- PE 150

- Posts

- The Next Source of Risk

The Next Source of Risk

The evolution of credit markets over the past two decades has been defined by a gradual but consequential shift in the locus of financial intermediation.

Introduction

The evolution of credit markets over the past two decades has been defined by a gradual but consequential shift in the locus of financial intermediation. Traditional bank lending, once the dominant channel for corporate financing, particularly in the middle market, has ceded ground to nonbank financial institutions, most notably private credit vehicles. This transition reflects both regulatory and structural forces. Post-crisis capital and liquidity requirements have constrained banks’ willingness and ability to extend riskier, longer-duration loans, while institutional investors have increasingly sought yield through alternative asset classes offering illiquidity premia.

The result has been the rapid emergence of private credit as a core component of the global financial system. What began as a niche strategy has scaled into a multi-trillion-dollar asset class, providing bespoke financing solutions to borrowers that fall outside traditional bank underwriting frameworks. Crucially, the architecture of private credit differs from that of banks. It is largely funded by long-term, locked-in capital, pensions, insurers, endowments, rather than short-term, runnable liabilities. This structural distinction has shaped the prevailing perception that private credit, while exposed to credit risk, is less vulnerable to liquidity-driven contagion.

However, the current phase of the cycle raises a more nuanced question. The issue is not whether private credit contains risk, but how that risk is transmitted and where it ultimately resides. As capital has flowed rapidly into the asset class, particularly in sectors undergoing technological disruption, the interaction between leverage, refinancing needs, and evolving business models has begun to test underwriting assumptions formed under a different macro-financial regime. At the same time, the increasing interconnection between private credit and banks introduces a second-order channel through which localized credit deterioration could have broader implications.

This report examines the emerging dynamics of private credit risk through a data-driven lens. It focuses on three interrelated themes: the structural shift from banks to nonbanks, the gradual normalization of default rates beneath the surface of headline stability, and the evolving role of banks as liquidity providers to the private credit ecosystem. The objective is not to frame a deterministic outcome, but to characterize the conditions under which credit risk may accumulate and propagate in a system where liquidity and capital are increasingly decoupled from traditional banking structures.

1. Structural Shift: From Bank Intermediation to Private Credit

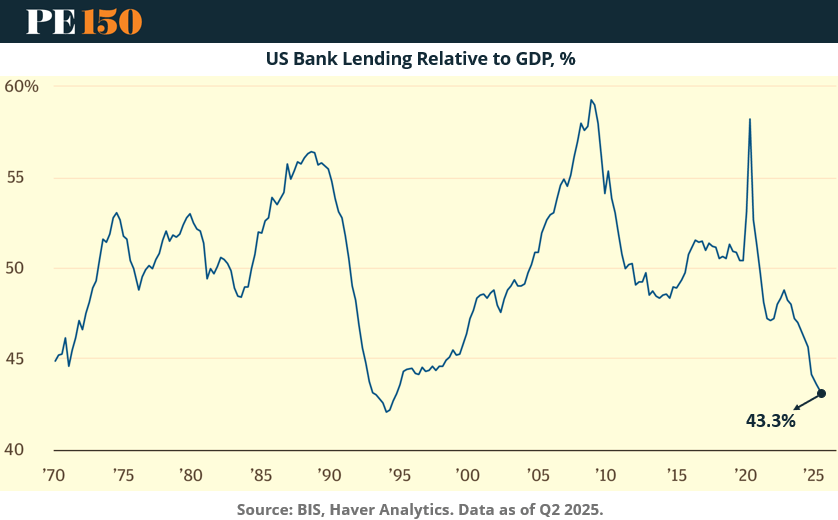

The expansion of private credit is best understood as the counterpart to a sustained decline in bank-centric lending relative to economic activity.

Over multiple decades, bank lending as a share of GDP has exhibited a downward trajectory, with the most recent reading near 43.3%, significantly below prior cyclical peaks. This trend reflects more than cyclical deleveraging; it captures a structural recalibration of bank balance sheets in response to tighter regulatory constraints and capital efficiency considerations.

As risk-weighted assets became more costly under Basel frameworks, banks increasingly shifted away from segments characterized by higher leverage, lower transparency, or longer duration, precisely the segments that private credit funds have targeted.

The decline in bank intermediation has not resulted in a contraction of total credit supply. Instead, lending activity has been redistributed across institutional forms.

The composition of lending balances reveals a substantial and growing contribution from nonbank intermediaries across corporate finance, real estate, and consumer segments. While banks still account for the majority of credit outstanding, nonbank participation is sufficiently large to influence both pricing and risk dynamics.

The addressable market for private credit, estimated at over $30 trillion, underscores the scale of this transition. Importantly, this redistribution introduces heterogeneity in underwriting practices. Private credit lenders often operate with greater flexibility in covenant structures, leverage tolerance, and deal customization, reflecting their ability to tailor financing solutions outside standardized bank frameworks.

The growth of private credit vehicles has been correspondingly rapid.

Assets under management have expanded from approximately $61 billion in the early 2000s to over $1.4 trillion by 2024, implying a compound annual growth rate exceeding 15%. This expansion reflects both supply and demand forces: investors seeking yield in a low-rate environment and borrowers requiring flexible financing solutions.

The accumulation of “dry powder” alongside deployed capital indicates that capital commitments have often outpaced immediate deployment opportunities, creating pressure to originate new loans at scale.

This structural shift has important implications for how risk is distributed. Private credit’s funding model, long-term capital funding long-term assets, reduces exposure to classic maturity transformation risks.

Unlike banks, which rely on short-term deposits to fund longer-duration loans, private credit funds operate with locked-in capital and limited redemption rights. This alignment mitigates the risk of forced asset sales triggered by investor withdrawals. Transmission of stress is therefore slower and more closely tied to borrower performance rather than funding dynamics.

However, this does not eliminate risk; it alters its temporal profile. Losses are more likely to accumulate gradually through credit deterioration rather than materialize abruptly through liquidity shocks.

2. Credit Conditions: Rising Leverage and Utilization Dynamics

While the structural case for private credit rests on funding stability, underlying borrower dynamics reveal a more complex picture.

Borrower leverage within private credit vehicles has trended upward over the past decade, with debt-to-asset ratios increasing steadily for BDCs relative to other nonbank financial institutions. This rise in leverage reflects both competitive pressures and the legacy of a low-rate environment in which higher leverage was more easily serviceable.

As interest rates have normalized at higher levels, the sustainability of these leverage ratios becomes more sensitive to earnings volatility and refinancing conditions.

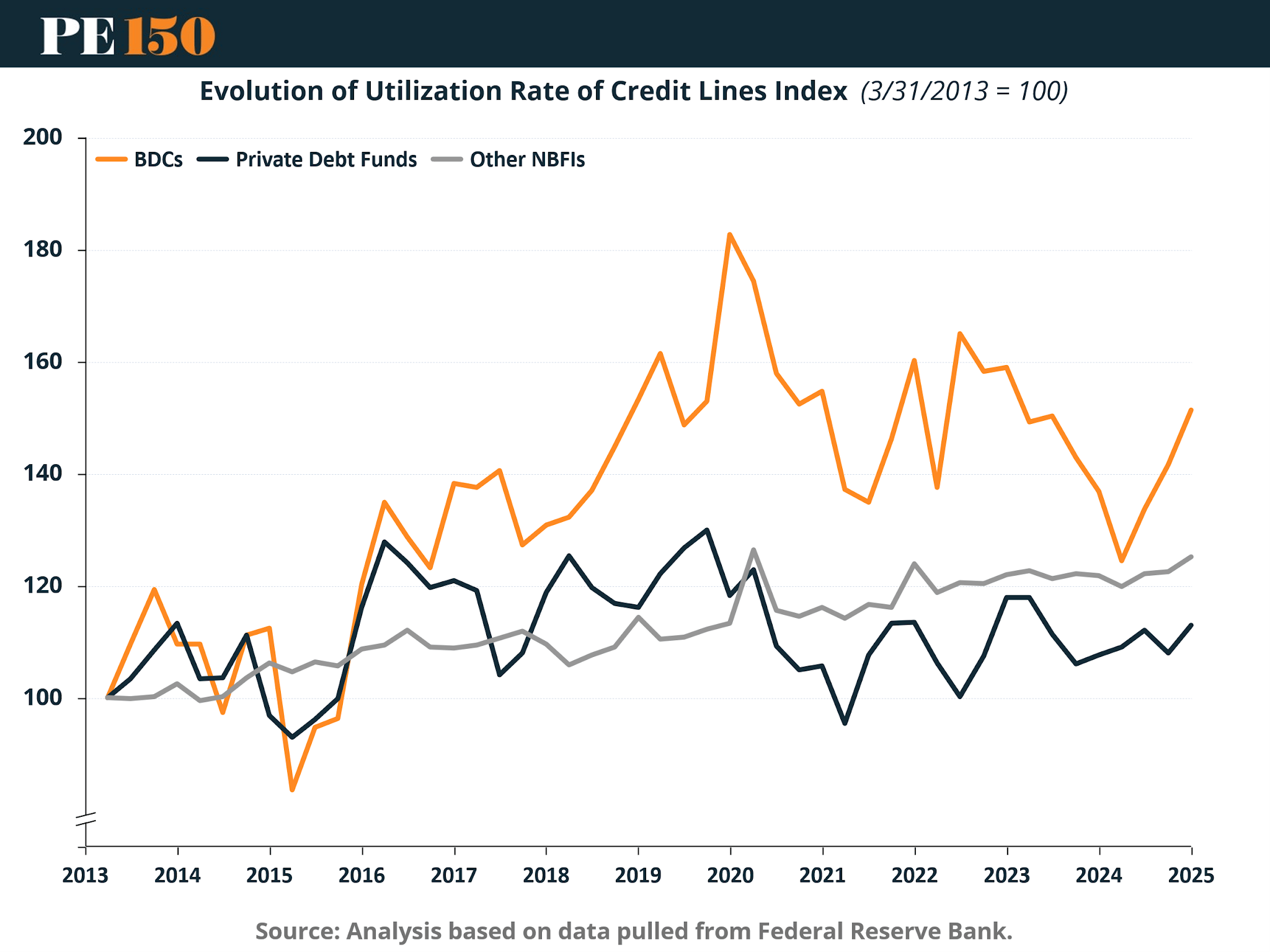

A complementary dimension of risk is visible in credit line utilization.

Utilization rates for private credit vehicles, both BDCs and private debt funds, consistently exceed those of other nonbanks, often hovering in the 55–65% range. Elevated utilization suggests that private credit vehicles rely more heavily on bank-provided liquidity to fund their operations. While utilization rates have converged somewhat across sectors, private credit remains structurally more dependent on these facilities.

This dependence is particularly relevant during periods of market stress, when access to alternative funding sources may become constrained.

The cyclical behavior of utilization is further clarified when indexed over time.

Indexed data show that utilization rates for BDCs exhibit greater volatility and a higher amplitude of increase compared to other nonbanks. Peaks in utilization correspond to periods of market stress or heightened funding demand, indicating that private credit vehicles draw more aggressively on bank credit lines when conditions tighten. This dynamic introduces a potential amplification mechanism: as borrower stress increases, private credit funds may simultaneously increase their reliance on bank liquidity, transmitting pressure back to the banking system. The characteristics of these credit lines provide additional context.

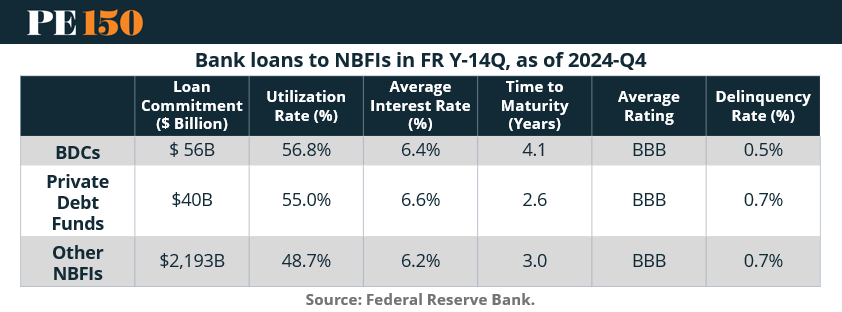

Bank lending to private credit vehicles is characterized by relatively high utilization rates, slightly elevated interest rates, and low delinquency metrics. Loans are predominantly investment grade, with average ratings around BBB and delinquency rates below 1%. At face value, this suggests that banks are not currently assuming excessive credit risk in their direct exposures. However, these metrics are backward-looking and may not fully capture the forward-looking implications of rising leverage and utilization. The combination of high utilization and increasing borrower leverage implies that credit lines may become more heavily drawn precisely when underlying asset quality is deteriorating.

3. Default Dynamics: From Benign Conditions to Normalization

The evolution of default rates provides a critical lens through which to assess the transition from benign to more normalized credit conditions.

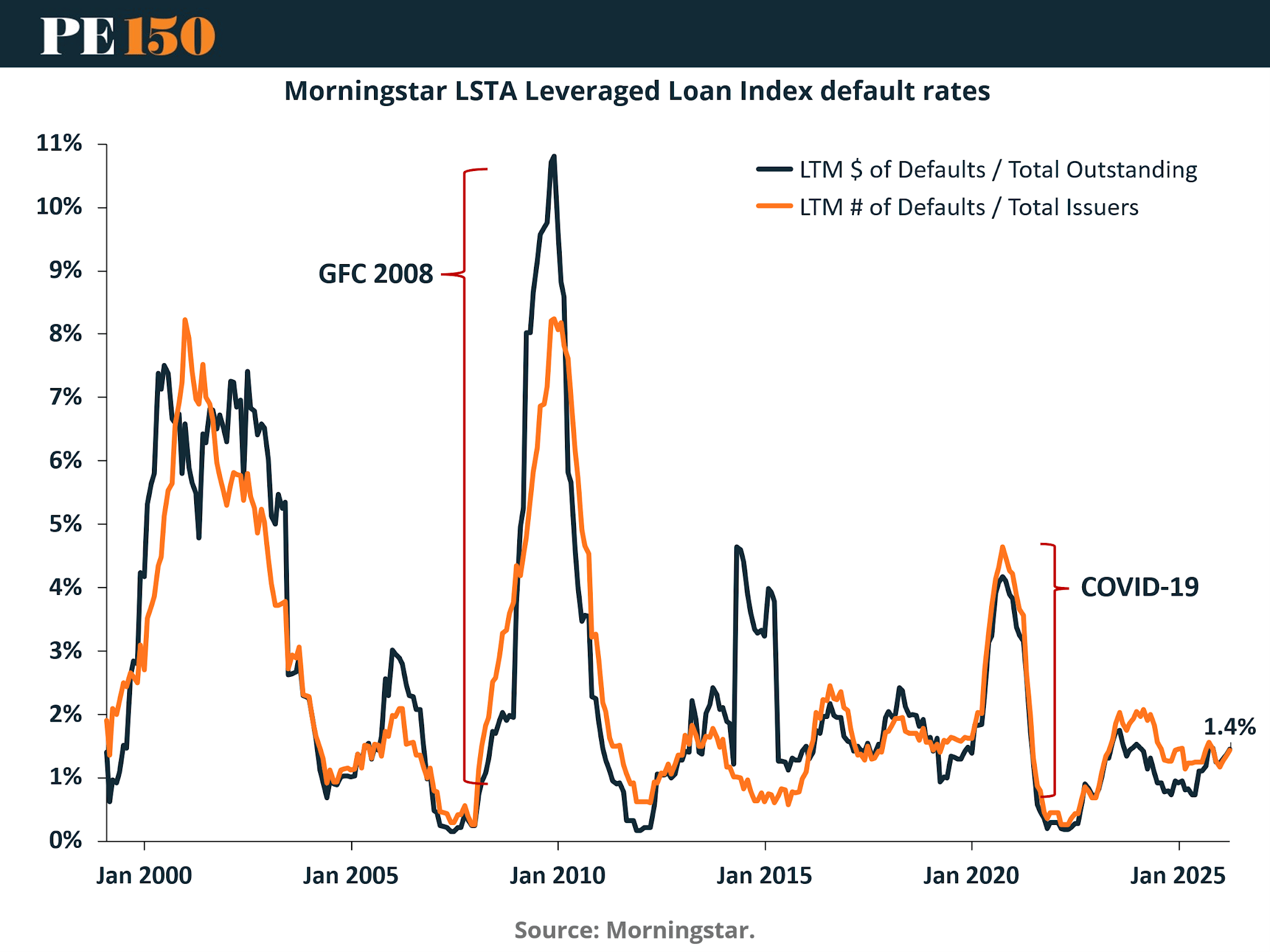

Historical data on leveraged loan defaults show a pattern of episodic spikes, most notably during the Global Financial Crisis and the COVID-19 shock, followed by periods of normalization. Current default rates remain well below crisis peaks but have begun to trend upward from historically low levels. This upward drift is consistent with a broader reversion toward average credit conditions after a prolonged period of suppressed defaults driven by low interest rates and ample liquidity.

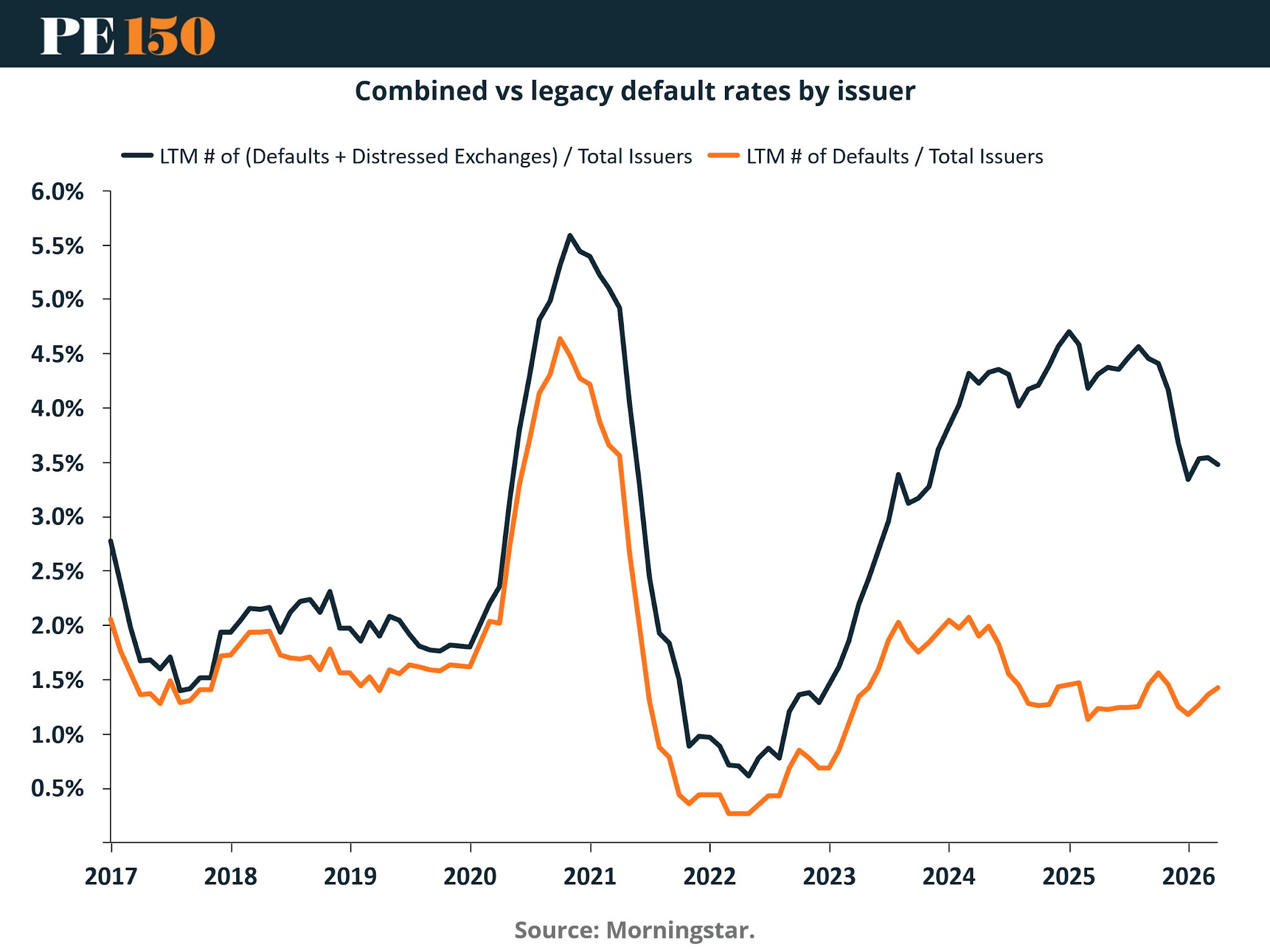

However, headline default rates may understate the extent of underlying stress.

When distressed exchanges and restructurings are incorporated into default measures, effective default rates rise materially above traditional metrics. The divergence between “legacy” defaults and combined default measures highlights the prevalence of liability management strategies, extend-and-amend transactions, covenant waivers, and payment-in-kind structures, that delay formal default recognition.

These mechanisms smooth the credit cycle in the short term but can obscure the accumulation of underlying risk.

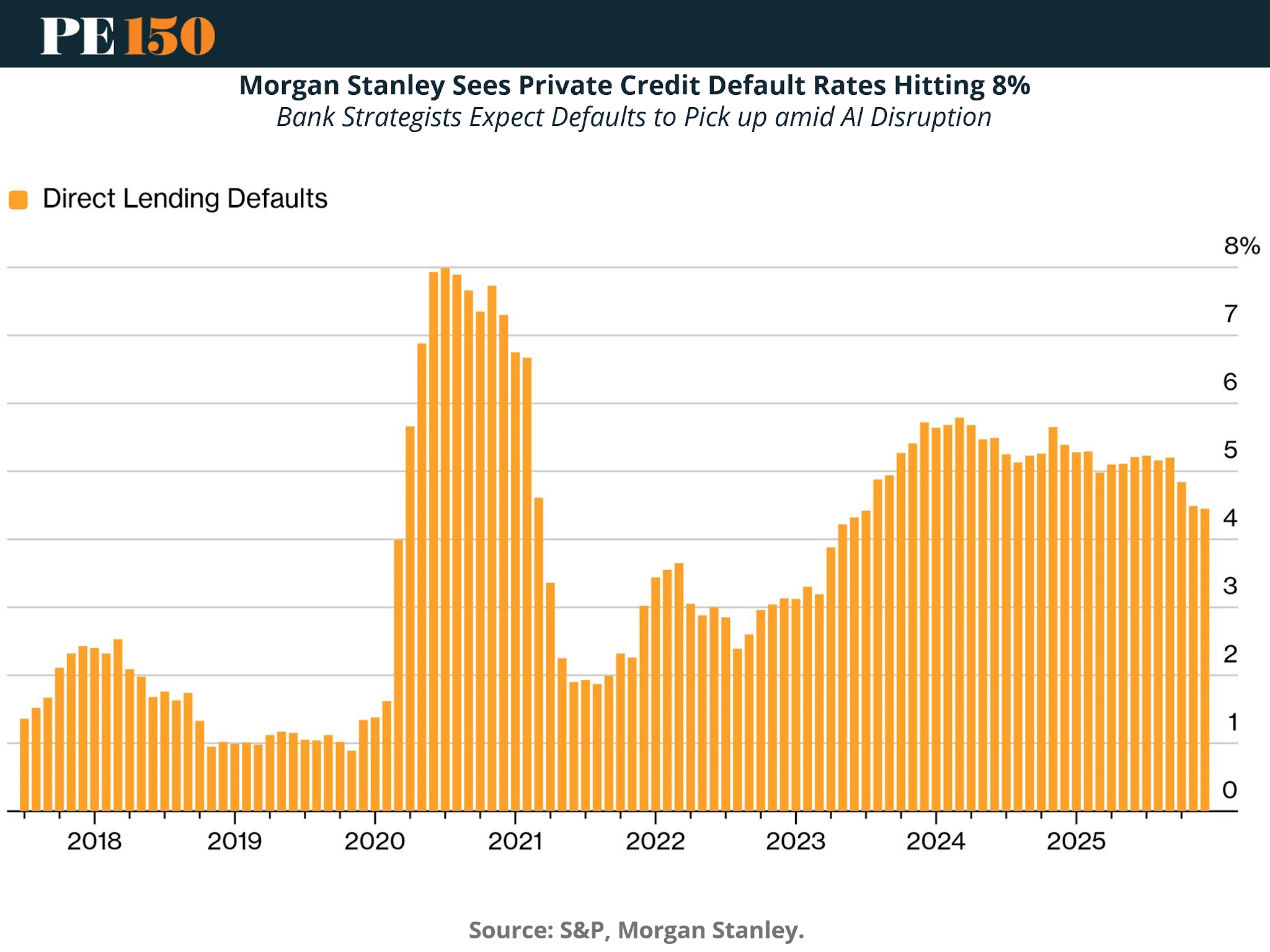

Forward-looking expectations reinforce the view that default rates are likely to continue normalizing.

Projections indicating potential default rates approaching 8% represent a significant increase from the historical range of 2–2.5%. Importantly, such levels would still fall short of systemic crisis thresholds observed in prior cycles. The adjustment would therefore be better characterized as a normalization of credit risk rather than an extreme stress event.

Nevertheless, the magnitude of the increase implies meaningful implications for portfolio performance, capital allocation, and future lending capacity.

4. Interconnections: The Banking System as Transmission Channel

The primary systemic dimension of private credit risk lies not within the asset class itself, but in its growing interconnection with the banking system.

Bank loan commitments to private credit vehicles have expanded rapidly over the past decade, with both commitments and utilized amounts increasing substantially. The scale of these exposures remains modest relative to total bank assets, but the growth trajectory is notable. Banks provide liquidity through revolving credit lines, warehouse financing, and strategic partnerships, effectively acting as enablers of private credit expansion.

This interdependence introduces a potential feedback loop. As private credit funds experience higher default rates and reduced cash flows, their demand for bank-provided liquidity may increase. Simultaneously, deterioration in underlying loan performance could impair the credit quality of bank exposures. While stress tests suggest that banks are currently well-capitalized and capable of absorbing such shocks, the scenario becomes more complex if liquidity demands are correlated across multiple nonbank sectors.

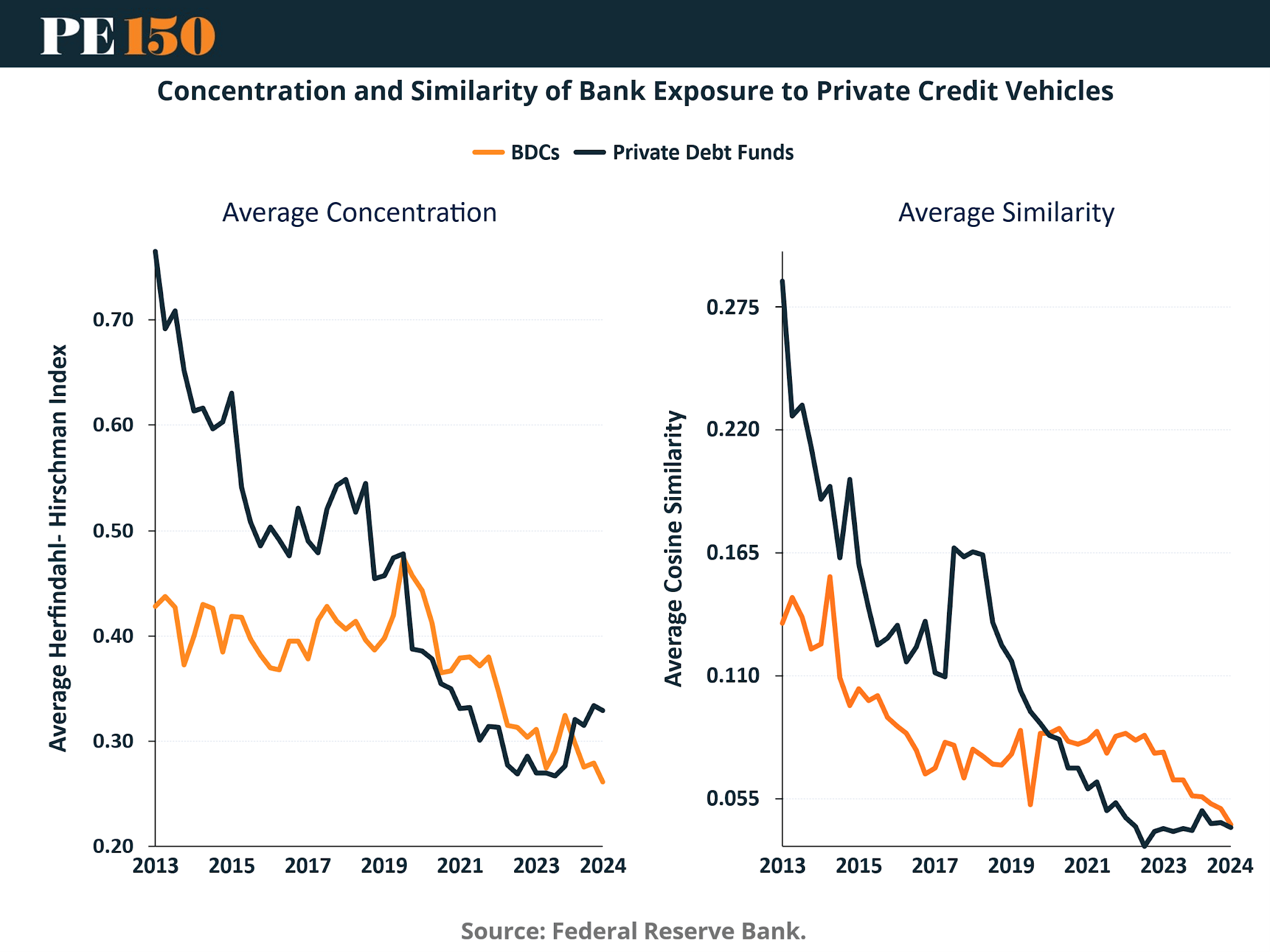

The concentration and diversification of these exposures provide partial mitigation.

Declining concentration and similarity indices indicate that bank exposures to private credit vehicles are not uniformly distributed. This reduces the likelihood that idiosyncratic stress in a single fund or borrower will propagate across the entire banking system.

However, correlated shocks, such as sector-wide stress in software or technology, could still generate synchronized drawdowns, amplifying systemic risk.

5. Liquidity Conditions, Valuations, and Capital Deployment

The broader macro-financial environment plays a critical role in shaping private credit dynamics.

Money supply growth has exhibited significant volatility, with periods of rapid expansion, particularly during and after the COVID-19 shock, followed by sharp contractions.

Elevated liquidity conditions have historically supported asset price inflation and facilitated aggressive capital deployment. The subsequent tightening of liquidity conditions introduces constraints on refinancing and increases the cost of capital, directly impacting leveraged borrowers.

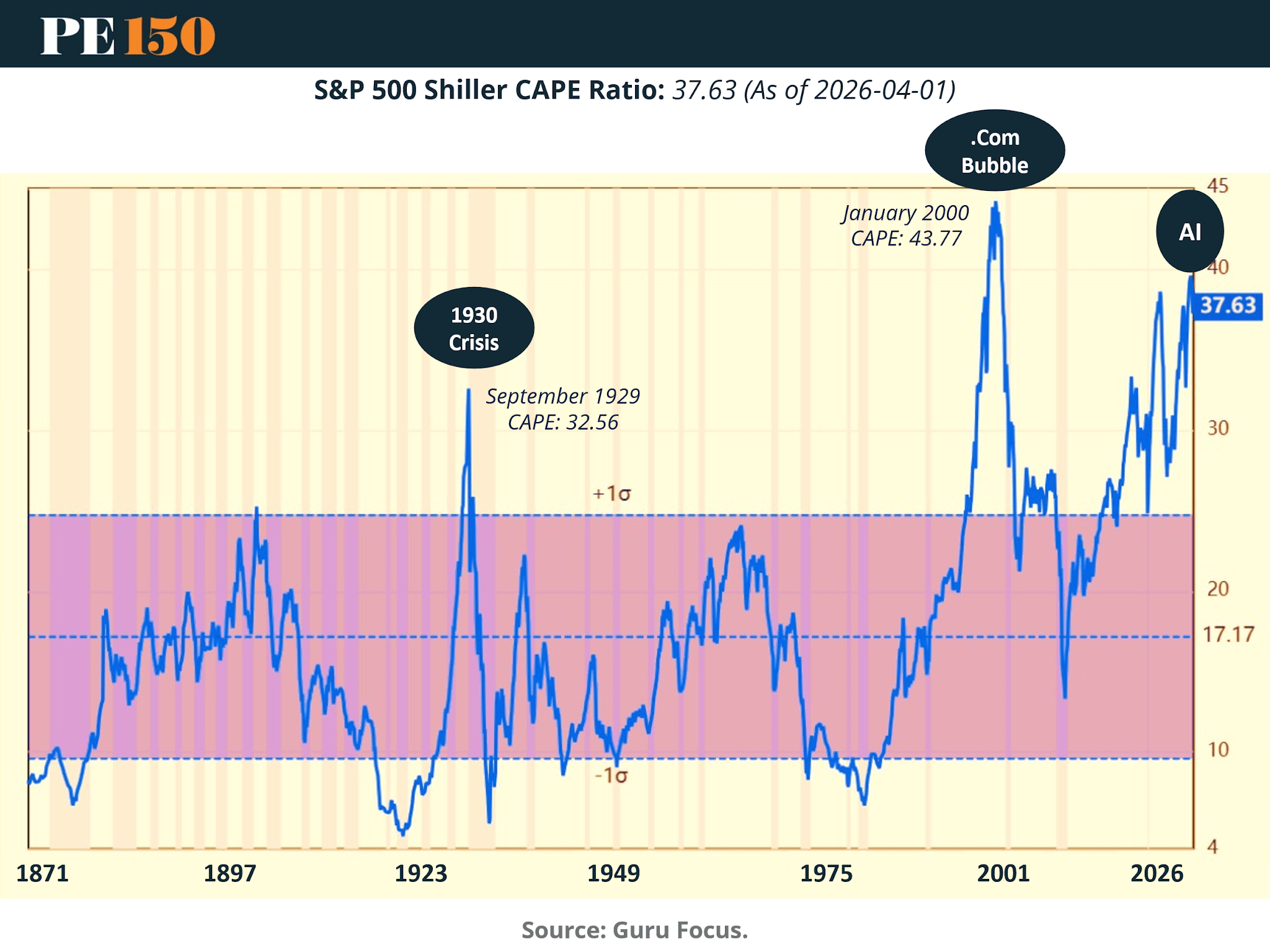

These liquidity dynamics intersect with valuation metrics in public markets.

Valuation multiples, as measured by the Shiller CAPE ratio, are currently elevated relative to long-term averages and comparable to historical peaks observed during periods of technological exuberance. While not directly determinative of private credit outcomes, elevated valuations in public markets often correlate with optimistic growth assumptions and increased risk appetite across asset classes.

In the context of private credit, this environment can lead to underwriting assumptions that may prove sensitive to shifts in growth expectations or discount rates.

The interaction between capital availability and investment behavior is further reflected in private market dynamics.

A substantial portion of private business ownership, estimated at approximately $10 trillion, is concentrated among aging cohorts, creating a structural supply of assets for acquisition and financing. This generational transition intersects with abundant private capital, including private equity and private credit funds, generating sustained demand for leveraged transactions.

The pressure to deploy capital efficiently can compress underwriting standards and increase competition among lenders.

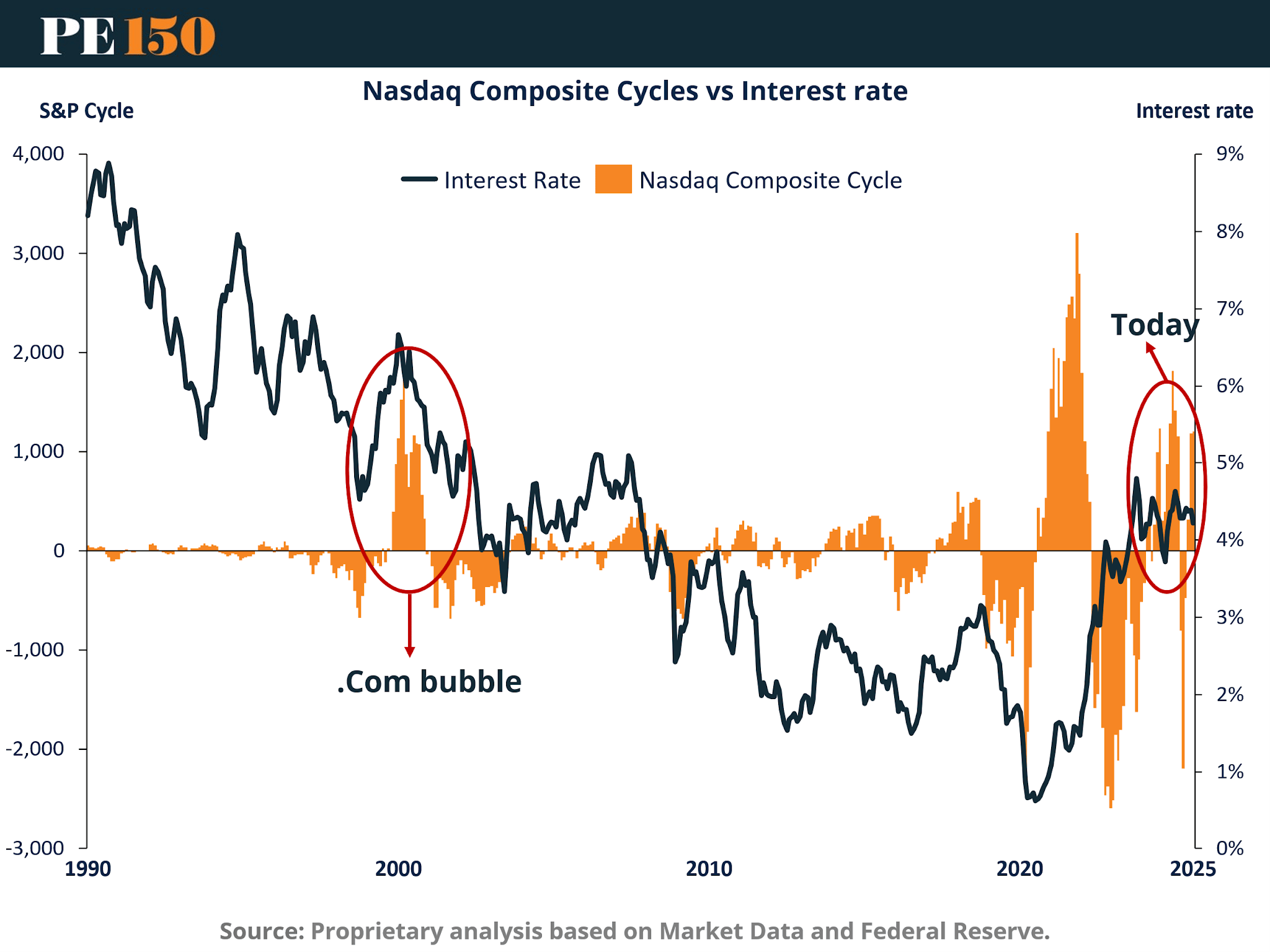

6. Market Cycles, Technology, and Sector Concentration

Technological cycles have historically interacted with financial conditions to shape credit outcomes.

Periods of elevated equity market activity, such as the late-1990s technology cycle and the current AI-driven expansion, have coincided with shifts in interest rate regimes.

The relationship between valuation cycles and monetary conditions underscores the sensitivity of growth-oriented sectors to changes in discount rates and capital availability.

The comparison between historical and current volatility patterns provides additional perspective.

Volatility associated with the current AI cycle appears significantly larger in magnitude than that observed during the .com period, suggesting a more pronounced dispersion of outcomes.

For private credit, where exposure to software and technology sectors is substantial, this increased volatility translates into greater uncertainty around revenue stability and repayment capacity.

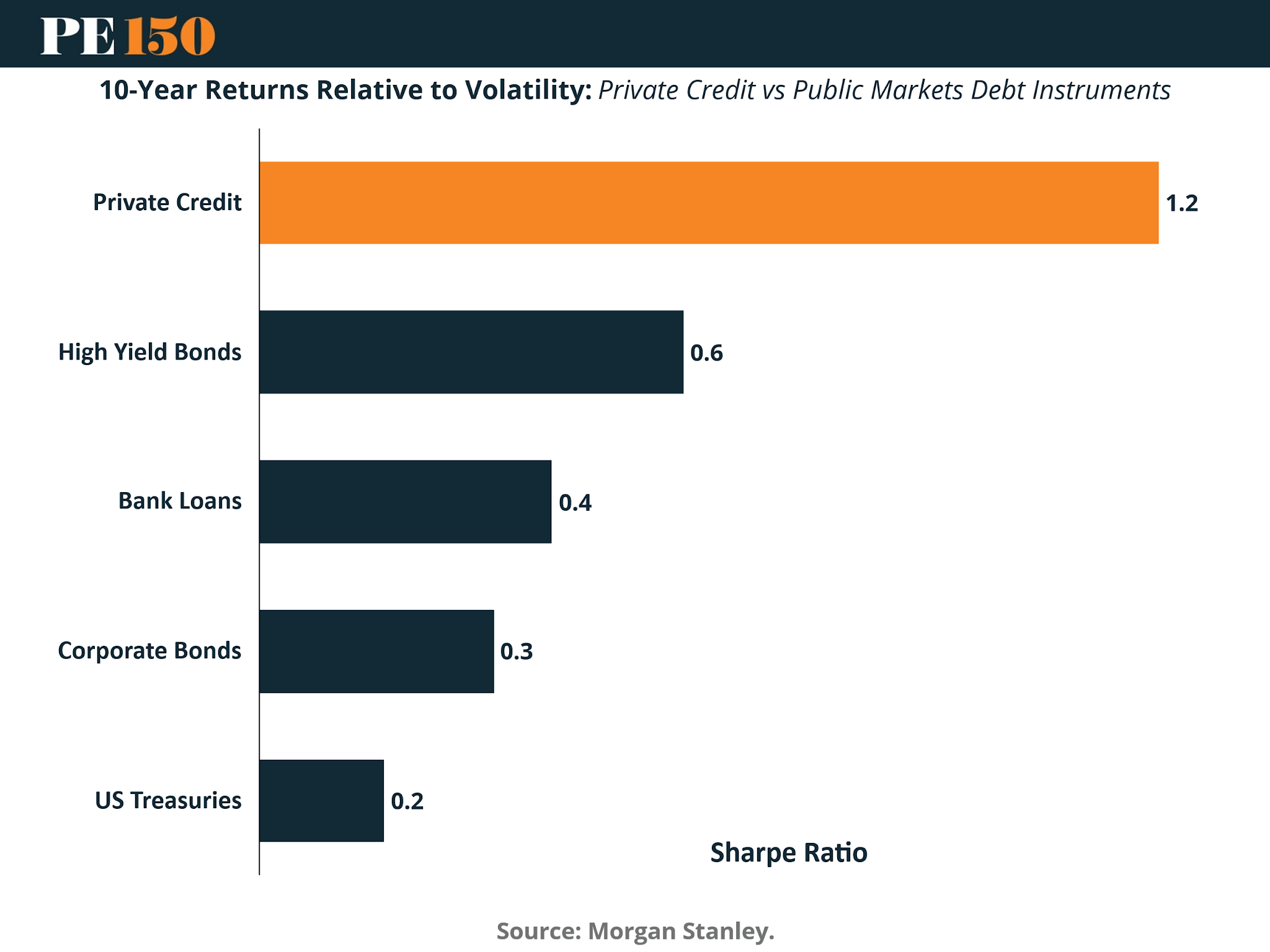

From a portfolio perspective, private credit has historically delivered attractive risk-adjusted returns.

Sharpe ratios indicate that private credit has outperformed traditional fixed income instruments on a risk-adjusted basis over the past decade. However, these metrics are backward-looking and largely reflect a period characterized by low defaults, ample liquidity, and favorable refinancing conditions. As the credit cycle evolves, the persistence of these performance characteristics will depend on the ability of the asset class to navigate higher default rates and more constrained liquidity environments.

Conclusion

Private credit is entering a phase characterized by the normalization of credit conditions after an extended period of benign performance. The structural shift from bank-based to nonbank-based intermediation has redistributed risk across the financial system, altering both its location and its transmission mechanisms. While the funding model of private credit, anchored in long-term, patient capital, mitigates the risk of rapid liquidity-driven contagion, it does not eliminate the accumulation of credit risk.

The data suggest that underlying stress is building gradually. Rising borrower leverage, elevated utilization of credit lines, and the divergence between headline defaults and broader measures of distress all point to a more complex credit environment. At the same time, the increasing interconnection between private credit and banks introduces a channel through which localized credit deterioration could have broader implications, particularly if liquidity demands become synchronized.

Macro-financial conditions further complicate the outlook. Elevated liquidity in recent years has supported aggressive capital deployment and high asset valuations, particularly in sectors linked to technological innovation. As liquidity conditions tighten and growth expectations evolve, the assumptions underpinning many private credit investments may be tested.

The defining feature of the current cycle is therefore not the presence of risk, but its form. Rather than manifesting through abrupt dislocations, risk is likely to emerge through a gradual process of credit deterioration, restructuring, and constrained refinancing capacity. The key variable is not the existence of defaults, but the system’s ability to absorb them without triggering feedback loops across interconnected institutions.

In this context, the trajectory of private credit default rates represents a critical indicator. Not as a signal of imminent systemic stress, but as a measure of how effectively the financial system can transition from a regime of abundant liquidity and low defaults to one characterized by more normalized credit conditions.

Sources & References

Acharya, V. V., N. Cetorelli, and B. Tuckman, 2024, Where Do Banks End and NBFIs Begin? (PDF) Federal Reserve Bank of New York Staff Reports, no. 1119. https://www.newyorkfed.org/medialibrary/media/research/staff_reports/sr1119.pdf

Aldasoro, I. and S. Doerr, 2025, Collateralized lending in private credit, working paper.

AM/PM Podcast. Is The Aggregator Boom a Bust? This Investment Banker Tells All. https://www.ampmpodcast.com/is-the-aggregator-boom-or-a-bust/

Axios. (2026). Why JPMorgan Chase CEO Jamie Dimon isn't sweating private credit. https://www.axios.com/2026/04/06/jpmorgan-chase-jamie-dimon-private-credit

Bank of International Settlements. (2025). Collateralized lending in private credit. https://www.bis.org/publ/work1267.pdf

Bank of International Settlements. (2025). Banks’ interconnections with non-bank financial intermediaries. https://www.bis.org/bcbs/publ/d598.pdf

Bank of International Settlements. (2025). BIS Quarterly Review International banking and financial market developments. https://www.bis.org/publ/qtrpdf/r_qt2503.pdf

Berrospide, Jose, Fang Cai, Siddhartha Lewis-Hayre, and Filip Zikes (2025). "Bank Lending to Private Credit: Size, Characteristics, and Financial Stability Implications," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, May 23, 2025, https://doi.org/10.17016/2380-7172.3802

Bloomberg. (2026). Morgan Stanley Sees Private Credit Default Rates Reaching 8%. https://www.bloomberg.com/news/articles/2026-03-16/private-credit-default-rates-to-reach-8-morgan-stanley-says?embedded-checkout=true

Business Insider. (2026). Jamie Dimon warns of a 'skunk at the party' for markets if inflation builds. https://www.businessinsider.com/jamie-dimon-jpmorgan-inflation-warning-economy-shareholder-letter-2026-4

Cai, F., and S. Haque, 2024, Private Credit: Characteristics and Risks, FEDS Notes. Washington: Board of Governors of the Federal Reserve System. https://www.federalreserve.gov/econres/notes/feds-notes/private-credit-characteristics-and-risks-20240223.html

Capital Brief. (2026). Jamie Dimon warns private credit losses may be larger than expected. https://www.capitalbrief.com/briefing/jamie-dimon-warns-private-credit-losses-may-be-larger-than-expected-5d844968-495b-4af1-af6f-9ec319541d1d/

Central Banking. (2026). Powell: We do not see systemic risks from private credit. https://www.centralbanking.com/central-banks/financial-stability/7975526/powell-we-do-not-see-systemic-risks-from-private-credit?check_logged_in=1

CNBC. (2026). Private credit’s ‘zero-loss fantasy’ is coming to an end as defaults and fund exits rise. https://www.cnbc.com/2026/03/25/private-credit-defaults-loan-quality-debt-risk-systemic-ai-disruption.html

CEPRES. (2025). Private Credit Outlook for 2025. https://a.storyblok.com/f/152404/x/0be95e431c/cepres-private-credit-outlook-2025.pdf?cv=1733234783687

Fitch. (2026). U.S. Private Credit Default Rate Continues Upward March to 5.8% in January 2026. https://www.fitchratings.com/research/corporate-finance/us-private-credit-default-rate-continues-upward-march-to-5-8-in-january-2026-23-02-2026#:~:text=Fitch%20Ratings%2DAustin/New%20York,defaulters%20generated%2089%20default%20events

Guru Focus. (2026). S&P 500 Shiller CAPE Ratio. https://www.gurufocus.com/economic_indicators/56/sp-500-shiller-cape-ratio

IMF. (2025). Growth of Nonbanks is Revealing New Financial Stability Risks. https://www.imf.org/en/blogs/articles/2025/10/14/growth-of-nonbanks-is-revealing-new-financial-stability-risks

McKinsey. (2024). The next era of private credit. https://www.mckinsey.com/industries/private-capital/our-insights/the-next-era-of-private-credit

Morgan Stanley. (2025). Understanding Private Credit’s Rapid Growth. https://www.morganstanley.com/ideas/private-credit-outlook-considerations

PE150. (2025). Banking Sector Retrenchment Created Tailwinds for Private Credit. https://www.pe150.com/p/banking-sector-retrenchment-created-tailwinds-for-private-credit-f83d

PE150. (2026). Private Credit Risk: Slow-Burning Stress in a Fast-Moving Capital Cycle. https://www.pe150.com/p/private-credit-risk-slow-burning-stress-in-a-fast-moving-capital-cycle

PE150. (2026). The Rise of New Products in the Private Markets. https://www.pe150.com/p/the-rise-of-new-products-in-the-private-markets

Reuters. (2026). Fed watching private credit sector for signs of trouble, Powell says. https://www.reuters.com/business/finance/fed-watching-private-credit-sector-signs-trouble-powell-says-2026-03-30/

Reuters. (2026). Private credit sector stresses could be catastrophic, but not just yet. https://www.reuters.com/business/finance/private-credit-sector-stresses-could-be-catastrophic-not-just-yet-2026-04-03/

Yahoo Finance. (2026). Fed Chair Powell sees no threat of private credit 'contagion,' says interest rates are in a 'good place'. https://finance.yahoo.com/news/fed-chair-powell-sees-no-threat-of-private-credit-contagion-says-interest-rates-are-in-a-good-place-165159434.html?guccounter=1&guce_referrer=aHR0cHM6Ly93d3cuZ29vZ2xlLmNvbS8&guce_referrer_sig=AQAAAGGFIBfw2cG2iQjh9ioNQSkQuqjjsPlVZxuV8tR8buoqswed8kOuBvEj_7YzH_6YA5BJGAPTXcCUyQp0JjCHlWseIDTjqWWrz-wjOqyEDvfN9mzxhUR5MoJsYG6-QB5DkdmAc8c_ZyJ_Bn0cc0Em7T4hTK_l_gpSTExMueEnCZDC