- PE 150

- Posts

- Oil Markets Brace for Shock as Iran Escalation Threatens the Strait of Hormuz

Oil Markets Brace for Shock as Iran Escalation Threatens the Strait of Hormuz

The confrontation between Iran, vs United States and Israeñ has rapidly transformed from a geopolitical flashpoint into a global energy shock.

Gaston Brizuela Bosio

March 09, 2026 • Estimated Reading Time: 5 minutes

In recent days, Iranian strikes on energy infrastructure across the Gulf—particularly in Qatar—combined with the near-closure of the Strait of Hormuz, have pushed oil markets into a state of extreme uncertainty. While spot markets remain relatively cautious for now, oil futures markets are already reacting with far greater alarm, anticipating the possibility of severe supply disruptions in the coming weeks. The events unfolding in the Gulf highlight how deeply integrated global energy markets are, and how quickly geopolitical conflict can ripple through the global economy.

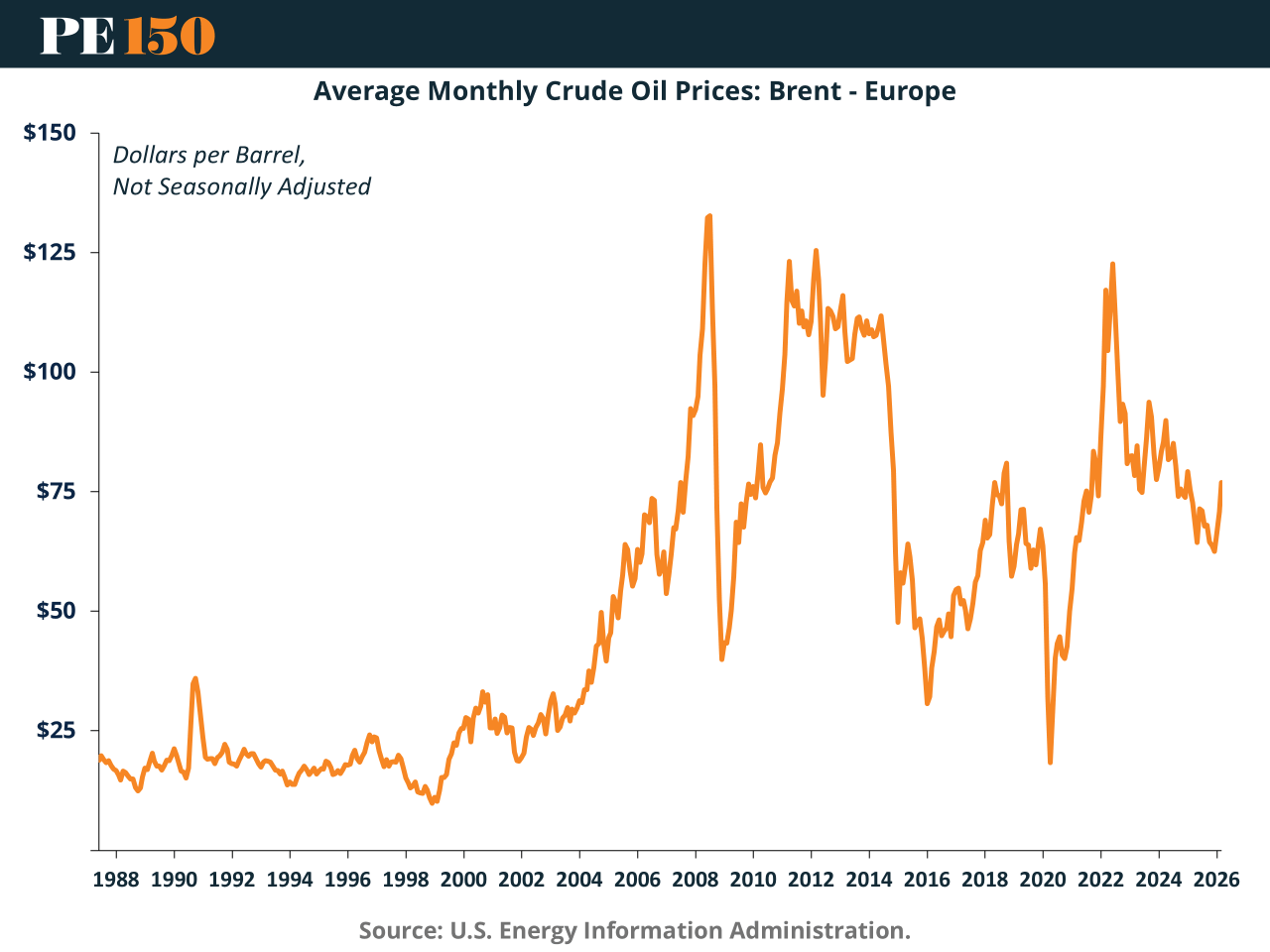

Historically, geopolitical shocks have repeatedly driven dramatic spikes in oil prices. As the chart above illustrates, major crises—from the Gulf War to the 2008 financial crisis and the Russian invasion of Ukraine—have produced sharp volatility in global crude benchmarks such as Brent. Oil markets are especially sensitive to political instability in the Middle East because the region remains one of the largest and most strategically important sources of global supply. Even relatively brief disruptions can cause prices to surge as traders anticipate shortages.

The latest escalation follows reports that Iranian forces struck refinery and liquefied natural gas facilities in Qatar and other Gulf locations. QatarEnergy subsequently halted LNG production after the attacks, declaring force majeure and warning that energy exports across the Gulf could cease entirely if the conflict continues. According to Qatar’s energy minister Saad al-Kaabi, the war could bring global economic activity to a halt if energy flows remain disrupted. Even if hostilities were to stop immediately, he cautioned that restoring production could take weeks or months.

At the center of the crisis lies the Strait of Hormuz, the narrow maritime corridor connecting the Persian Gulf with the open ocean. Roughly 20 million barrels of oil and petroleum products per day—about one-fifth of global consumption—normally transit this chokepoint. With shipping traffic now severely restricted and nearly two hundred tankers stranded in the region, energy traders are confronting the possibility that a significant share of the world’s oil supply could temporarily disappear from the market.

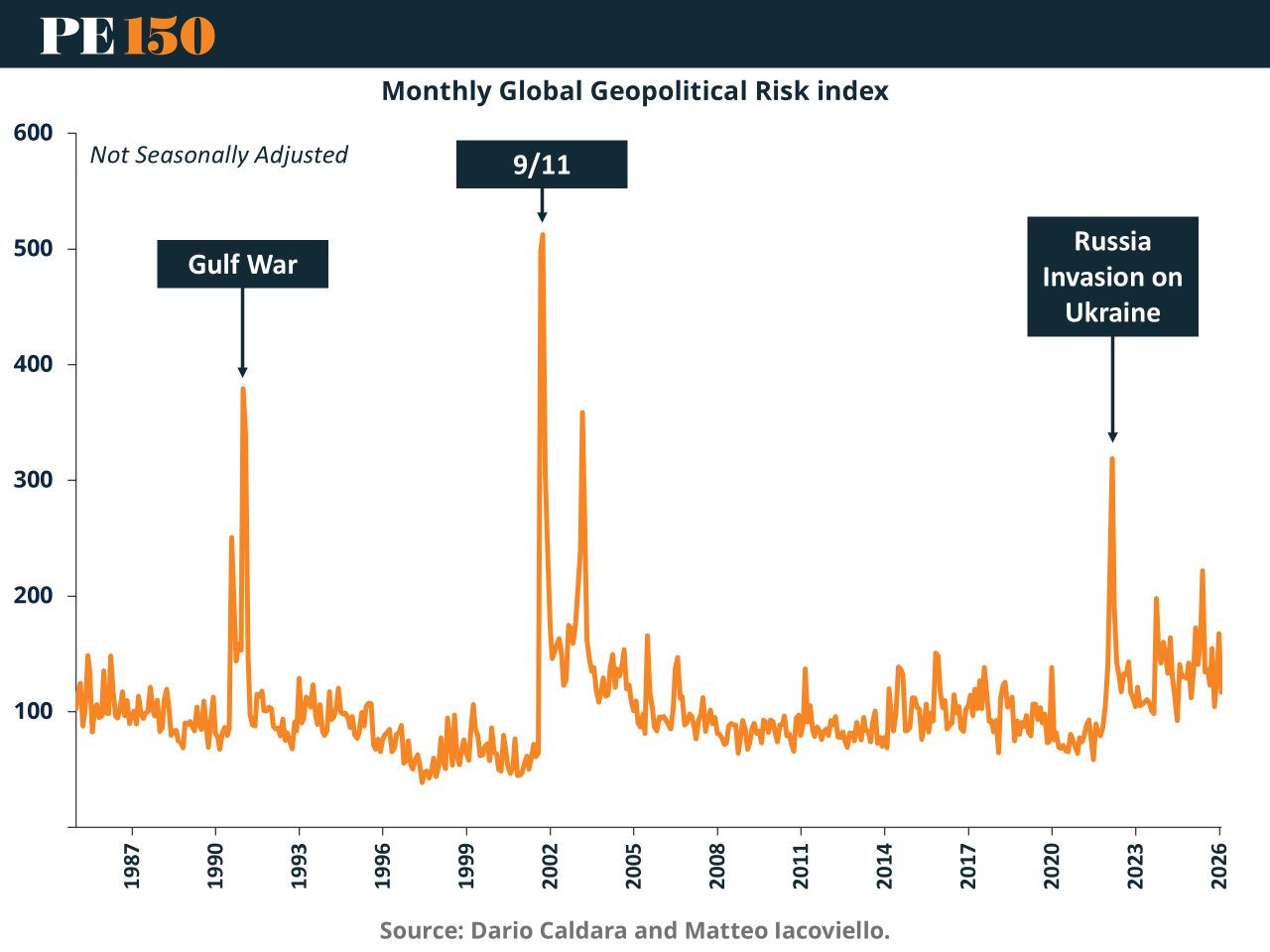

The geopolitical risk index underscores how unusual the current moment is. Historically, the largest spikes in global risk coincide with major geopolitical shocks such as the Gulf War, the September 11 attacks, or Russia’s invasion of Ukraine. The current surge reflects the rapidly escalating tensions surrounding Iran and the potential for the conflict to widen across the Middle East.

Energy markets are reacting in two distinct ways. Spot markets—where oil is traded for immediate delivery—have risen but remain comparatively restrained. Brent crude has climbed toward the low $90 range per barrel, reflecting concern but not yet a full-scale supply panic. Futures markets, however, are reacting much more aggressively. Contracts for future delivery have surged as traders attempt to hedge against the possibility that the Strait of Hormuz could remain blocked for an extended period.

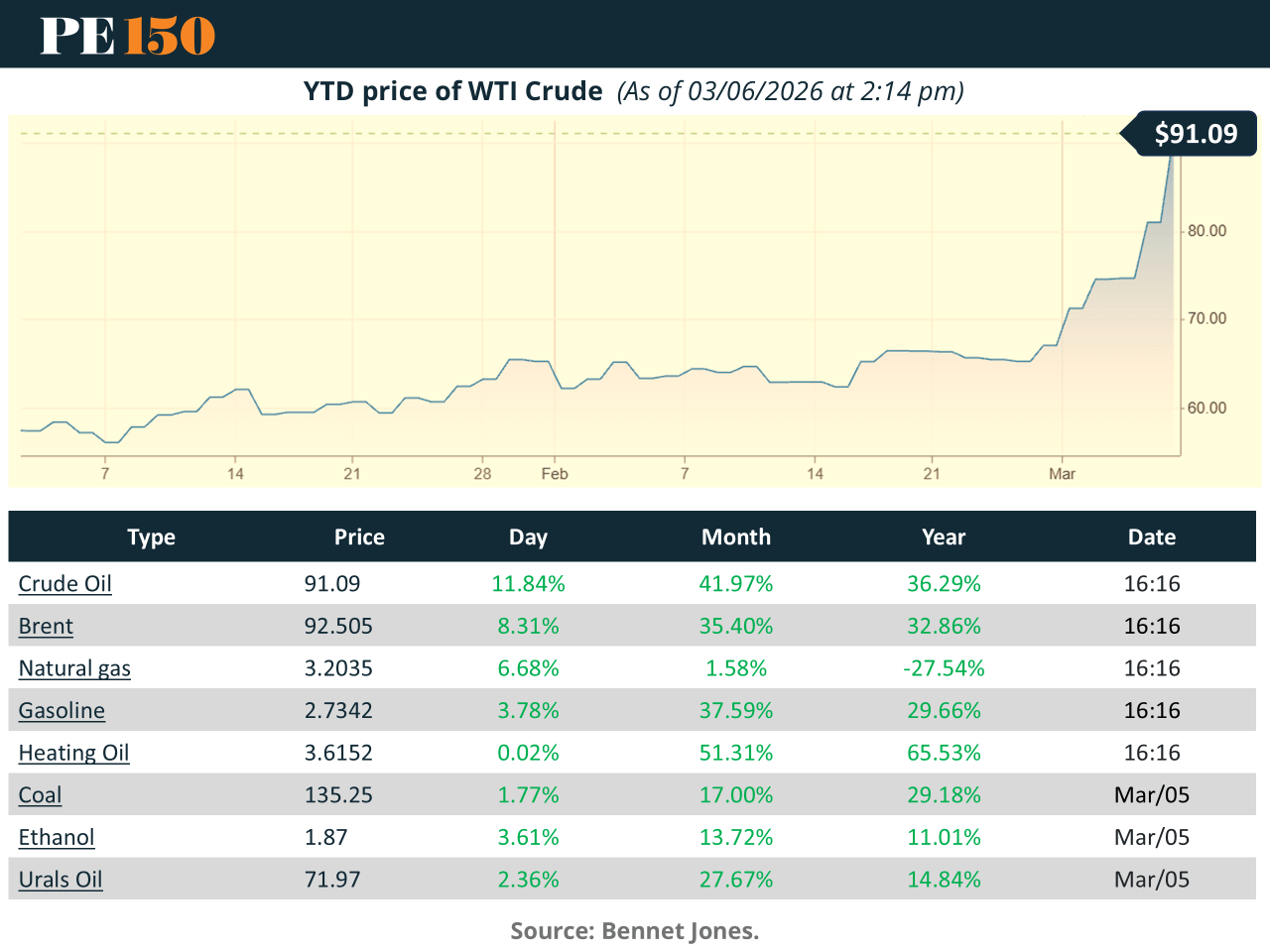

WTI crude futures recently jumped more than 10 percent in a single week, marking the largest gain since the energy shock following Russia’s invasion of Ukraine in 2022. Traders are pricing in the possibility that Gulf exporters may soon be unable to ship oil at all if tanker traffic cannot safely pass through the strait. Qatar’s warning that regional production could stop within days has intensified those fears.

The year-to-date trajectory of WTI crude prices reflects how quickly sentiment has shifted. For much of the early part of the year, oil prices were relatively stable, fluctuating in the $60–70 range amid expectations of abundant global supply. However, as tensions in the Middle East escalated and shipping through Hormuz became increasingly risky, prices accelerated sharply upward. The recent move toward $90 per barrel reflects the market’s sudden reassessment of geopolitical risk.

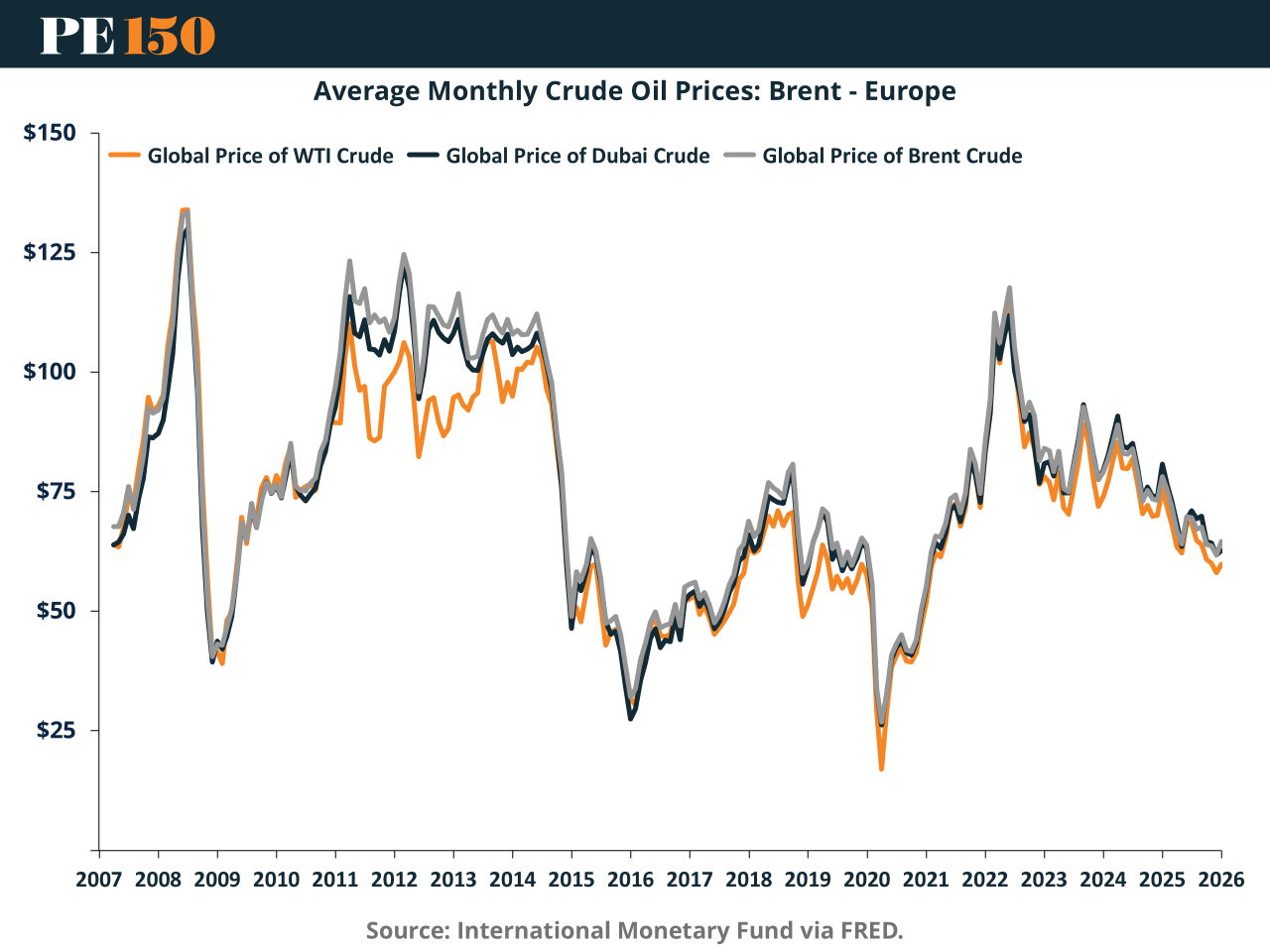

Yet the current surge also highlights an important feature of the oil market that economists often describe as the “global bathtub.” In this framework, oil supply from different producers flows into a single global market, while consumption drains from that shared pool. Because crude oil is largely homogeneous and transportable, prices across regions tend to converge—a phenomenon known as the “law of one price.” As a result, disruptions in one region can often be offset by increased production elsewhere.

The convergence of global oil benchmarks—WTI, Brent, and Dubai crude—illustrates this principle. Despite being produced in different parts of the world, their prices move closely together over time because oil is traded in a highly integrated global market. When supply is disrupted in one region, alternative supplies are typically redirected from other producers, stabilizing prices.

This dynamic has historically limited the impact of sanctions and regional disruptions. For example, when the United States imposed sanctions on Iranian oil exports in 2012, global prices remained relatively stable. The decline in Iranian production was offset by rising U.S. shale output and increased supply from other producers. In essence, other “spigots” in the global bathtub opened wider to compensate.

However, the current crisis is different in one critical respect: it threatens not just a single producer but the physical infrastructure that enables global oil trade. The Strait of Hormuz functions as the primary export route for many Gulf producers, including Saudi Arabia, Iraq, Kuwait, and the United Arab Emirates. If the strait remains blocked, even countries not directly involved in the conflict could struggle to move their oil to global markets.

Some producers do have partial alternatives. Saudi Arabia and the UAE maintain pipelines capable of bypassing Hormuz and transporting oil to ports on the Red Sea or the Gulf of Oman. Saudi Arabia has already begun redirecting shipments through Red Sea terminals to maintain export flows. Nevertheless, these pipelines cannot fully replace the enormous volume of oil normally shipped through the strait.

The longer the disruption persists, the greater the risk of a true global energy shock. Analysts warn that if Gulf exports halt for several weeks, oil prices could climb toward $150 per barrel—levels that would likely trigger significant inflation and slow economic growth worldwide. Countries heavily dependent on Gulf energy imports, such as China, India, and Japan, would be particularly vulnerable.

Despite the immediate turmoil, some analysts remain skeptical that the crisis will produce long-lasting supply disruptions. Prior to the current escalation, global oil markets were expected to enter a period of surplus supply in 2026. J.P. Morgan analysts projected Brent crude could average around $60 per barrel due to strong production growth outpacing demand.

Under normal circumstances, such fundamentals would keep prices relatively contained. But geopolitical shocks can overwhelm supply-demand balances in the short term. Historically, major political upheavals in oil-producing countries—from revolutions to wars—have produced price spikes averaging more than 70 percent from their starting point.

For now, global energy markets remain caught between two competing forces. On one hand, underlying supply conditions suggest oil should remain relatively abundant. On the other, the possibility of a prolonged conflict involving Iran—and the disruption of one of the world’s most critical energy chokepoints—creates the risk of a severe supply shock.

The divergence between cautious spot prices and panicked futures markets reflects this uncertainty. Traders are effectively betting on two different scenarios at once: that the current crisis might resolve quickly, but that if it does not, the consequences for global energy markets could be profound.

In the coming weeks, the trajectory of oil prices will depend largely on whether the Strait of Hormuz reopens and whether Gulf energy infrastructure can resume normal operations. If shipping resumes and production restarts, prices may retreat toward the levels implied by global supply fundamentals. But if the conflict escalates or spreads further across the region, the world could soon face its most significant energy crisis since the shocks of the 1970s.

Sources & References

BBC. (2026). Oil price jumps after Qatar warns all Gulf production could stop within days. https://www.bbc.com/news/articles/cy031ylgepro

CNBC. (2026). WTI Crude. https://www.cnbc.com/quotes/@CL.1

D. Caldara and M. Iacoviello. Geopolitical Risk Index. https://www.matteoiacoviello.com/gpr.htm

Federal Reserve Bank of St. Louis. (2018). The economics of oil sanctions. A look at Iran, the law of one price, and the global bathtub. https://fredblog.stlouisfed.org/2018/06/the-economics-of-oil-sanctions/

International Monetary Fund, Global price of WTI Crude [POILWTIUSDM], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/POILWTIUSDM, March 6, 2026.

JP Morgan. (2026). Oil price forecast: A bearish outlook for Brent in 2026. https://www.jpmorgan.com/insights/global-research/commodities/oil-prices

Trading Economics. (2026). Crude Oil WTI (USD/Bbl). https://tradingeconomics.com/commodity/crude-oil

US Energy Information Administration. (2026). Petroleum & Other Liquids. https://www.eia.gov/dnav/pet/pet_pri_spt_s1_d.htm