- PE 150

- Posts

- Where the Risk Moved: The Hidden Turnaround Opportunity Inside Private Credit

Where the Risk Moved: The Hidden Turnaround Opportunity Inside Private Credit

Over the past decade, banks have quietly restructured how risk flows through the financial system.

Private credit did not just grow. It absorbed the system.

Over the past decade, banks have quietly restructured how risk flows through the financial system. Instead of holding loans on balance sheet, they now originate and distribute, with private credit funds, BDCs, and other non bank lenders stepping in as the end holders. What looks like disintermediation is really a reintermediation. The risk never left. It just changed hands.

At the same time, performance has masked complexity. Private credit has delivered top tier risk adjusted returns, with a 1.2 Sharpe ratio, outperforming both private equity and public credit. Loss rates remain low, senior lending looks protected, and capital continues to flood in through new structures like semi liquid vehicles, now accounting for 53% of inflows. On the surface, the asset class looks engineered for stability.

But that stability comes with a catch. Risk in private credit does not reprice in real time. It gets extended, amended, and managed behind closed doors. As shown throughout this report , capital has concentrated in the very structures that delay loss recognition. For turnaround investors, that is not a warning. It is the opportunity.

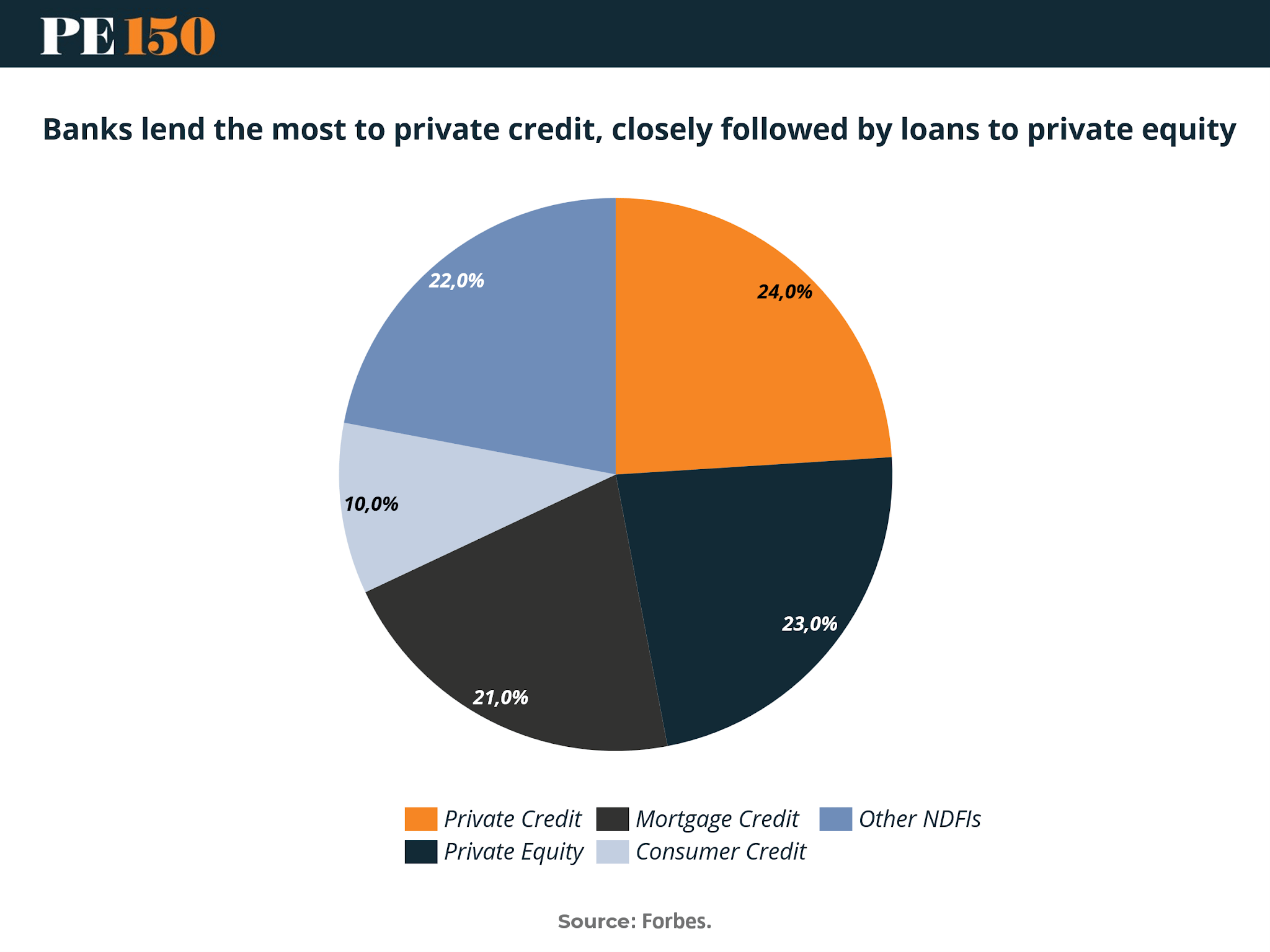

Banks Built the Pipeline. Private Credit Owns the Flow.

Banks are not retreating from private markets, they are redirecting capital into them. The chart shows 24% of bank lending flowing to private credit, just ahead of 23% to private equity. That is not a coincidence. It is a signal that private credit has moved from a substitute to a core transmission channel for institutional lending.

This matters more in the context of today’s capital structure reality. Traditional bank lending is constrained by regulation and balance sheet pressure, yet demand for flexible capital has not slowed. The result is a handoff. Banks originate risk, but increasingly rely on private credit funds to absorb and manage it. What used to sit on bank balance sheets is now being intermediated through direct lenders.

For turnaround investors, this is where the opportunity sharpens. When banks are this exposed to private credit, they are indirectly exposed to the same stressed borrowers. And unlike public markets, that stress does not reprice instantly. It lingers inside portfolios, waiting for restructuring capital, amendments, and sponsor intervention.

Key Takeaways from the Chart

• Private credit leads with 24% of bank lending, confirming its role as the primary outlet for nontraditional corporate financing

• Private equity at 23% sits right behind, reinforcing how tightly linked equity sponsors and credit providers have become in deal ecosystems

• Combined, private markets capture nearly half of bank lending, signaling a structural shift away from traditional corporate lending channels

• Mortgage and consumer credit lag at 21% and 10%, showing banks are prioritizing institutional over retail exposure in this cycle

• Other NDFIs at 22% highlight growing competition, but private credit remains the most direct conduit for complex or stressed deals

• Strategic implication: turnaround opportunities will not originate in public distress cycles first, they will emerge inside private credit portfolios where bank originated risk is now warehoused

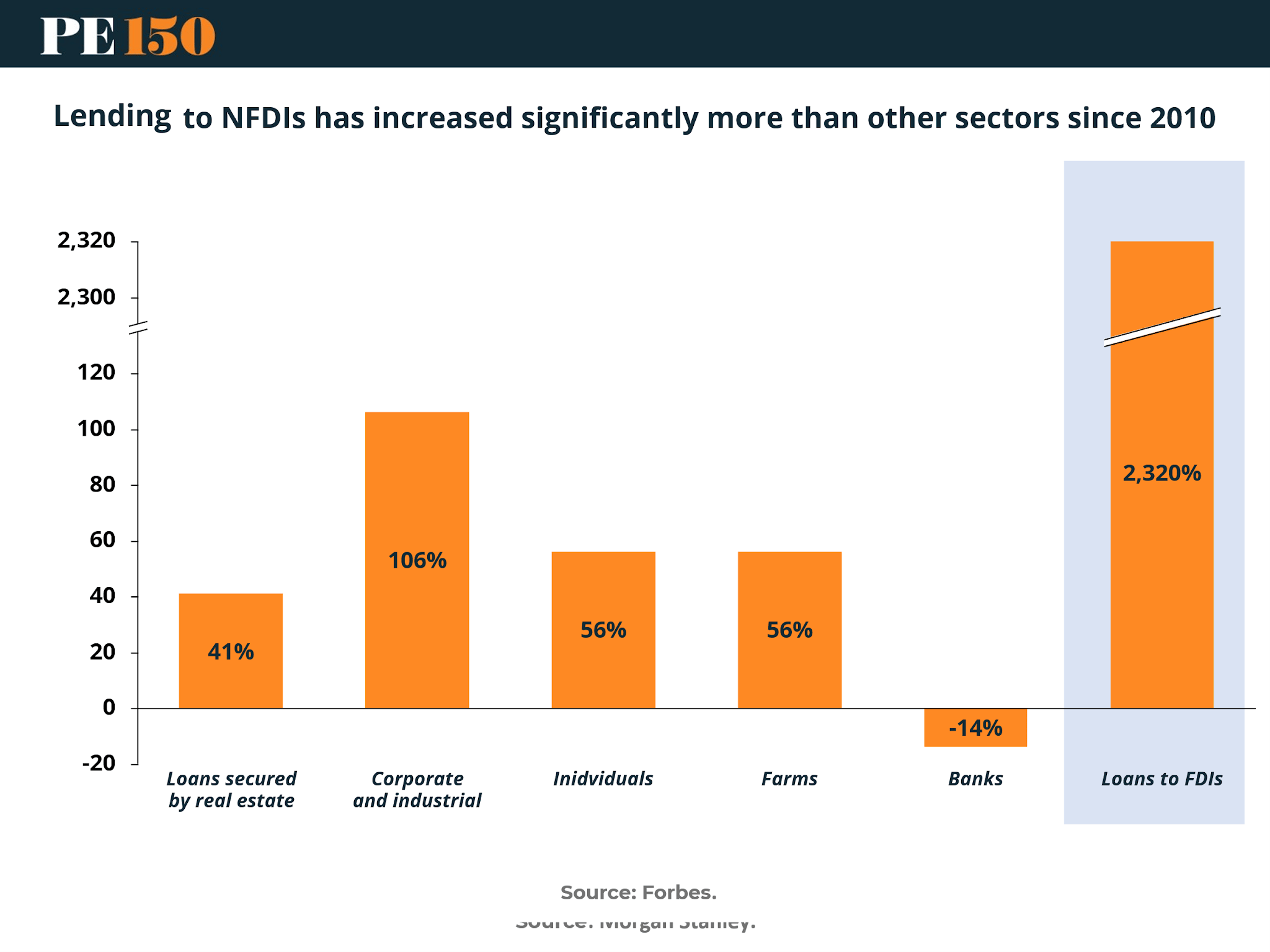

The 23x Shift: Where Credit Growth Actually Happened

If you want to understand where future distress will surface, don’t look at absolute size. Look at growth. Since 2010, lending to financial institutions has surged 2,320%, dwarfing every other category on the chart. The next closest, corporate and industrial lending, sits at just 106%. That gap is not cyclical. It is structural.

This is the quiet build behind private credit’s rise. As banks pulled back from direct corporate risk, capital did not disappear. It moved. Non bank financial institutions became the new balance sheets, absorbing risk that used to live inside regulated entities. Private credit funds, BDCs, and specialty lenders became the intermediaries of choice.

For turnaround investors, this is the map. Stress is no longer concentrated in traditional bank loan books. It is distributed across a fragmented ecosystem of lenders, many of whom lack the scale, tools, or patience to manage prolonged underperformance. When conditions tighten, that fragmentation turns into opportunity.

Key Takeaways from the Chart

• Loans to financial institutions surged 2,320% since 2010, massively outpacing every other lending category

• Corporate and industrial lending grew 106%, highlighting how muted traditional credit expansion has been

• Real estate at 41% and consumer at 56% show steady but unspectacular growth, reinforcing the shift toward institutional channels

• Bank lending contracted by 14%, confirming that risk is being pushed out of regulated balance sheets

• The delta between 2,320% and 106% is the story, credit risk has migrated, not disappeared

• Strategic implication: the next wave of turnaround opportunities will sit inside NDFIs and private credit vehicles, where rapid growth has outpaced underwriting discipline

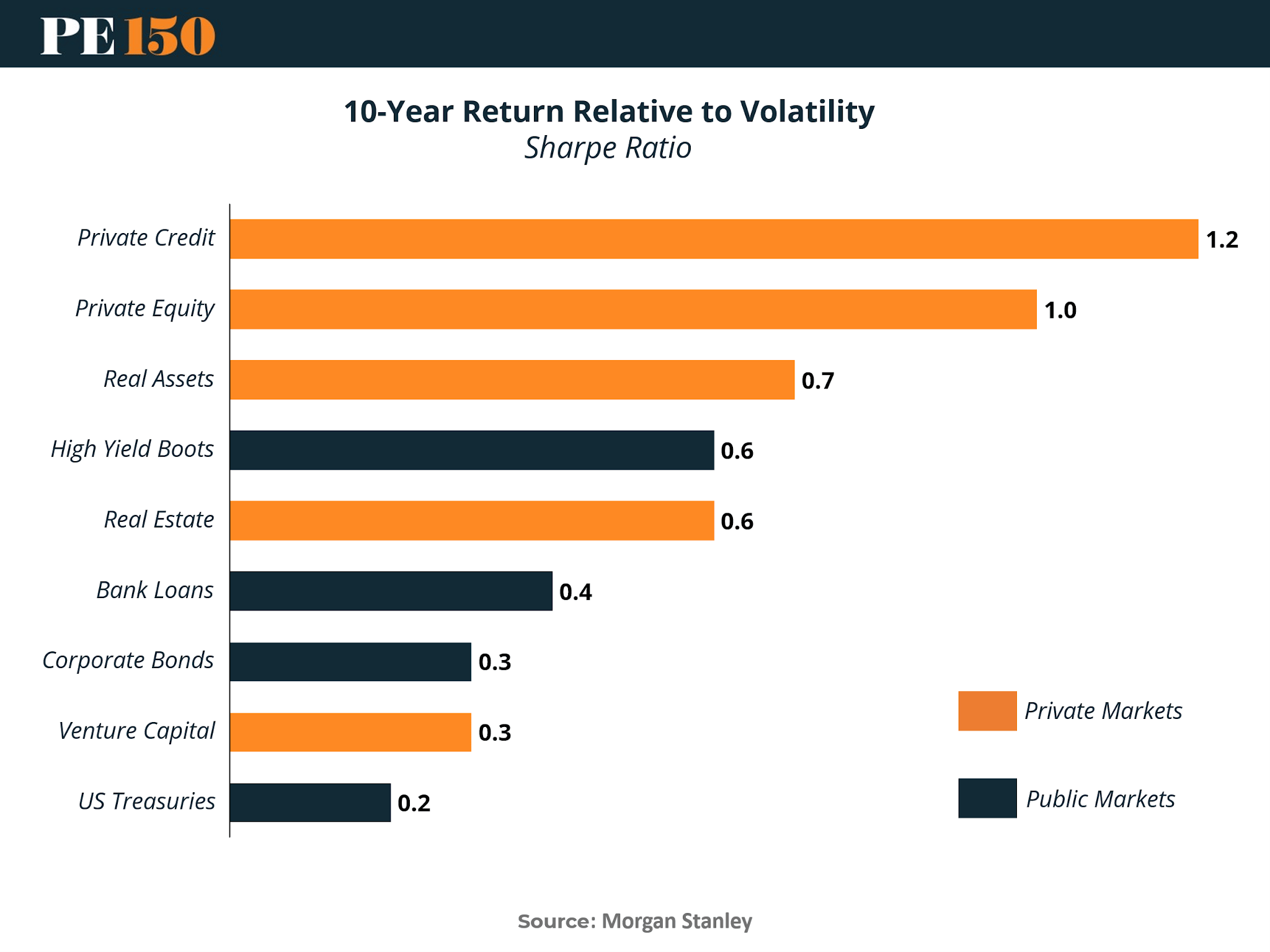

The Illusion of Safety: Why the Best Risk Adjusted Returns Sit in Private Credit

For years, private credit was sold as a yield story. Clip your coupon, avoid volatility, and move on. But the data tells a different story. With a Sharpe ratio of 1.2, private credit is not just competitive, it is leading the entire asset class stack on a risk adjusted basis.

What makes this striking is the comparison set. Private equity, long considered the gold standard for alternative returns, comes in at 1.0. Public market instruments like corporate bonds and bank loans lag far behind at 0.3 and 0.4. Even high yield barely reaches 0.6. This is not a marginal advantage. It is a structural gap in how returns are being generated versus how risk is being managed.

For turnaround investors, this reframes the opportunity set. If private credit delivers superior risk adjusted returns in stable periods, what happens when stress enters the system? The answer is asymmetry. The same structures that smooth volatility also delay loss recognition, creating pockets where risk is mispriced and intervention capital can earn outsized returns.

Key Takeaways from the Chart

• Private credit leads with a 1.2 Sharpe ratio, the highest across all asset classes shown

• Private equity follows at 1.0, confirming strong performance but with more volatility

• Real assets at 0.7 and high yield at 0.6 highlight the drop off once you leave top tier private strategies

• Bank loans at 0.4 and corporate bonds at 0.3 show how traditional credit underperforms on a risk adjusted basis

• US Treasuries at 0.2 reinforce the low return reality of “safe” assets

• Strategic implication: the best risk adjusted returns are concentrated in private credit, but that stability can mask underlying stress, creating ideal entry points for turnaround capital when conditions shift

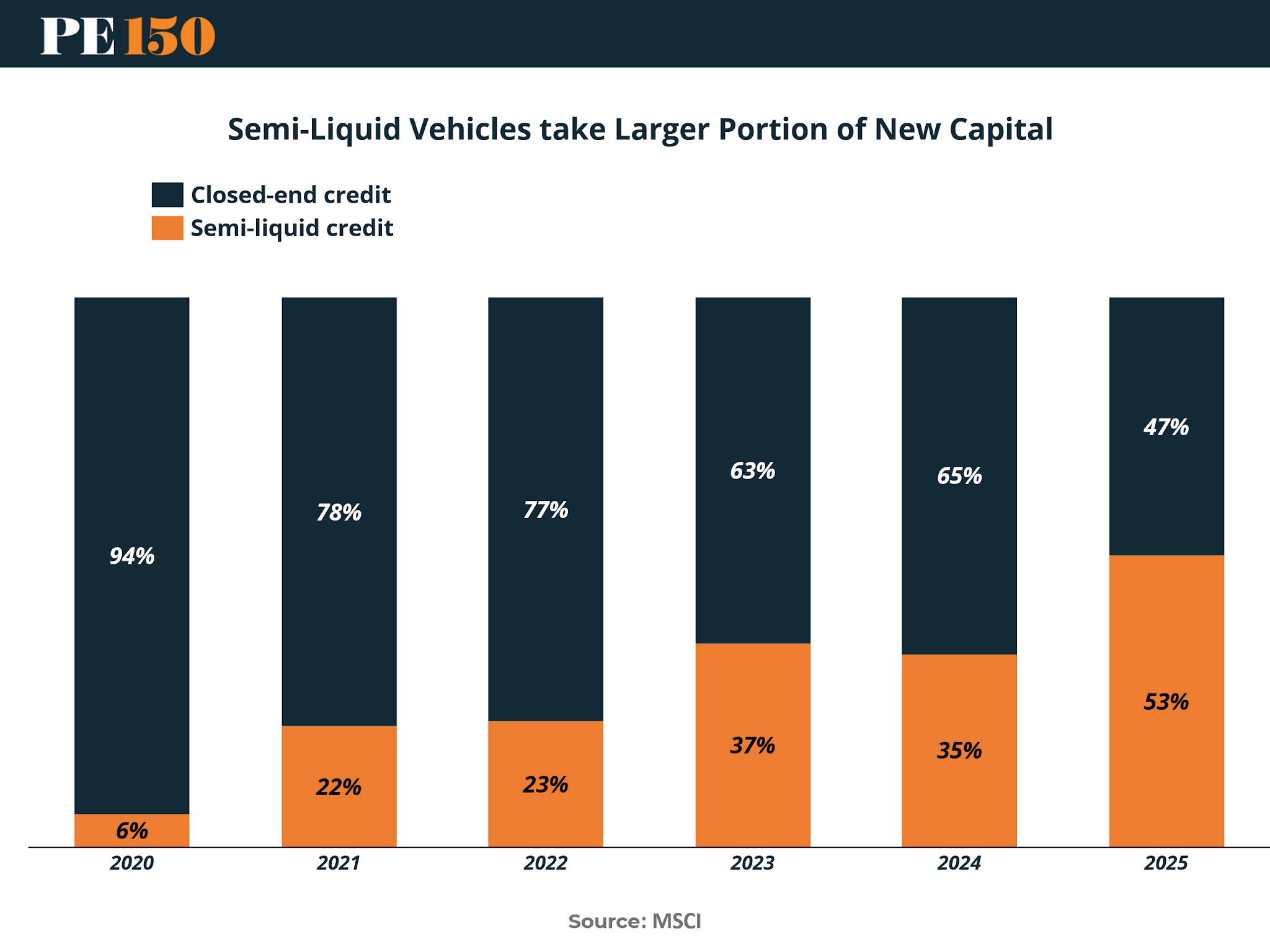

Liquidity Without Exit: The Rise of Perpetual Capital

Private credit used to run on a simple contract. Lock up capital, earn yield, exit when the cycle allows. That model is quietly breaking. Semi liquid vehicles now account for 53% of new capital in 2025, up from just 6% in 2020. In five years, the structure flipped.

This is not just product innovation. It is demand driven. Investors want exposure to private credit returns without decade long lockups, while managers want permanent or at least stickier capital to navigate uncertain exit environments. Semi liquid funds promise both. Periodic liquidity for LPs, continuous capital for managers.

But structure shapes behavior. When liquidity is offered but not guaranteed, timing mismatches emerge. Capital can request an exit faster than underlying assets can be worked out. In benign markets, this is manageable. In stressed environments, it becomes a pressure point. For turnaround investors, that pressure is where opportunity forms.

Key Takeaways from the Chart

• Semi liquid credit grew from 6% in 2020 to 53% in 2025, overtaking closed end structures in just five years

• Closed end credit fell from 94% to 47%, marking a fundamental shift in how private credit is funded

• The inflection began in 2023 at 37%, accelerating as liquidity demands intensified

• Growth plateaued slightly in 2024 at 35% before jumping again, suggesting structural rather than cyclical adoption

• More flexible capital is entering an inherently illiquid asset class, creating potential timing mismatches

• Strategic implication: in a downturn, semi liquid funds may become forced sellers or restructuring catalysts, creating entry points for turnaround capital

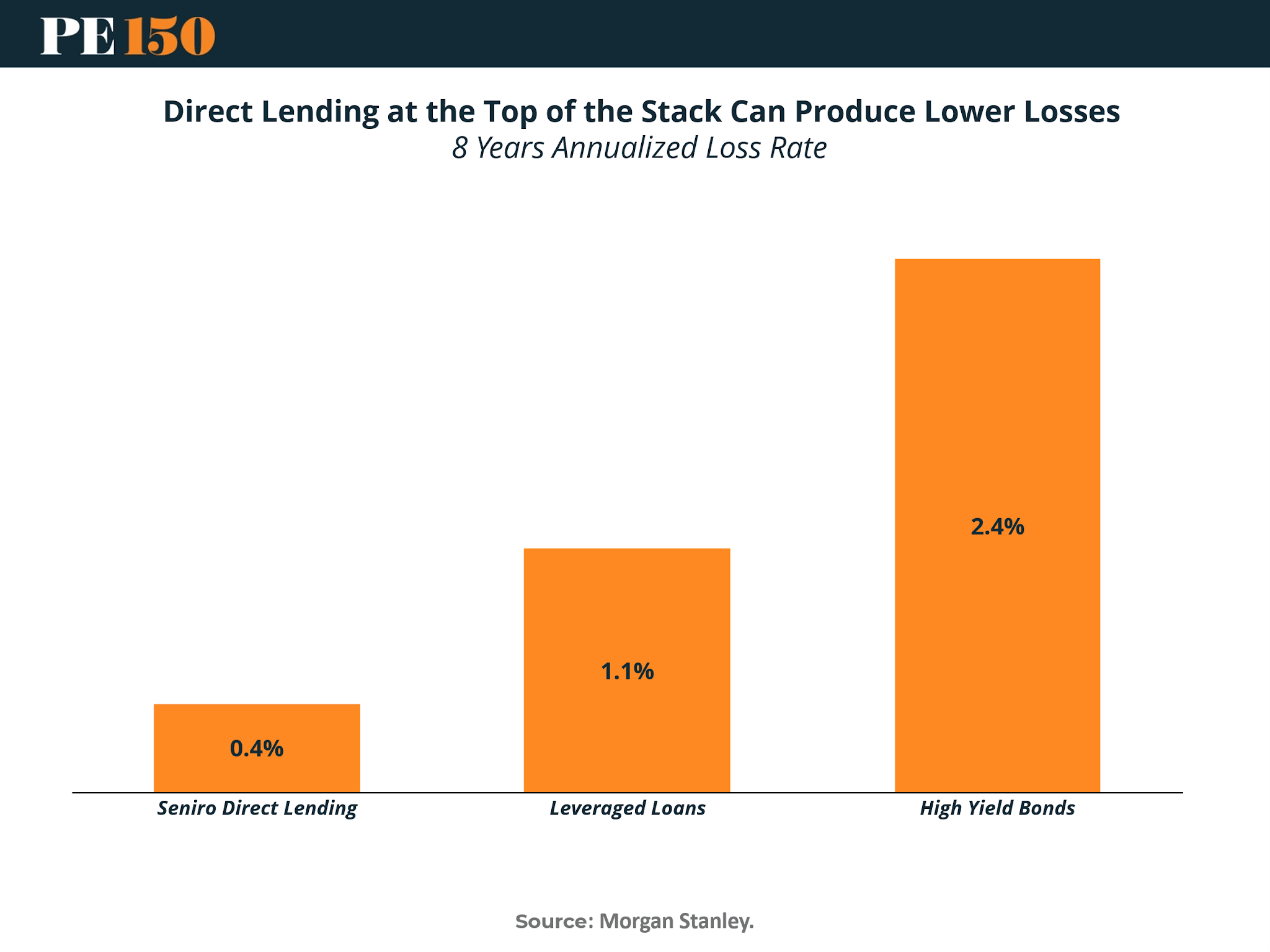

Protected on the Way In, Vulnerable on the Way Out

At first glance, private credit looks built for defense. Senior direct lending posts just 0.4% annualized losses over eight years, compared to 1.1% for leveraged loans and 2.4% for high yield bonds. Structurally, it sits at the top of the capital stack, with tighter documentation and direct lender control.

That positioning has been a feature, not a bug. Private lenders have benefited from sponsor alignment, covenant protections, and the ability to intervene early. Losses have been contained not because risk is absent, but because it is actively managed. Compared to broadly syndicated markets, where dispersion is higher and control is weaker, private credit has looked almost insulated.

But low realized losses can be misleading. In private markets, stress does not always crystallize immediately. It gets extended, amended, and restructured. For turnaround investors, that means today’s low loss rates may reflect delayed recognition rather than permanent avoidance. When the cycle forces resolution, the gap between perceived and realized risk is where opportunity lives.

Key Takeaways from the Chart

• Senior direct lending shows just 0.4% annualized losses, significantly below other credit instruments

• Leveraged loans at 1.1% and high yield bonds at 2.4% highlight the premium on structural seniority and control

• Position in the capital stack matters, top of stack exposure materially reduces realized loss rates

• Direct lender control enables early intervention, preventing issues from escalating into defaults

• Low losses do not mean low risk, they often reflect active management and delayed restructuring

• Strategic implication: turnaround opportunities emerge when suppressed losses begin to surface, forcing lenders to transition from extend and pretend to restructure and exit

Conclusion

Turnaround investing is no longer about chasing visible distress. It is about finding where stress is being deferred.

Private credit has become the primary holder of corporate risk, fueled by 2,320% growth in lending to financial institutions and supported by structures designed to smooth volatility. Low loss rates and strong Sharpe ratios are not contradictions. They are part of the same system, one that prioritizes control, flexibility, and time over immediate price discovery.

But time cuts both ways. The rise of semi liquid capital introduces liquidity expectations into an illiquid asset base. The dominance of direct lending concentrates decision making among a fragmented set of lenders. And the reliance on amendments and extensions pushes risk forward rather than resolving it. When conditions tighten, these features can quickly become fault lines.

The implication is clear. The next wave of turnaround opportunities will not begin in public markets or headline defaults. It will emerge inside private credit portfolios, where risk has been warehoused, managed, and in many cases, delayed. The investors who understand that shift will not just react to distress. They will be positioned ahead of it.

Sources & References

Morgan Stanley. Private Credit Outlook. https://www.morganstanley.com/ideas/private-credit-outlook-considerations

McKinsey. Global Private Markets Report. https://www.mckinsey.com/industries/private-capital/our-insights/global-private-markets-report/private-equity

Legal 500. Recent Trends in PC. https://www.legal500.com/guides/hot-topic/us-recent-trends-in-private-credit-and-syndicated-loan-markets/

Morningstar. KBRA Research Releases. https://www.morningstar.com/news/business-wire/20260225517482/kbra-releases-research-private-credit-q4-2025-middle-market-borrower-surveillance-compendium-stability-at-the-median-stress-at-the-margins

MSCI. Private Capital in Focus. https://www.msci.com/research-and-insights/blog-post/private-capital-in-focus-trends-to-watch-for-2026

Forbes. PC and Non Banks at Historic Heights. https://www.forbes.com/sites/mayrarodriguezvalladares/2026/03/04/bank-lending-to-private-credit-and-non-banks-is-at-historic-highs/