s imports ($23.1B) and less than 2% by volume in recent estimates. Trade tensions, logistics, and political risk have constrained this channel.

Instead, China has diversified toward:

Malaysia (+13.6% growth)

Australia (+11.1%)

Brazil and West Africa

Even marginal suppliers like Norway and Venezuela (triple-digit growth rates)

This reflects a portfolio approach to energy security—not eliminating dependence, but distributing it.

A Structural Vulnerability: Geography

Despite diversification, one fact remains: a significant portion of China’s oil flows originates from the Middle East and passes through chokepoints such as the Strait of Hormuz.

This raises a controversial but analytically relevant question:

Could conflict involving Iran function—intentionally or not—as a constraint on China’s energy supply?

The argument, often raised in geopolitical circles, is straightforward:

Iran is a major indirect supplier to China

Disruption (via war, sanctions enforcement, or blockade) would tighten supply

China would face higher prices, logistical stress, and potential growth constraints

From a macroeconomic perspective, such a shock would operate through:

Terms-of-trade deterioration (higher import costs)

Industrial margin compression

Financial tightening via FX pressure

Supply chain disruptions in energy-intensive sectors

However, this theory should be treated cautiously. Global oil markets are fungible and adaptive. Supply shocks tend to re-route rather than disappear entirely. Moreover, China’s diversification strategy—Russia, Africa, Latin America—acts as a buffer against single-point disruptions.

Still, the risk is asymmetric: even partial disruption in Middle Eastern flows would disproportionately impact China relative to more energy-independent economies.

Conclusion: Demand Power, Strategic Constraint

China’s position in global oil markets is paradoxical:

It is the dominant demand driver, shaping global trade flows

Yet it remains structurally dependent on external supply, much of it geopolitically sensitive

The macroeconomic implication is clear: China wields market power without full supply sovereignty. This tension—between dominance and vulnerability—will define not only China’s energy strategy, but also the geopolitical landscape surrounding global oil in the decade ahead.

Sources & References

Andman Partners. (2025). China Dominates Global Crude Oil Demand. https://andamanpartners.com/2025/10/china-dominates-global-crude-oil-demand/

Visual Capitalist. (2025). Visualizing China’s Crude Oil Imports by Country. https://www.visualcapitalist.com/chinas-crude-oil-imports-by-country/

Worldexports. Top 15 Crude Oil Suppliers to China. https://www.worldstopexports.com/top-15-crude-oil-suppliers-to-china/