- PE 150

- Posts

- The Math Of Compounding, And Why Markets Are Suddenly Nervous

The Math Of Compounding, And Why Markets Are Suddenly Nervous

The hidden arithmetic behind market optimism, volatility, and sudden fear.

Good morning, ! This week we analyze the mathematics behind different compounding strategies, time horizons, and volatility profiles. Meanwhile, 2025 closed with the second-highest Global Buyout deal value of the past decade, signaling a strong recovery in this segment. Looking ahead, markets are showing signs of anxiety as geopolitical tensions in the Middle East raise concerns about potential disruption to the Strait of Hormuz.

Sponsor Spotlight: Juniper Square presents a new report on the rise of modern fund formats — breaking down what’s driving GPs beyond traditional closed-end structures and why shifting investor profiles, liquidity expectations, and faster operating cadences are changing what “good operations” looks like. Get the report →

DATA DIVE

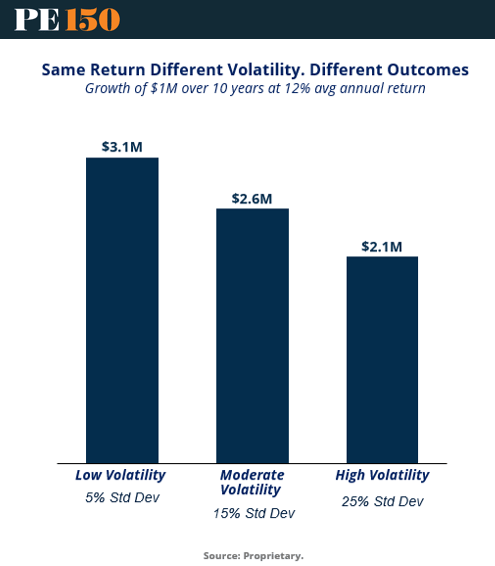

Consistency Beats Volatility

Stat: Three portfolios each delivering 12% average annual returns produced dramatically different outcomes over ten years. A $1M portfolio grew to $3.1M with 5% volatility, $2.6M with 15% volatility, and just $2.1M with 25% volatility.

Context: The divergence comes from a mathematical reality investors often underestimate. Returns compound geometrically, not arithmetically. As volatility rises, the realized growth rate falls due to volatility drag. Even when the average return is identical, variability reduces compounding efficiency. Drawdowns worsen the effect. A 25% loss requires a 33% gain just to break even, meaning recovery consumes years that could otherwise compound forward. Historical crashes show the time cost clearly. The Dot Com Bust fell roughly 49% and took about 4.5 years to recover, while the Global Financial Crisis dropped about 57% and required roughly four years to regain prior levels.

Strategic Takeaway: For private equity investors, the lesson is structural. Long term wealth is not maximized by chasing the highest return but by maximizing return stability. Strategies with smoother valuation paths, controlled drawdowns, and reinvestable cash flow protect the compounding engine that ultimately drives portfolio value. (Read the Full Report Here)

TREND TO WATCH

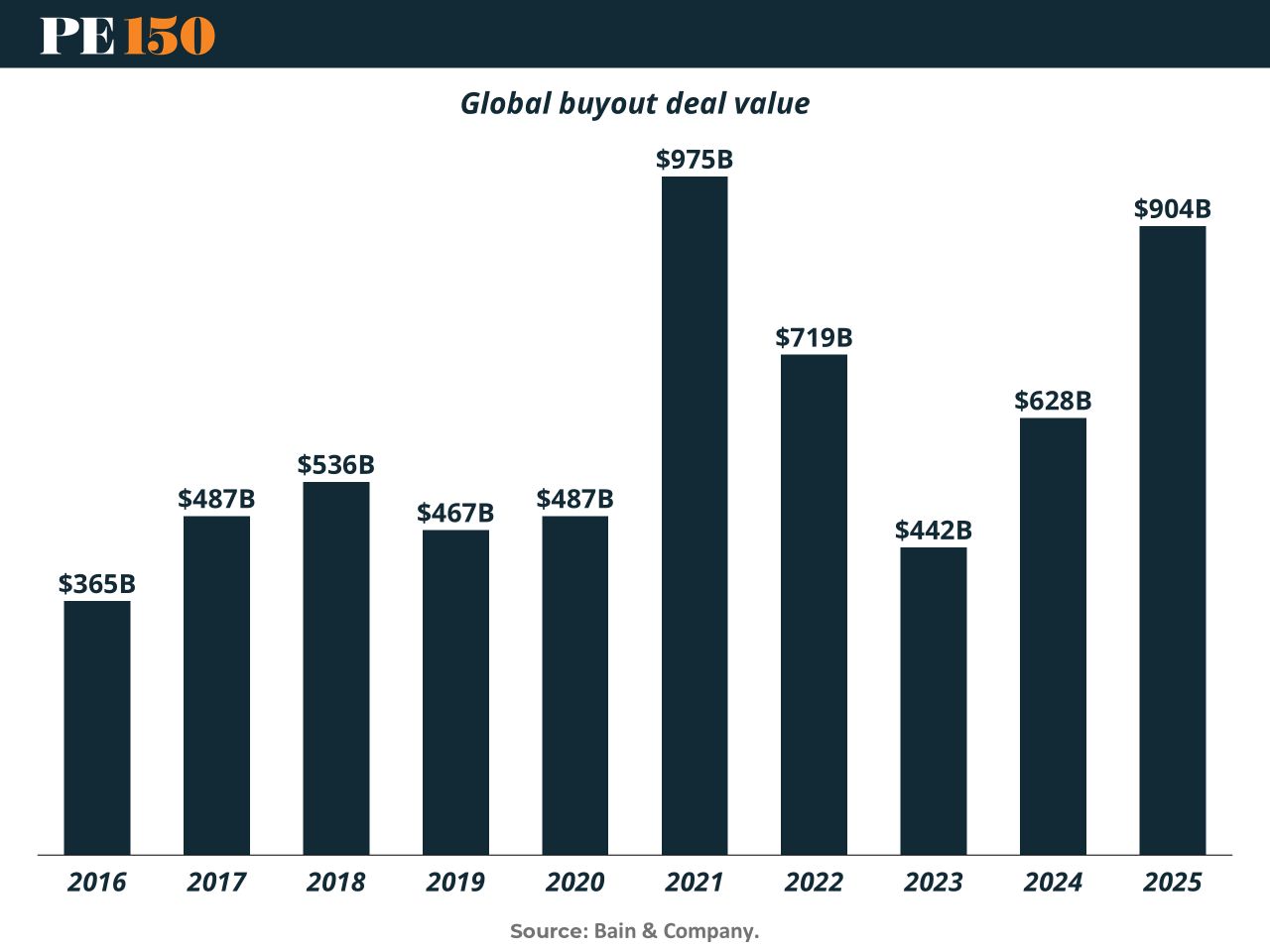

Buyouts Are Back (Almost)

After two slow years, global buyout dealmaking is finally showing signs of life.

According to Preqin, buyout deal value is projected to reach $904B in 2025, a 44% jump from $628B in 2024. If realized, that would mark the strongest year since the 2021 peak, when cheap financing and abundant liquidity pushed deal value to $975B.

The rebound follows a sharp reset. Deal value dropped from $719B in 2022 to $442B in 2023, as higher interest rates, tight credit markets, and valuation gaps stalled transactions.

Now the gears are slowly turning again. Financing markets are reopening, aging dry powder is pushing GPs to deploy, and buyer–seller pricing expectations are starting to converge.

The key caveat: this isn’t 2021 again. Pricing discipline and operational value creation remain the focus. (More)

PRESENTED BY JUNIPER SQUARE

The private markets have evolved beyond traditional closed-end funds. More GPs are launching new fund structures tailored to different investor profiles with different liquidity expectations and faster operating cadences.

That shift changes what “good operations” looks like. Investor onboarding, servicing, reporting, and communications cannot be treated as a series of handoffs across point solutions, as disconnection creates friction, inconsistency, and slower decision-making.

With all these new fund structures in play, the operating model decides who scales and who stalls. Connected fund and investor data turns execution into a competitive advantage — giving teams the speed, precision, and confidence to scale without adding friction.

Download the report to understand what’s driving the rise of new fund structures and the operational implications for GPs.

Supporting our sponsors supports our free newsletters. Please support our sponsors!

COMPLIANCE CORNER

ERISA Capital Is Opening Up. The Compliance Bar Is Rising.

Private equity has long treated ERISA capital as a regulatory puzzle. The familiar constraint is the 25% benefit plan investor threshold, which determines whether a fund’s assets become subject to ERISA fiduciary rules. Cross that line and the GP effectively inherits pension level duties across the portfolio.

Recent regulatory signals suggest the door to retirement capital is opening slightly wider. Clarifications around fiduciary advice rules and prohibited transaction exemptions now require written fiduciary acknowledgments and clearer conflict disclosure when advising ERISA accounts. At the same time, refinements to the benefit plan investor definition exclude certain non ERISA vehicles, giving managers more room to accept retirement capital without triggering plan asset status.

Opportunity comes with sharper scrutiny. Enforcement attention in 2025 has centered on fiduciary process rather than investment outcomes. Regulators and litigators are examining valuation methodology, fee transparency, and documented diligence for illiquid strategies such as buyouts.

For PE firms, the takeaway is simple. Access to pension capital is expanding, but the operational burden is rising in parallel. The firms that win this capital will not just deliver returns. They will demonstrate institutional grade governance around monitoring, disclosures, and fiduciary documentation. (More)

LIQUIDITY CORNER

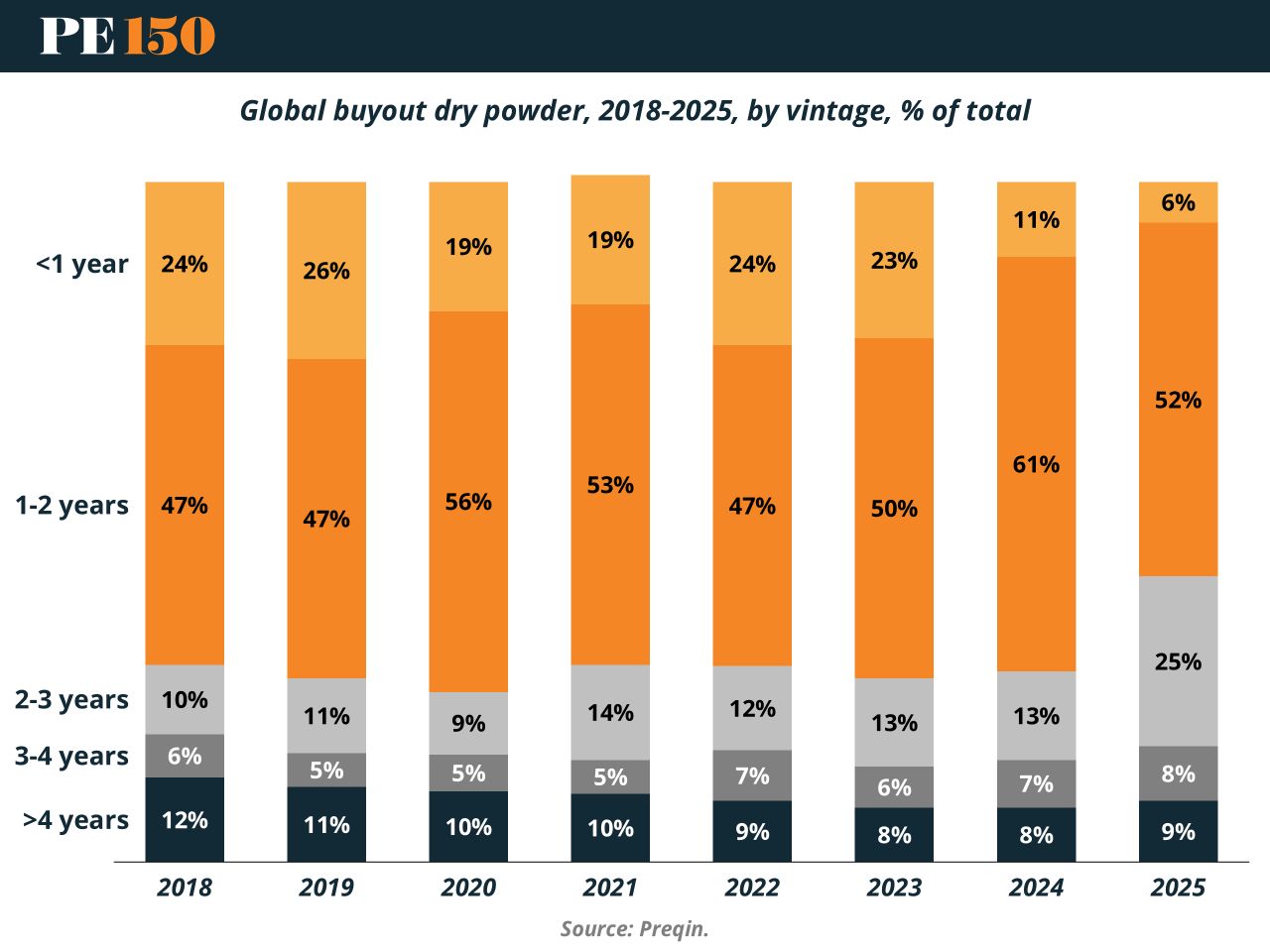

The Dry Powder Clock

Private equity dry powder isn’t just large — it’s aging. And that changes the calculus.

According to Preqin, the share of fresh capital (<1 year old) has dropped sharply, falling from ~24–26% of global buyout dry powder in 2018–2019 to just 6% in 2025. Meanwhile, the 1–2 year vintage bucket now represents 52% of available capital, meaning a large portion of funds raised during the 2022–2023 fundraising boom has entered its core deployment window.

Even more notable: 2–3 year-old capital has surged to 25%, nearly doubling year-over-year. Combined with older vintages, 42% of buyout dry powder is now more than two years old.

Why it matters: PE funds typically deploy capital within four to five years, meaning the investment clock is ticking.

The likely result? Rising deployment pressure, more competition for deals, and potentially tighter pricing spreads if markets reopen. (More)

MACROVIEW

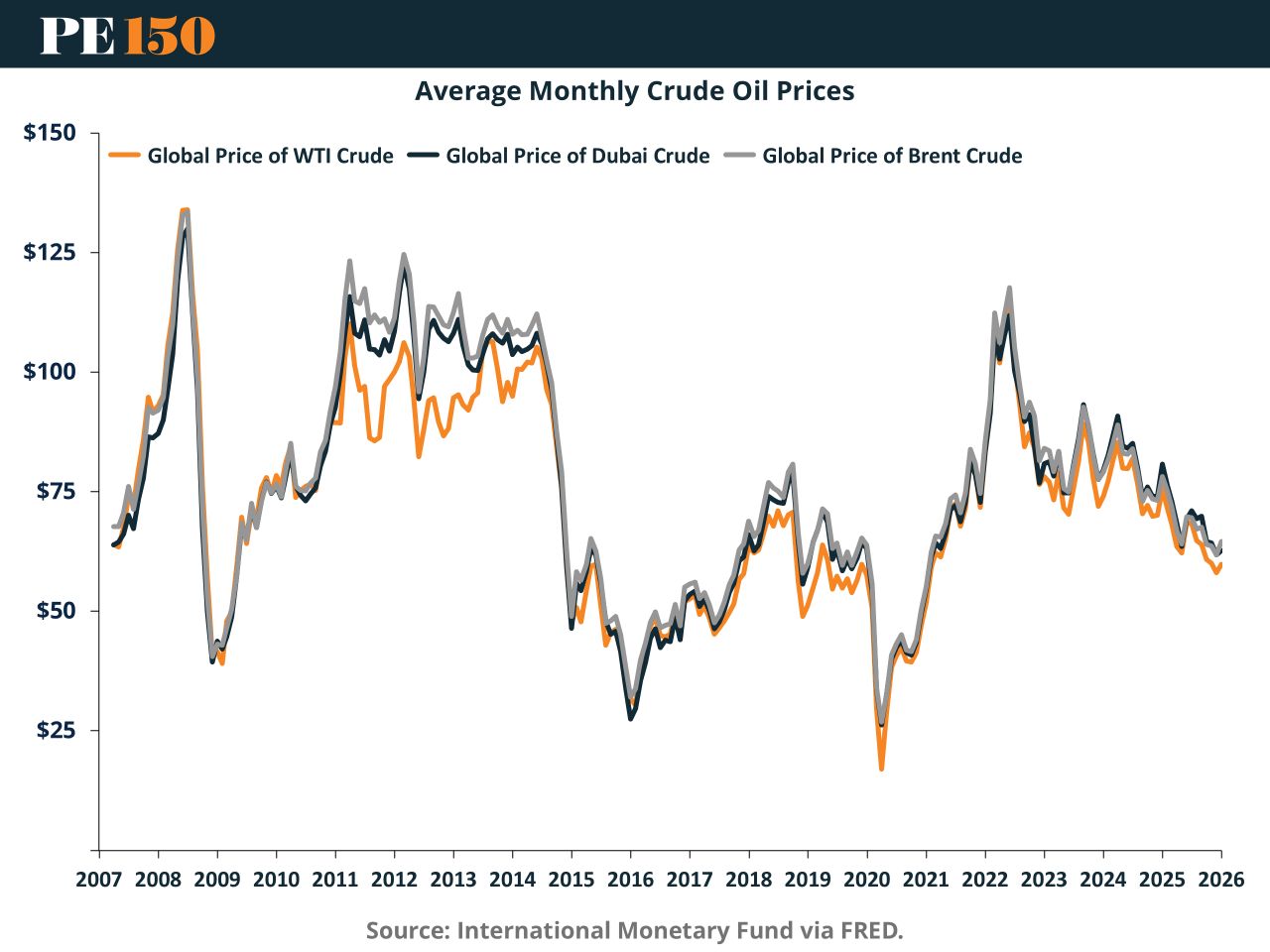

The $90 Oil Warning

Geopolitics is back in the driver’s seat of energy markets. Following escalating tensions between Iran, the U.S., and Israel, oil traders are increasingly pricing in the risk of a major supply disruption centered around the Strait of Hormuz—one of the most critical chokepoints in global energy trade.

The stakes are enormous: roughly 20 million barrels per day—about 20% of global oil consumption—normally pass through the strait. With tanker traffic restricted and Gulf infrastructure under threat, futures markets are already reacting. WTI crude jumped more than 10% in a single week, while Brent prices have climbed toward the low $90s per barrel.

The chart above illustrates how tightly integrated oil markets are. WTI, Brent, and Dubai crude prices move almost in lockstep, reflecting what economists call the “global bathtub” effect—supply disruptions in one region quickly ripple across the entire market. Even localized geopolitical shocks historically trigger large price spikes.

The key risk now isn’t just production—it’s logistics. If Hormuz remains blocked for an extended period, analysts warn oil could surge toward $150 per barrel, potentially reigniting global inflation and tightening financial conditions.

Bottom line for PE: energy shocks rarely stay confined to energy. Sustained oil spikes would ripple through transportation, manufacturing, and consumer sectors, reshaping deal models and portfolio margins across the private markets. (More)

Download the report on the rise of new fund structures and what it means for GP operations as investor expectations and operating cadence shift. Get the report →

Supporting our sponsors supports our free newsletters. Please support our sponsors!

“In the short run, the market is a voting machine, but in the long run, it is a weighing machine.”

Benjamin Graham