- PE 150

- Posts

- Private Credit +2,320%: The System Has Shifted

Private Credit +2,320%: The System Has Shifted

This week we're diving into private credit as the new risk warehouse, why deal flow isn’t translating into closes, how ERISA is reshaping access to alternatives, and the rise of engineered liquidity in private markets.

Good morning, ! This week we're diving into private credit as the new risk warehouse, why deal flow isn’t translating into closes, how ERISA is reshaping access to alternatives, and the rise of engineered liquidity in private markets.

Want to advertise in PE 150? Check out our ad platform, here.

Know someone who would love this? Pass it along—they’ll thank you later! Here’s the link.

DATA DIVE

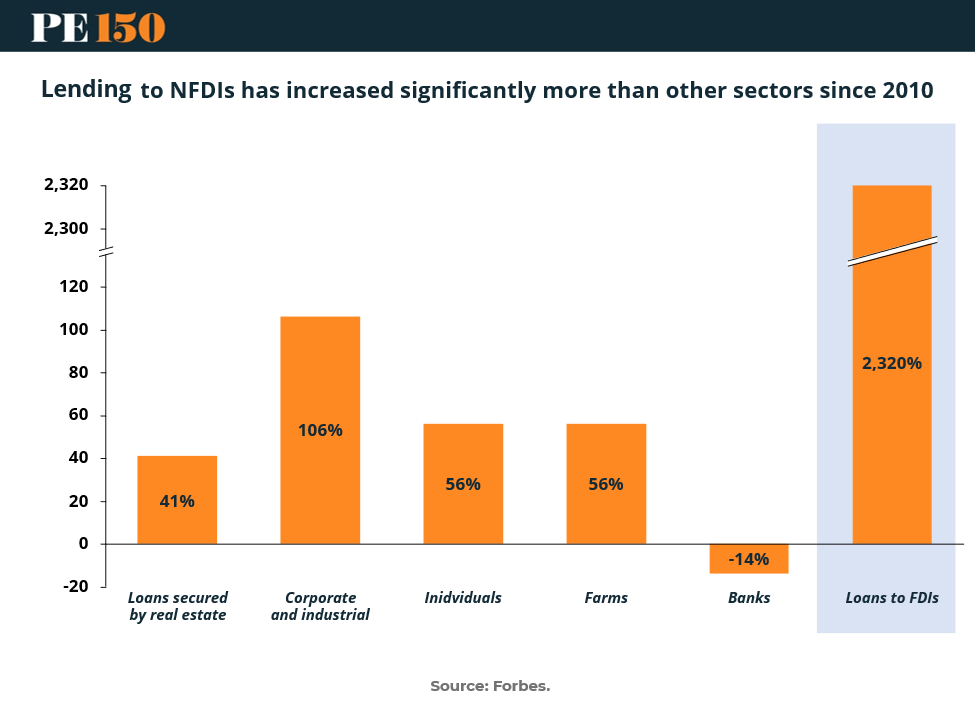

The System’s New Balance Sheet

Private credit is no longer a supplement to the banking system. It is the system.

Over the past decade, lending to financial institutions has exploded by 2,320%, as banks shifted from holding risk to distributing it. What used to sit on regulated balance sheets now lives inside private credit funds, BDCs, and other non bank lenders. At the same time, performance has remained strong, with a 1.2 Sharpe ratio and just 0.4% loss rates in senior direct lending, reinforcing the narrative that this is a stable, yield generating asset class.

But that stability is not accidental. It is structural. Private credit is designed to smooth volatility, extend duration, and delay loss recognition through amendments and restructurings. The rise of semi liquid vehicles, now 53% of inflows, adds a new layer of complexity, pairing illiquid assets with more flexible capital.

The result is a market where risk is concentrated, but not fully visible.

Bottom line:

Private credit has become the primary warehouse of corporate risk. For turnaround investors, the opportunity is no longer in reacting to defaults. It is in anticipating where delayed stress inside private credit portfolios will finally be forced to resolve. (More)

TREND TO WATCH

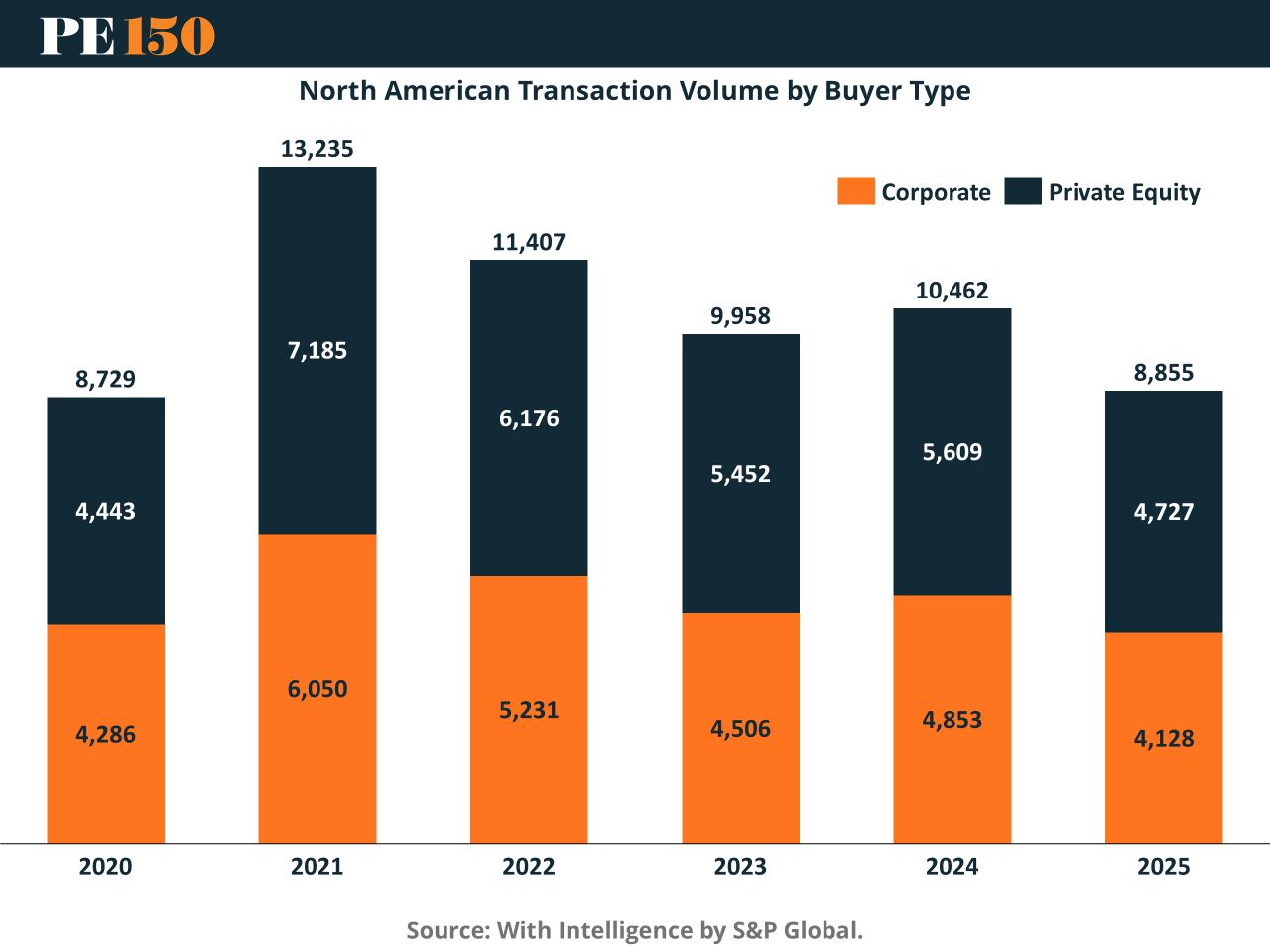

More Listings, Fewer Closings

Private equity dealmaking is staging a tentative rebound, but calling it a comeback would be generous. After peaking in 2021, North American transaction volumes remain below trend, with PE still outpacing corporates, just at lower absolute levels . The bigger issue: a growing backlog of aging PortCos, with 63% held over four years.

The friction point? Deals marketed vs. deals closed. That conversion rate slipped in late 2024 and hasn’t recovered, reflecting a persistent risk-off buyer mindset.

Yes, inflation is stabilizing and policy clarity is improving, which should help confidence. But until buyers actually show up—and close—this is less a recovery and more a pressure release valve. (More)

COMPLIANCE CORNER

ERISA Opens the Door (Carefully)

For years, ERISA acted like a strict bouncer—Private Equity could get in, but only under tight conditions. That’s changing.

A 2025 Executive Order is pushing regulators to revisit long-standing restrictions, including prior DOL guidance that discouraged alternatives in 401(k) plans. The result: early signs of a more permissive framework for private markets.

The SEC is also smoothing access, allowing certain registered funds to bypass “Plan Asset” look-through rules, historically triggered at the 25% threshold.

Why it matters: This isn’t deregulation—it’s recalibration. Fiduciary duty still rules, but the path to Alternative Investments just got wider.

The bottom line: More access, more scrutiny. Sponsors who move early need compliance frameworks that can withstand both. (More)

LIQUIDITY CORNER

The New Liquidity Spectrum

Stat: Semi liquid and evergreen structures now offer periodic or flexible liquidity, versus zero liquidity in traditional 10 to 12 year closed end funds.

Context: The classic private equity model was built on locked capital and delayed gratification. That structure is now being challenged by vehicles that introduce redemption features, NAV based subscriptions, and access for high net worth investors. Semi liquid funds provide scheduled liquidity windows, while evergreen funds go further with flexible redemptions subject to notice and gating. The investor base is shifting alongside the structure, moving from purely institutional LPs toward private wealth channels that demand optionality.

Strategic Takeaway: Liquidity is becoming a product feature, not just an outcome. Managers who can engineer controlled liquidity without breaking long term value creation will win distribution. But more flexibility comes with fragility. In a stressed market, gates will matter more than promises, and sponsors will be tested on whether they built access or just the illusion of it. (More)

MACROVIEW

Labor Market Signal vs Structural Shift

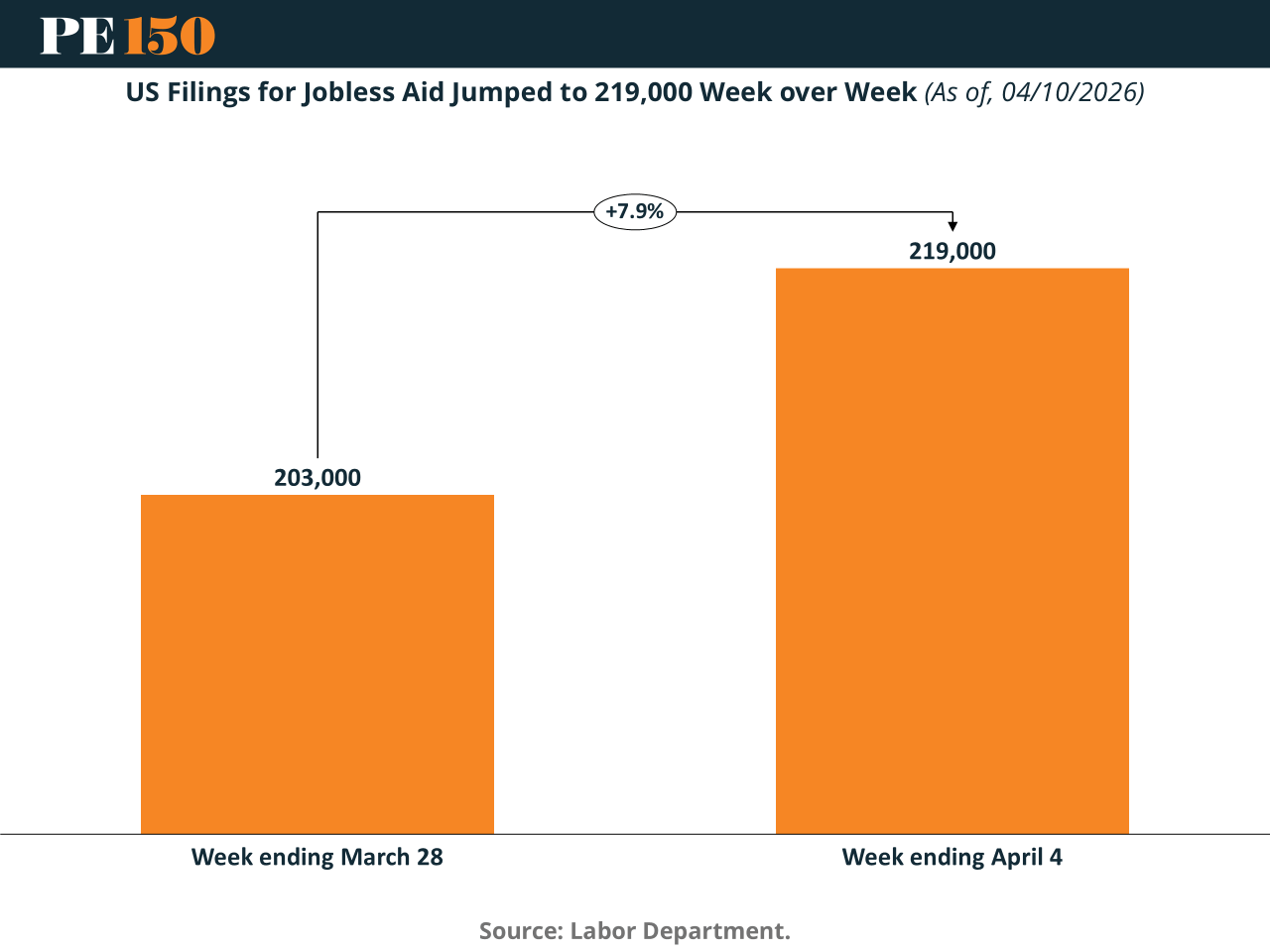

Initial jobless claims rose to 219,000, a 7.9% increase that may appear concerning. However, the broader signal remains stability. Claims sit within the 200,000–250,000 range and remain well below long-term averages (~360,000), indicating subdued layoffs.

The key shift lies beneath the surface. The labor market remains in a “low-hire, low-fire” equilibrium, with firms cautious on both hiring and firing amid macro uncertainty and tight financial conditions.

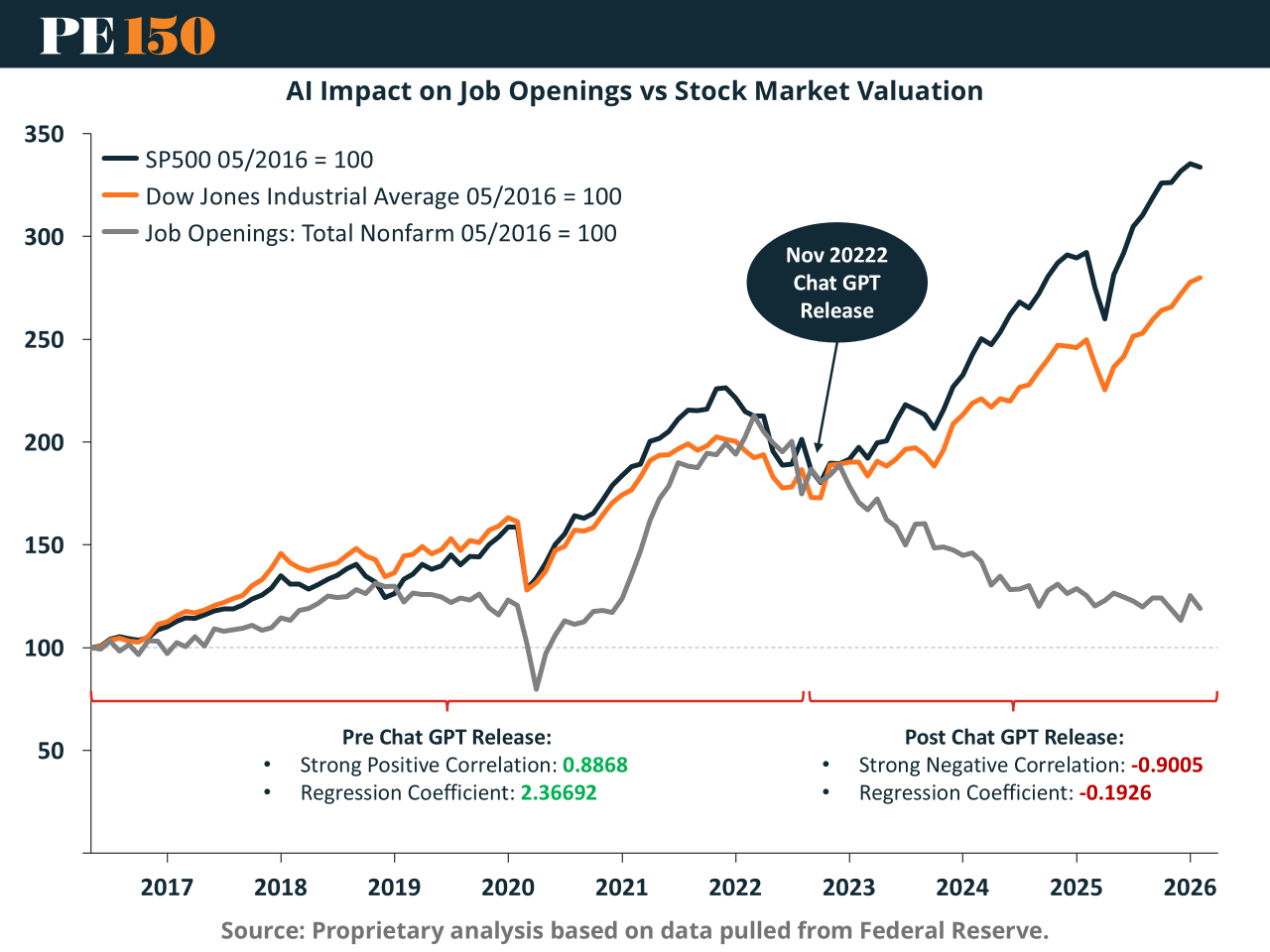

More importantly, a structural break is emerging. Since late 2022, the positive correlation between job openings and equity markets has reversed. Stocks continue to rise, while nonfarm job openings decline.

The likely driver is AI adoption. Firms are scaling output with less labor, signaling a shift toward capital over labor. The labor market appears stable—but its demand dynamics are fundamentally changing. (More)

"All progress takes place outside the comfort zone."

Michael John Bobak