- PE 150

- Posts

- Private Credit Risk: Slow-Burning Stress in a Fast-Moving Capital Cycle

Private Credit Risk: Slow-Burning Stress in a Fast-Moving Capital Cycle

Private credit has evolved from a niche financing channel into a core component of institutional portfolios. Its expansion has been underpinned by a structural shift: banks retrenching from middle-market lending and long-duration capital stepping in to fill the gap. That architecture—long-term investors funding long-term loans—has shaped both the resilience and the risk profile of the asset class.

Today, the key question is not whether risk exists, but how it manifests. The answer is increasingly tied to the pace of capital deployment, particularly into sectors facing technological disruption and elevated leverage. Artificial intelligence investment is accelerating capital expenditure cycles, compressing timelines for funding and refinancing, and placing pressure on borrowers whose business models were underwritten in a lower-rate, lower-disruption environment.

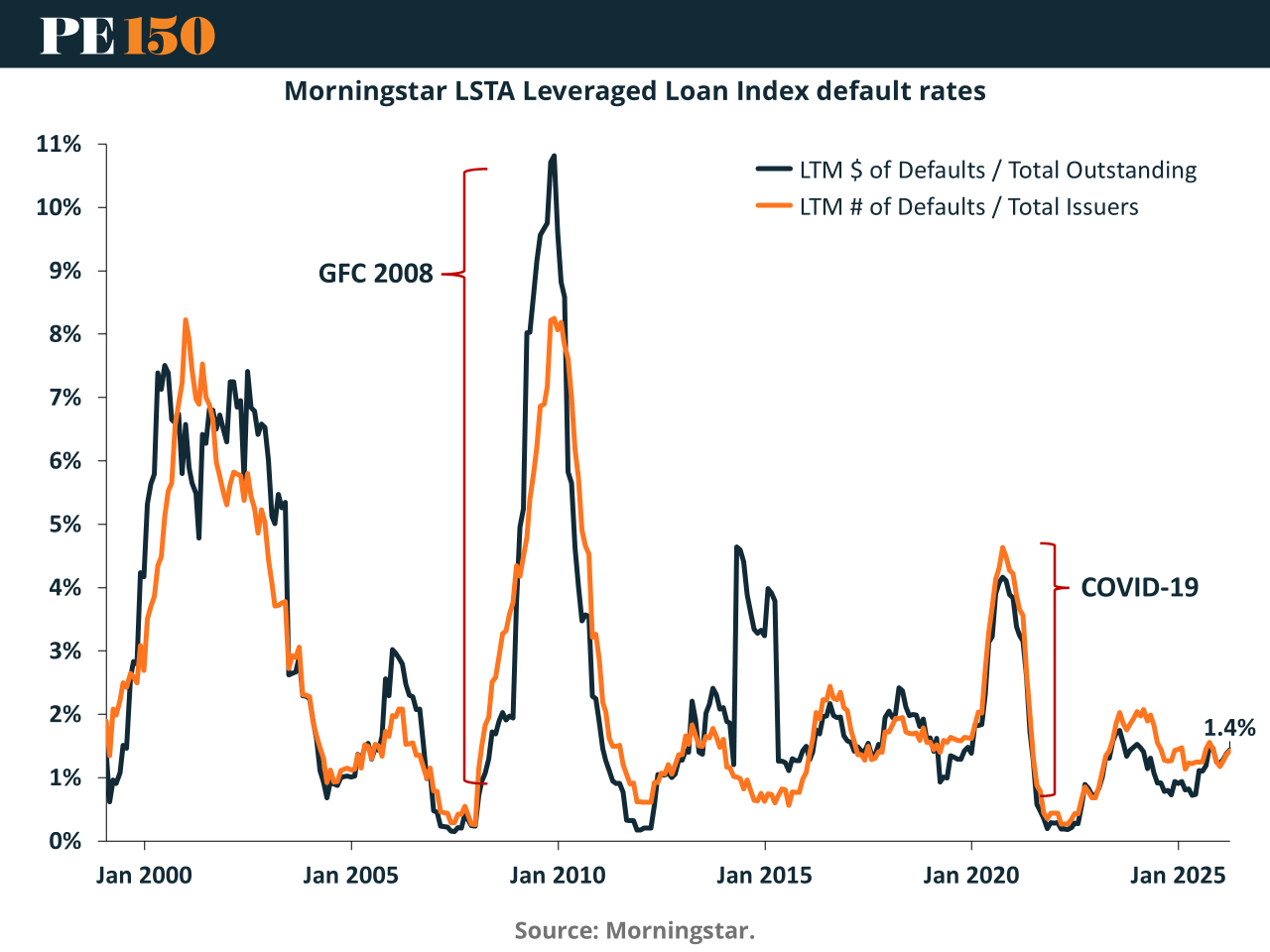

Default Cycles Are Normalising—Not Disappearing

Default rates across leveraged loans provide a useful benchmark for credit cycles. Historically, stress episodes—such as the Global Financial Crisis and the pandemic—produced sharp spikes in defaults, followed by relatively rapid normalization. Current levels remain far below systemic peaks but have begun to trend upward.

This pattern matters. Private credit has, for much of the past decade, operated under benign conditions: low rates, abundant liquidity, and strong refinancing capacity. That environment allowed for aggressive underwriting assumptions, higher leverage, and covenant flexibility. As rates remain elevated and growth expectations shift—particularly in AI-exposed sectors—those assumptions are being tested.

The emerging increase in defaults is therefore less an anomaly than a reversion to a more typical credit regime. Importantly, much of this stress is not expressed through immediate bankruptcies, but through softer forms of distress: payment-in-kind interest, maturity extensions, and restructurings. These mechanisms delay recognition but do not eliminate underlying risk.

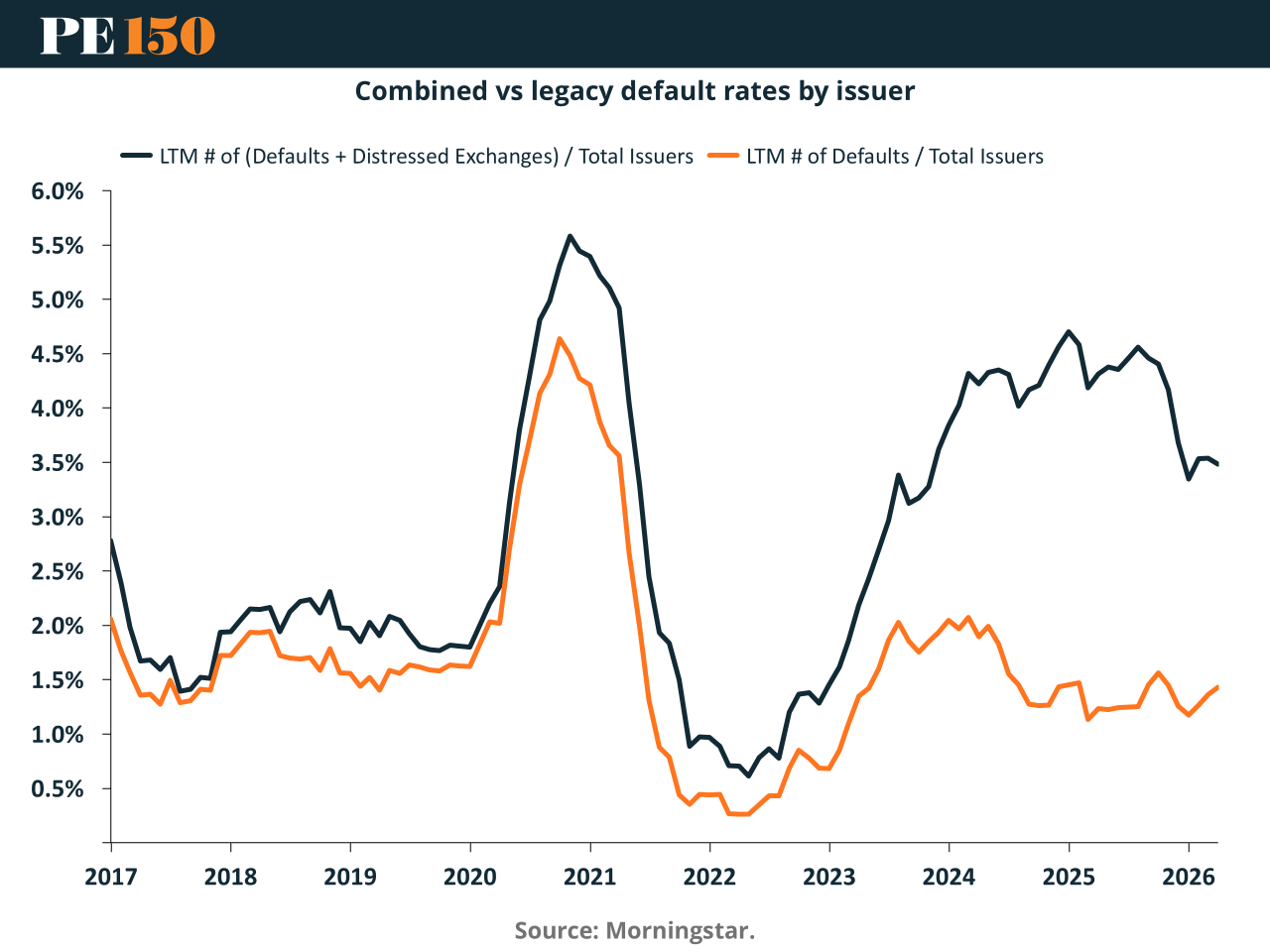

Issuer-Level Stress Is Building Beneath the Surface

At the issuer level, a divergence is visible between headline defaults and broader measures of distress. When distressed exchanges and restructurings are included, effective default rates are materially higher than traditional metrics suggest.

This gap highlights a defining feature of private credit: loss recognition is gradual. Rather than immediate default events, lenders and sponsors often employ “extend and amend” strategies to stabilize borrowers. While this reduces short-term volatility, it can obscure the true extent of credit deterioration.

The current cycle reflects several compounding pressures:

Higher leverage accumulated during the low-rate period

Rising interest costs, particularly for floating-rate structures

Sector concentration, notably in software and technology

AI-driven disruption, which is altering revenue visibility and competitive dynamics

These factors do not produce instant systemic shocks, but they do increase the probability of cumulative losses over time.

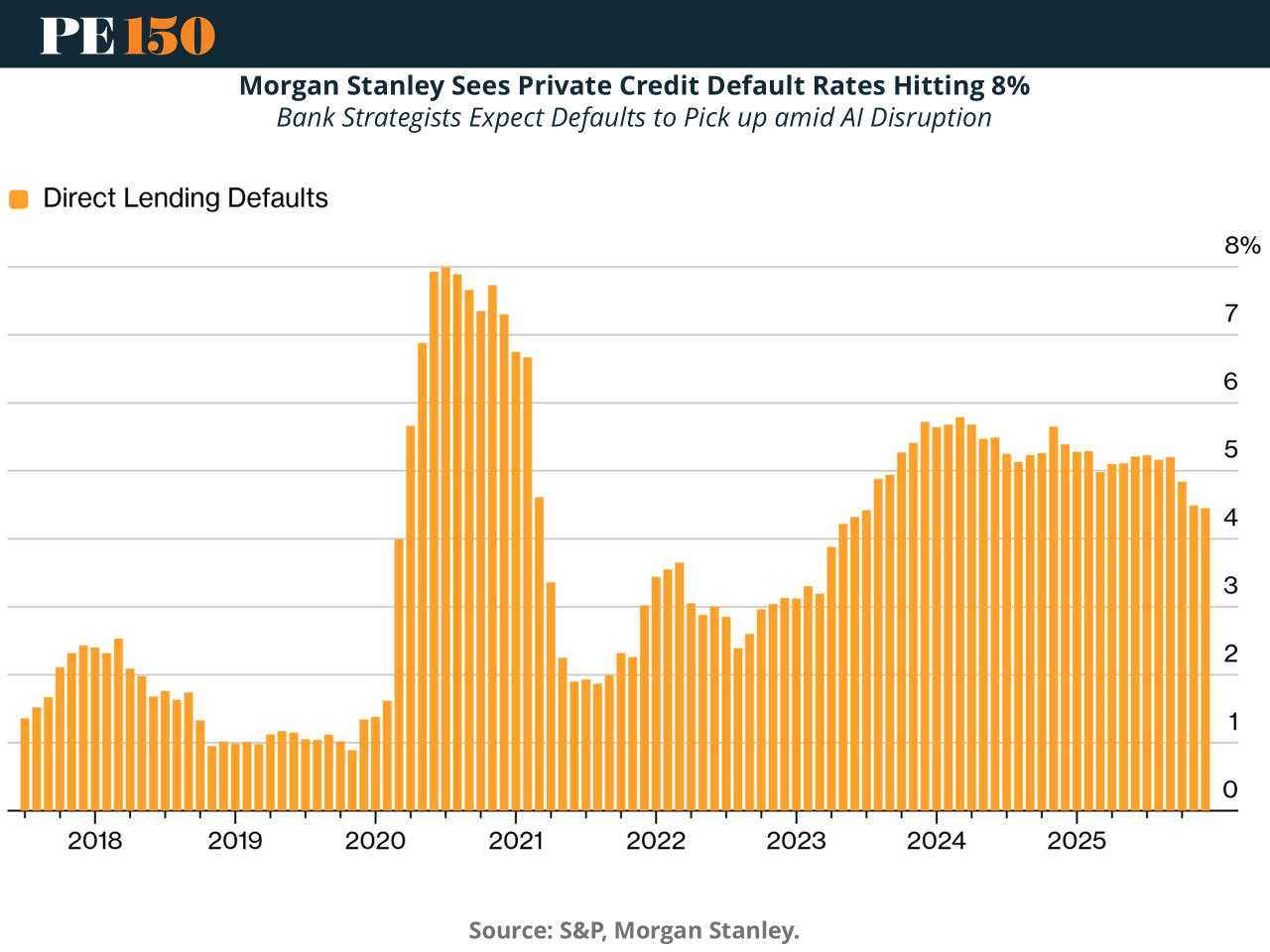

AI Investment: A Catalyst for Funding Imbalance

The acceleration of AI investment introduces a new dimension to private credit risk. Capital is being deployed rapidly into sectors where long-term outcomes remain uncertain. In software, where private credit exposure is significant, leverage is high and coverage ratios are thin.

This creates a structural tension:

Capital is being committed quickly, often ahead of proven cash-flow durability

Borrowers face near-term refinancing needs, with a front-loaded maturity wall

Revenue models may be disrupted, reducing repayment capacity

Under these conditions, default rates could rise meaningfully toward levels last seen during stress episodes. In more adverse scenarios, the interaction between technological disruption and financial leverage could amplify losses.

However, the mechanism remains fundamentally credit-driven. Unlike liquidity crises, which can trigger immediate dislocations, this type of stress unfolds through earnings erosion, refinancing difficulty, and gradual impairment of borrower quality.

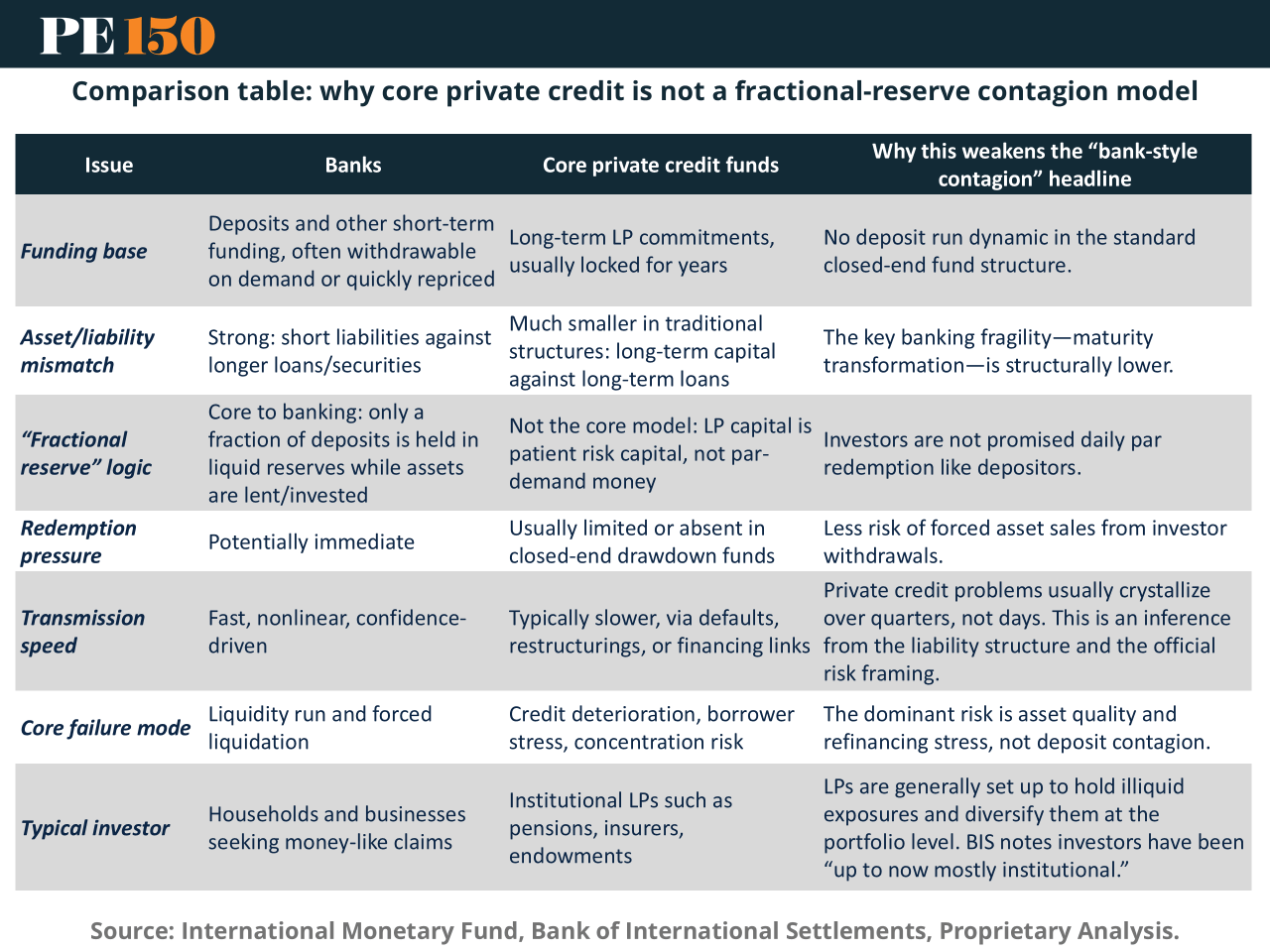

The Core Structure Limits Rapid Contagion

A central distinction between private credit and banking lies in funding structure. Banks operate with short-term, runnable liabilities funding long-term assets—a configuration inherently vulnerable to liquidity shocks. Private credit, by contrast, is largely funded by long-term commitments from institutional investors.

This alignment produces several stabilizing features:

No deposit run dynamic: investors cannot redeem capital on demand

Lower maturity mismatch: assets and liabilities are broadly aligned

Slower transmission of stress: losses emerge through credit deterioration rather than funding withdrawal

Private credit does not replicate the core fragility of fractional-reserve banking. Contagion, when it occurs, is therefore unlikely to be sudden or nonlinear. Instead, it manifests as a gradual tightening of credit conditions, reduced lending capacity, and delayed loss recognition.

This does not eliminate risk. It changes its tempo.

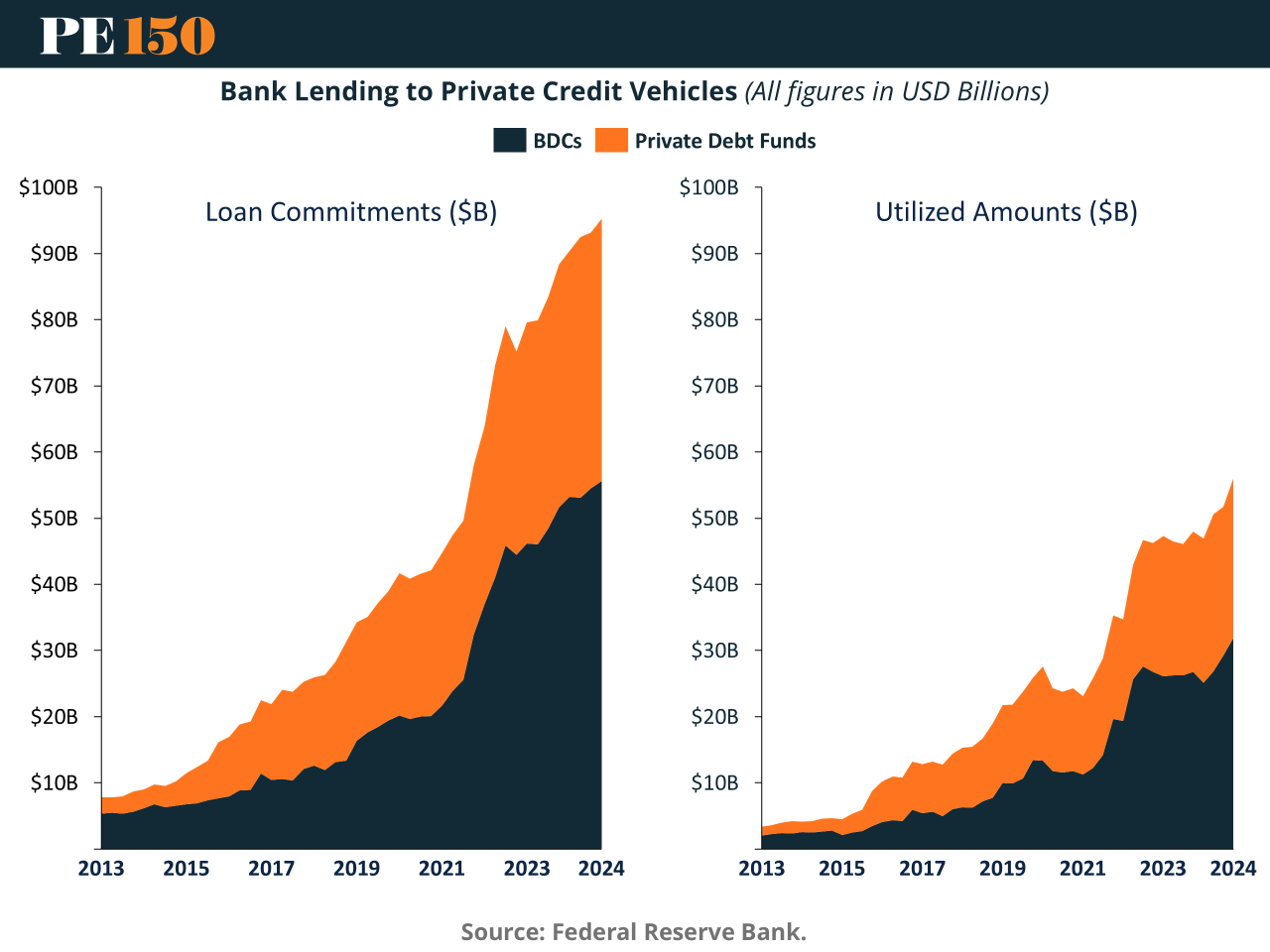

The Real Systemic Channel: Banks

The most important systemic linkage is not within private credit itself, but between private credit and banks. Bank lending to private credit vehicles—through credit lines, warehouse financing, and partnerships—has grown significantly over the past decade.

This introduces a second-order risk:

Private credit funds rely on banks for liquidity and leverage

Banks are exposed to private credit through direct lending and structured relationships

Stress in private credit can therefore transmit indirectly into the banking system

While current exposure levels remain manageable relative to bank balance sheets, the direction of travel is clear. As private credit scales, so too does its integration with regulated institutions.

The risk scenario is not a classic bank run. It is a synchronized drawdown of credit lines, combined with deterioration in underlying loan performance. In such a scenario, banks would face pressure on both capital and liquidity, particularly if multiple private credit vehicles require support simultaneously.

This places responsibility squarely on banks’ balance sheet management. The principle is straightforward:

borrow long and lend long.

If banks fund long-duration exposures with short-term liabilities—or extend liquidity without appropriate capital buffers—the system becomes vulnerable not because of private credit itself, but because of how it is financed.

Liquidity Illusion and Redemption Pressure

Recent episodes of capped redemptions in semi-liquid vehicles highlight another emerging tension. While traditional private credit funds are closed-end, newer structures offer periodic liquidity, creating a partial mismatch between investor expectations and asset reality.

This dynamic introduces:

Redemption pressure during stress periods

Potential gating mechanisms, which can erode investor confidence

A shift in investor base, from retail-like flows to institutional capital

However, even here, the impact remains contained relative to banking systems. Liquidity constraints are managed through fund structures rather than forced asset sales, limiting immediate spillovers.

Conclusion: Risk Is Real, but Its Form Matters

Private credit is entering a more challenging phase. Defaults are rising, underwriting standards are being tested, and rapid capital deployment—particularly into AI-driven sectors—is exposing vulnerabilities.

Yet the nature of the risk is often misunderstood.

This is not a system prone to sudden collapse through liquidity contagion. It is a system where:

Losses accumulate gradually

Stress is absorbed through restructurings

Capital remains largely locked in place

The primary systemic concern lies at the interface with banks. As interconnections deepen, the risk of indirect contagion increases—not through depositor runs, but through balance sheet linkages and funding dependencies.

The appropriate stance is neither alarmist nor complacent. Private credit is not a replication of banking fragility. But neither is it insulated from the broader financial system.

The cycle ahead will likely be defined by a simple reality: when capital moves faster than credit quality, risk does not disappear—it is merely deferred.

Sources & References

Acharya, V. V., N. Cetorelli, and B. Tuckman, 2024, Where Do Banks End and NBFIs Begin? (PDF) Federal Reserve Bank of New York Staff Reports, no. 1119. https://www.newyorkfed.org/medialibrary/media/research/staff_reports/sr1119.pdf

Aldasoro, I. and S. Doerr, 2025, Collateralized lending in private credit, working paper.

AM/PM Podcast. Is The Aggregator Boom a Bust? This Investment Banker Tells All. https://www.ampmpodcast.com/is-the-aggregator-boom-or-a-bust/

Axios. (2026). Why JPMorgan Chase CEO Jamie Dimon isn't sweating private credit. https://www.axios.com/2026/04/06/jpmorgan-chase-jamie-dimon-private-credit

Bank of International Settlements. (2025). Banks’ interconnections with non-bank financial intermediaries. https://www.bis.org/bcbs/publ/d598.pdf

Bank of International Settlements. (2025). BIS Quarterly Review International banking and financial market developments. https://www.bis.org/publ/qtrpdf/r_qt2503.pdf

Berrospide, Jose, Fang Cai, Siddhartha Lewis-Hayre, and Filip Zikes (2025). "Bank Lending to Private Credit: Size, Characteristics, and Financial Stability Implications," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, May 23, 2025, https://doi.org/10.17016/2380-7172.3802

Bloomberg. (2026). Morgan Stanley Sees Private Credit Default Rates Reaching 8%. https://www.bloomberg.com/news/articles/2026-03-16/private-credit-default-rates-to-reach-8-morgan-stanley-says?embedded-checkout=true

Business Insider. (2026). Jamie Dimon warns of a 'skunk at the party' for markets if inflation builds. https://www.businessinsider.com/jamie-dimon-jpmorgan-inflation-warning-economy-shareholder-letter-2026-4

Cai, F., and S. Haque, 2024, Private Credit: Characteristics and Risks, FEDS Notes. Washington: Board of Governors of the Federal Reserve System. https://www.federalreserve.gov/econres/notes/feds-notes/private-credit-characteristics-and-risks-20240223.html

Capital Brief. (2026). Jamie Dimon warns private credit losses may be larger than expected. https://www.capitalbrief.com/briefing/jamie-dimon-warns-private-credit-losses-may-be-larger-than-expected-5d844968-495b-4af1-af6f-9ec319541d1d/

Central Banking. (2026). Powell: We do not see systemic risks from private credit. https://www.centralbanking.com/central-banks/financial-stability/7975526/powell-we-do-not-see-systemic-risks-from-private-credit?check_logged_in=1

CNBC. (2026). Private credit’s ‘zero-loss fantasy’ is coming to an end as defaults and fund exits rise. https://www.cnbc.com/2026/03/25/private-credit-defaults-loan-quality-debt-risk-systemic-ai-disruption.html

Fitch. (2026). U.S. Private Credit Default Rate Continues Upward March to 5.8% in January 2026. https://www.fitchratings.com/research/corporate-finance/us-private-credit-default-rate-continues-upward-march-to-5-8-in-january-2026-23-02-2026#:~:text=Fitch%20Ratings%2DAustin/New%20York,defaulters%20generated%2089%20default%20events

IMF. (2025). Growth of Nonbanks is Revealing New Financial Stability Risks. https://www.imf.org/en/blogs/articles/2025/10/14/growth-of-nonbanks-is-revealing-new-financial-stability-risks

Morgan Stanley. (2025). Understanding Private Credit’s Rapid Growth. https://www.morganstanley.com/ideas/private-credit-outlook-considerations

Reuters. (2026). Fed watching private credit sector for signs of trouble, Powell says. https://www.reuters.com/business/finance/fed-watching-private-credit-sector-signs-trouble-powell-says-2026-03-30/

Reuters. (2026). Private credit sector stresses could be catastrophic, but not just yet. https://www.reuters.com/business/finance/private-credit-sector-stresses-could-be-catastrophic-not-just-yet-2026-04-03/

Yahoo Finance. (2026). Fed Chair Powell sees no threat of private credit 'contagion,' says interest rates are in a 'good place'. https://finance.yahoo.com/news/fed-chair-powell-sees-no-threat-of-private-credit-contagion-says-interest-rates-are-in-a-good-place-165159434.html?guccounter=1&guce_referrer=aHR0cHM6Ly93d3cuZ29vZ2xlLmNvbS8&guce_referrer_sig=AQAAAGGFIBfw2cG2iQjh9ioNQSkQuqjjsPlVZxuV8tR8buoqswed8kOuBvEj_7YzH_6YA5BJGAPTXcCUyQp0JjCHlWseIDTjqWWrz-wjOqyEDvfN9mzxhUR5MoJsYG6-QB5DkdmAc8c_ZyJ_Bn0cc0Em7T4hTK_l_gpSTExMueEnCZDC