- PE 150

- Posts

- The Bottleneck and the Breakout: What’s Really Driving PE Growth in 2025

The Bottleneck and the Breakout: What’s Really Driving PE Growth in 2025

Private equity is facing a liquidity bottleneck just as portfolio companies deliver outsized growth. This tension is reshaping how firms exit, deploy capital, and capture value in 2025.

Good morning, ! This week we're covering private equity`s cash bottleneck and the exit landscape, PE-backed companies are projected to grow revenues 10.6% in 2025, US GDP grew 3.8% QoQ with Manufacturing leading the wave, and Private Credit still pulls capital mostly driven by higher yields than public credits and its diversification feature.

Want to advertise in PE 150? Check out our self-serve ad platform, here.

Know someone who would love this? Pass it along—they’ll thank you later! Here’s the link.

DATA DIVE

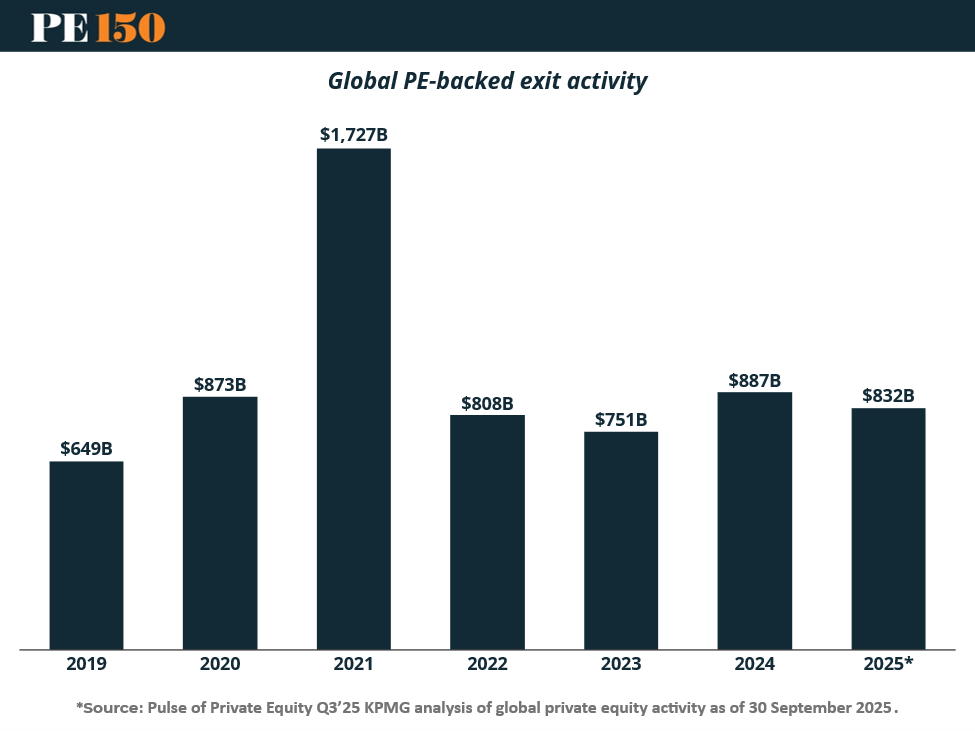

Liquidity Is Back… Just Not How You Remember It

This year’s exit data shows a market recovering in shape, not speed. Global PE-backed exits are projected to hit $832B in 2025, up from 2024 but still half the $1.7T peak in 2021. The rebound is powered by trade sales and secondary buyouts, while IPOs remain a rounding error. With holding periods nearing six years and more than $2.6T in dry powder, sponsors are engineering liquidity through continuation funds, NAV financing, and minority recaps. As EY’s Pete Witte notes, momentum is improving but still “choppy,” pushing firms to build liquidity rather than wait for it. The real bottleneck: proving value — 65% of firms struggle to document value creation, and 41% cite weak data granularity during diligence. In 2025, liquidity isn’t found — it’s built.

TOGETHER WITH MODE MOBILE

Apple just secretly added Starlink satellite support to iPhones through iOS 18.3.

One of the biggest potential winners? Mode Mobile.

Mode’s EarnPhone already reaches 50M+ users that have earned over $325M, and that’s before global satellite coverage. With SpaceX eliminating "dead zones," Mode's earning technology can now reach billions more in unbanked and rural populations worldwide.

Their global expansion is perfectly timed, and accredited investors still have a chance to invest in their pre-IPO offering at $0.50/share.

With their recent 32,481% revenue growth and newly reserved Nasdaq ticker, Mode is one step closer to a potential IPO.

-

Disclosures

Mode Mobile recently received their ticker reservation with Nasdaq ($MODE), indicating an intent to IPO in the next 24 months. An intent to IPO is no guarantee that an actual IPO will occur.

The Deloitte rankings are based on submitted applications and public company database research, with winners selected based on their fiscal-year revenue growth percentage over a three-year period.

This offer is only open to accredited investors.

TREND OF THE WEEK

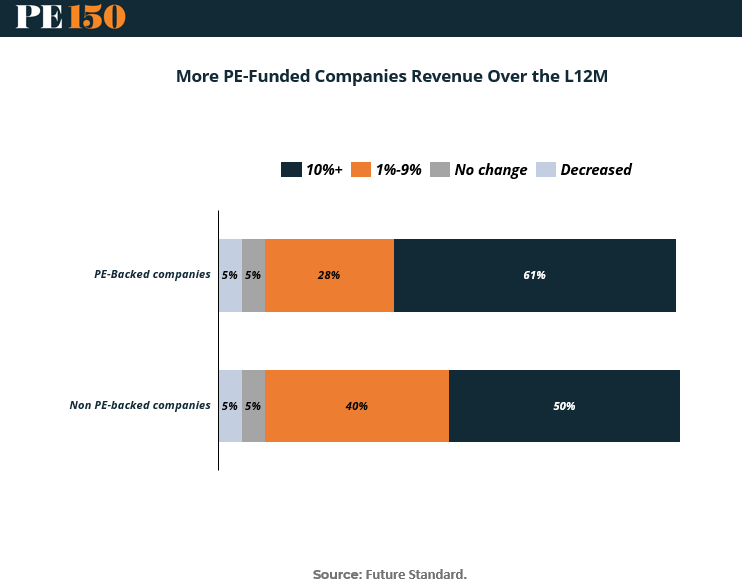

PE-Backed Companies Are Pulling Away on Growth

Private equity is doing what it says on the tin: driving growth.

New data from Future Standard shows that 61% of PE-backed companies grew revenue by 10% or more over the last 12 months—compared to just 50% of non-PE-backed peers. Meanwhile, fewer PE-backed firms reported modest growth (1–9%) or stagnation.

It’s not just a one-off. This trend aligns with recent multi-year revenue performance showing a consistent delta between sponsored and non-sponsored companies. The implication: operational playbooks, bolt-on M&A, and growth equity injections are delivering measurable results.

For LPs, it’s validation. For corporate strategists, it’s pressure. And for GPs facing slower exits, it’s a compelling pitch: even if the liquidity timeline stretches, the value creation engine is still firing.

The takeaway: In a market focused on fundamentals, growth is the new leverage. And PE seems to be winning that race. (More)

LIQUIDITY CORNER

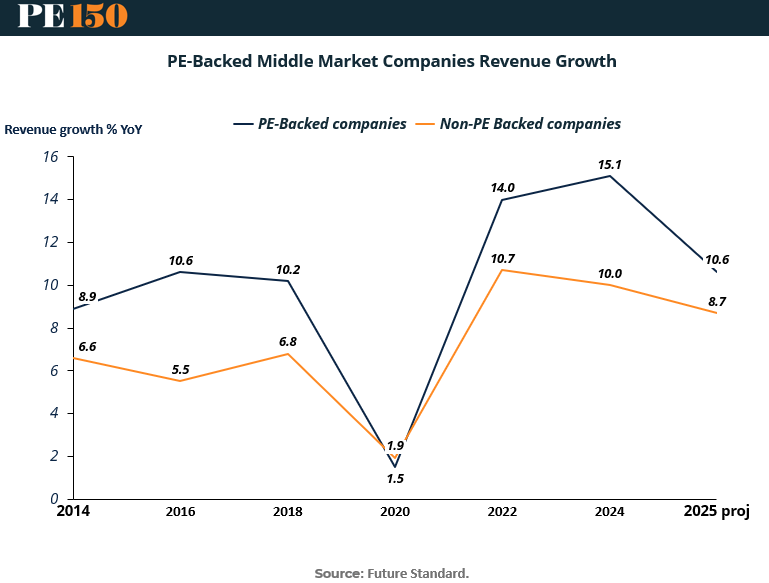

Middle Market Momentum = Exit Optionality

If you're sitting on a portfolio of PE-backed middle market companies, the latest revenue growth data offers a reason to exhale—and maybe pick up the phone.

According to Future Standard, PE-backed companies are projected to grow revenues 10.6% in 2025, outpacing non-PE peers at 8.7%. That gap isn’t new—but it’s consistent. Even post-pandemic, PE-backed firms posted faster rebounds (14.0% in 2022, 15.1% in 2024) than non-sponsored companies.

This matters in a liquidity-starved environment. Strong top-line growth gives GPs more optionality: dividend recaps, partial exits, continuation vehicles, or even IPO prep—all become more viable when the comp set is lagging. For buyers with dry powder, it’s also a signal: the performance delta is real, and it’s widening.

Bottom line: Exit markets may still be constrained, but the growth engine is on. For firms with high-performing portfolio companies, 2025 could finally bring leverage back—to the negotiating table. (More)

DEAL OF THE WEEK

PAG’s Big-Mall Energy

PAG just dropped $2.8bn to take control of a portfolio of Dalian Wanda malls, marking China’s largest PE check of the year and the biggest cross-border commercial real estate deal since 2021. The Hong Kong firm also helped assemble $6.3bn for a fund backed by Sunshine Life Insurance, Tencent, and a JD.com-linked vehicle—a who’s-who lineup betting that China’s battered consumer sector finally has a pulse. Wanda, once overexposed to real estate, has been offloading everything from theme parks to Legendary Entertainment. Now PAG is effectively wagering that strong tenants like Adidas and Nike can carry a recovery. It’s a rare moment where “Chinese mall operator” and “PE optimism” show up in the same sentence. (More)

PRESENTED BY FINANCE BUZZ

Put Interest On Ice Until 2027

Pay no interest until 2027 with some of the best hand-picked credit cards this year. They are perfect for anyone looking to pay down their debt, and not add to it!

Click here to see what all of the hype is about.

PRIVATE CREDIT

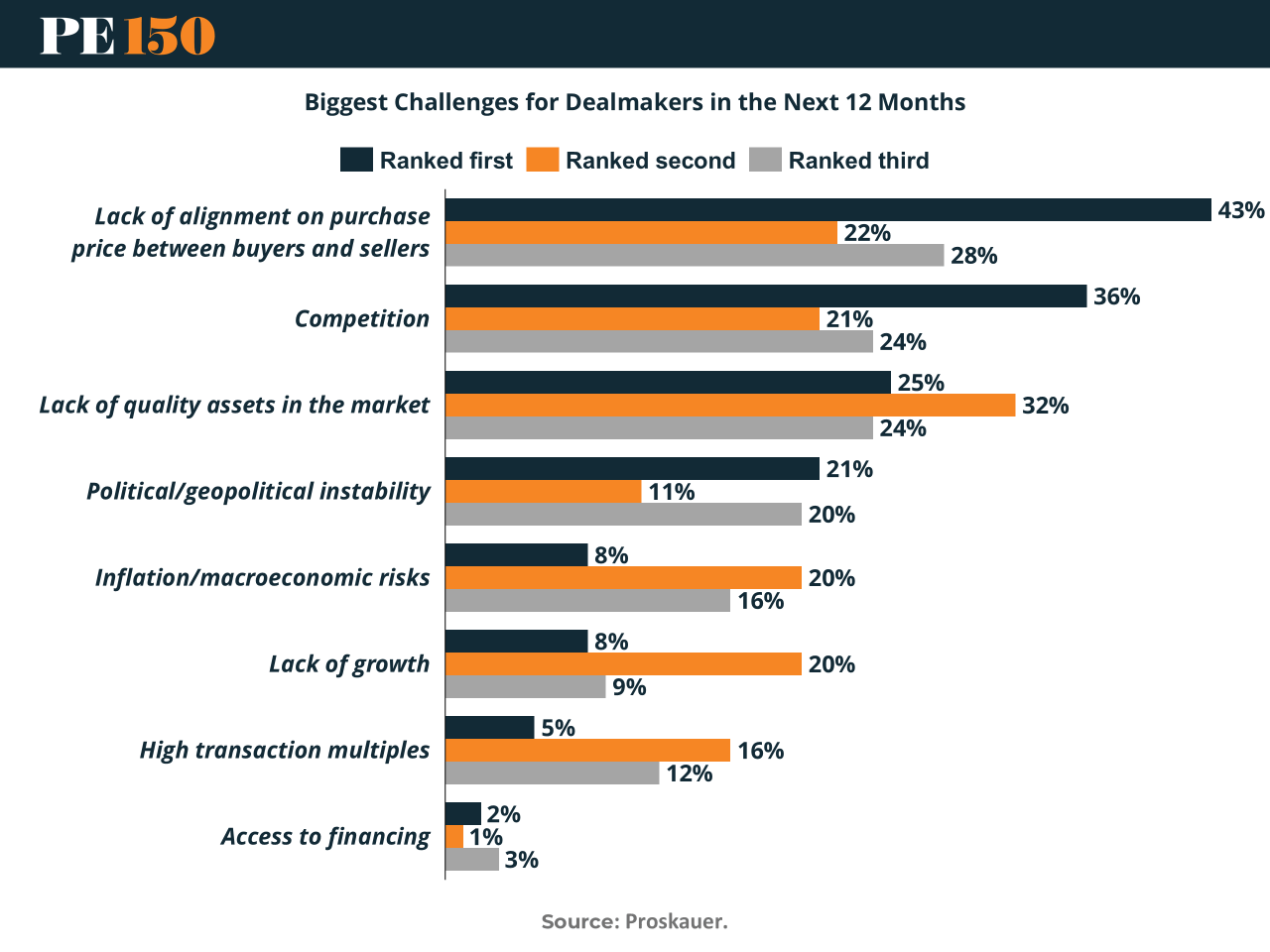

Credit’s New Prime Time

Private credit lenders are staring at the same wall the rest of the deal economy keeps running into: lack of alignment on purchase price. With 43% of respondents citing it as the top challenge, it’s the clear bottleneck shaping underwriting discipline and slowing deployment. Meanwhile, competition has muscled its way into second place at 36%, leap-frogging inflation/macro risks, which barely registers as a primary concern at 8%. For private credit, this reshuffle matters. More bidders fighting over fewer quality assets — and doing so at mismatched valuations — means lenders must stretch on structure, not price. In other words: tighter covenants, heavier diligence, and a renewed focus on quality of assets, now a solid mid-tier concern at 25%. (More)

MICROSURVEY

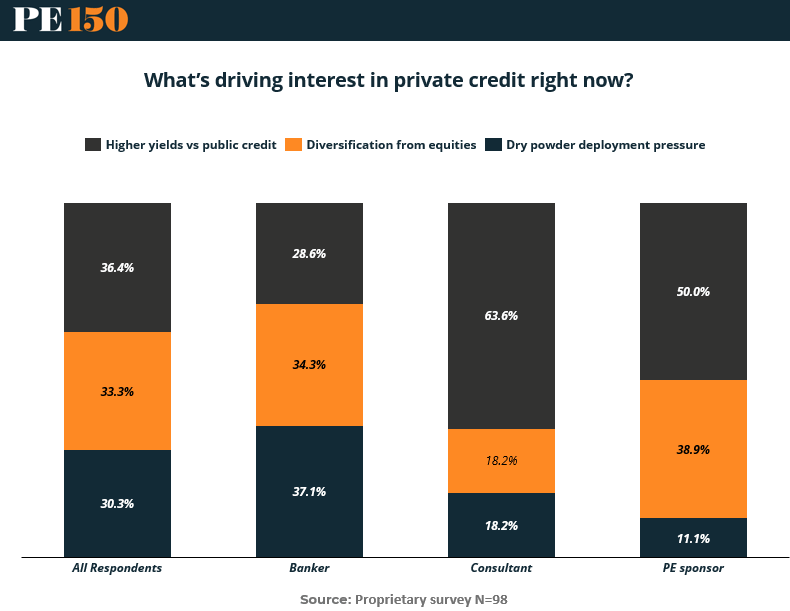

Why Private Credit Keeps Pulling Capital

Higher yields are still king—but the reasons vary depending on where you sit.

In our latest survey of 98 market participants, 36.4% of all respondents cited higher yields vs. public credit as the top driver of private credit interest. But break it down by role, and motivations diverge:

63.6% of consultants are yield-maximizers—far above any other group.

37.1% of bankers say it’s more about dry powder deployment.

50% of PE sponsors still chase yield, but 39% also see diversification from equities as a key factor.

That last stat might be the most telling. With dealmaking still slow and fundraising uneven, PE sponsors increasingly view private credit as a capital deployment and portfolio allocation tool—not just a returns engine.

Bottom line: Private credit isn’t a one-size-fits-all play. Understanding the “why” behind capital flows is key for GPs pitching funds—and LPs rebalancing portfolios. (More)

MACROVIEW

The Two-Speed Economy

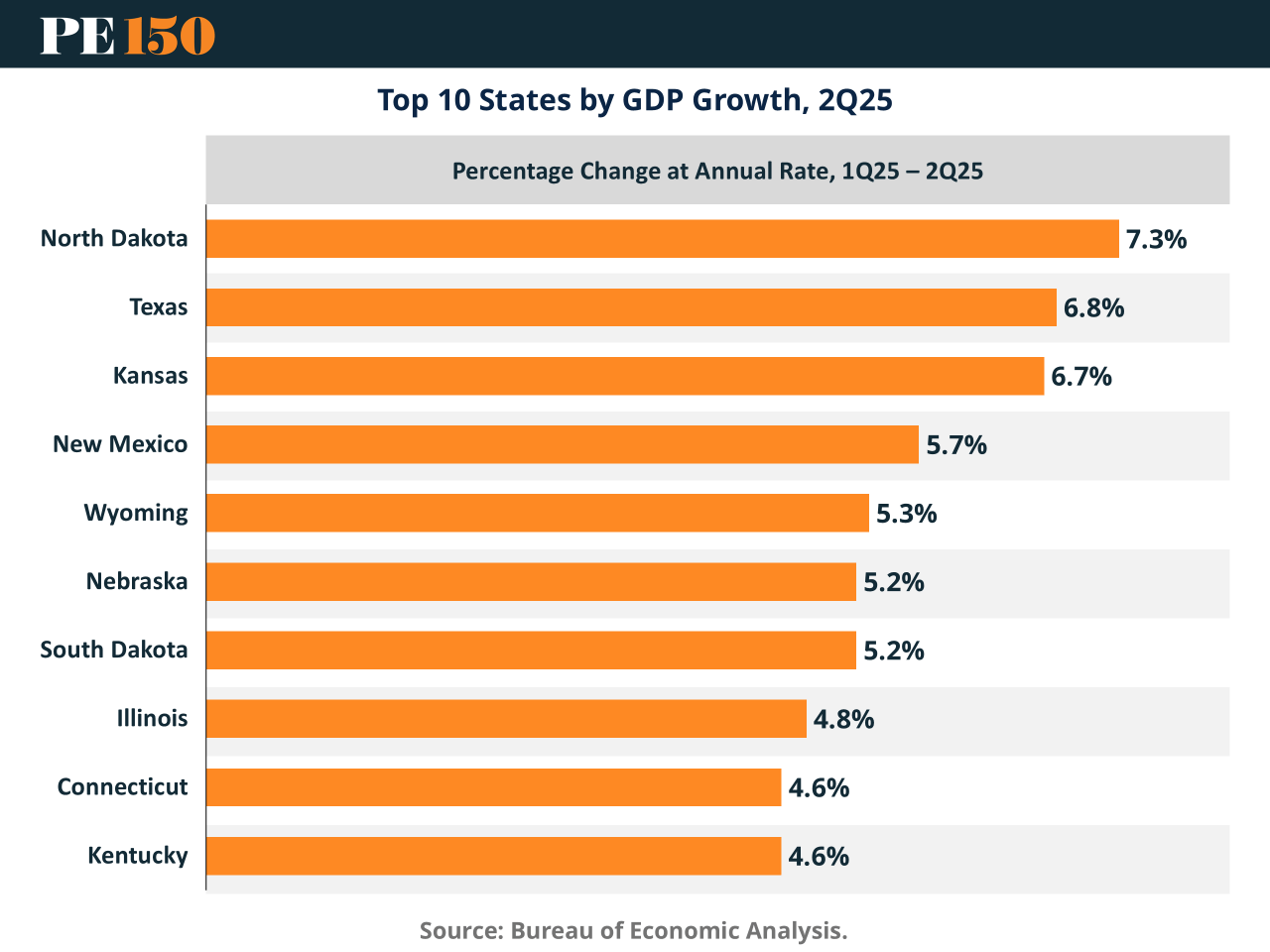

U.S. GDP rose 3.8% in Q2 2025, but this isn’t your grandpa’s recovery — it’s a bifurcated grind. North Dakota, Texas, and New Mexico are booming thanks to energy and mining, while Arkansas shrank, and the District of Columbia flatlined. The top performers? Resource hubs flush with capital and commodity tailwinds. Manufacturing led nationally, with 1.1 percentage points of growth, driven by demand for durables, reshoring, and tech upgrades. Meanwhile, retail and government lagged — a drag on portfolios tied to consumer credit, municipal debt, and small business. (More)

COMPLIANCE CORNER

Registration Rules: Not Optional

Under the Investment Advisers Act of 1940, the U.S. Securities and Exchange Commission (SEC) expects advisers to private funds to be registered — unless they meet one of the exemptions. Those include the venture‑capital adviser exemption, the foreign private adviser exemption, and the private‑fund adviser exemption under §3(c)(1) or §3(c)(7) structures. Once you fall above US$150 million in private‑fund AUM, you’re filing Form PF and full disclosure applies. Even for the exempt reporting advisers (ERAs), books and records are still subject to SEC inspection. The message: registration, disclosure, oversight—you shouldn’t treat them as optional. Non‑compliance isn’t “creative structuring”; it’s increased risk. (More)

THIS WEEK IN HISTORY

Markets Freeze: JFK’s Assassination Halts Wall Street

On November 22, 1963, U.S. equity markets ground to a halt. Just after 1:30 p.m. ET, news broke that President John F. Kennedy had been assassinated in Dallas. Within 30 minutes, the NYSE, AMEX, and Chicago Board of Trade suspended trading—marking one of the few times in history the U.S. markets closed early due to national tragedy.

The Dow had already dropped 21 points (≈ 2.8%) in the chaotic minutes before the halt—equivalent to a 1,000+ point swing in today’s index terms. Trading resumed the following Monday, and the market surprisingly rebounded, ending the week flat.

Why it matters: The 1963 shutdown reinforced a hard truth for market participants—liquidity vanishes when uncertainty becomes existential. For PE investors and dealmakers, the lesson holds: macro shocks don’t just move prices—they freeze the pipes.

Fun fact: This was the first major news event where live television directly impacted financial flows in real time. The information edge didn’t belong to the traders—it belonged to the TV. (More)

TWEET OF THE WEEK

"Never let the fear of striking out keep you from playing the game."

Babe Ruth