- PE 150

- Posts

- AI Power Demand Set to Jump 168%: A Trillion PE Opportunity

AI Power Demand Set to Jump 168%: A Trillion PE Opportunity

AI’s energy appetite is creating one of the largest infrastructure opportunities in decades.

Good morning, ! This week we're covering AI’s looming power demand and the massive infrastructure opportunity it’s creating, why buying companies at lower EBITDA multiples still drives the strongest PE returns, the growing regulatory scrutiny around valuing illiquid assets, and how evergreen funds are reshaping liquidity in private markets.

Juniper Square breaks down why new fund formats are changing what best-in-class operations looks like for PE GPs — and why more firms are moving beyond fragmented tools and legacy service models toward a fund operations partner: one connected operating model that combines software, data, and embedded expertise to improve visibility, control, and investor experience. Read the full breakdown →

DATA DIVE

The AI Power Problem

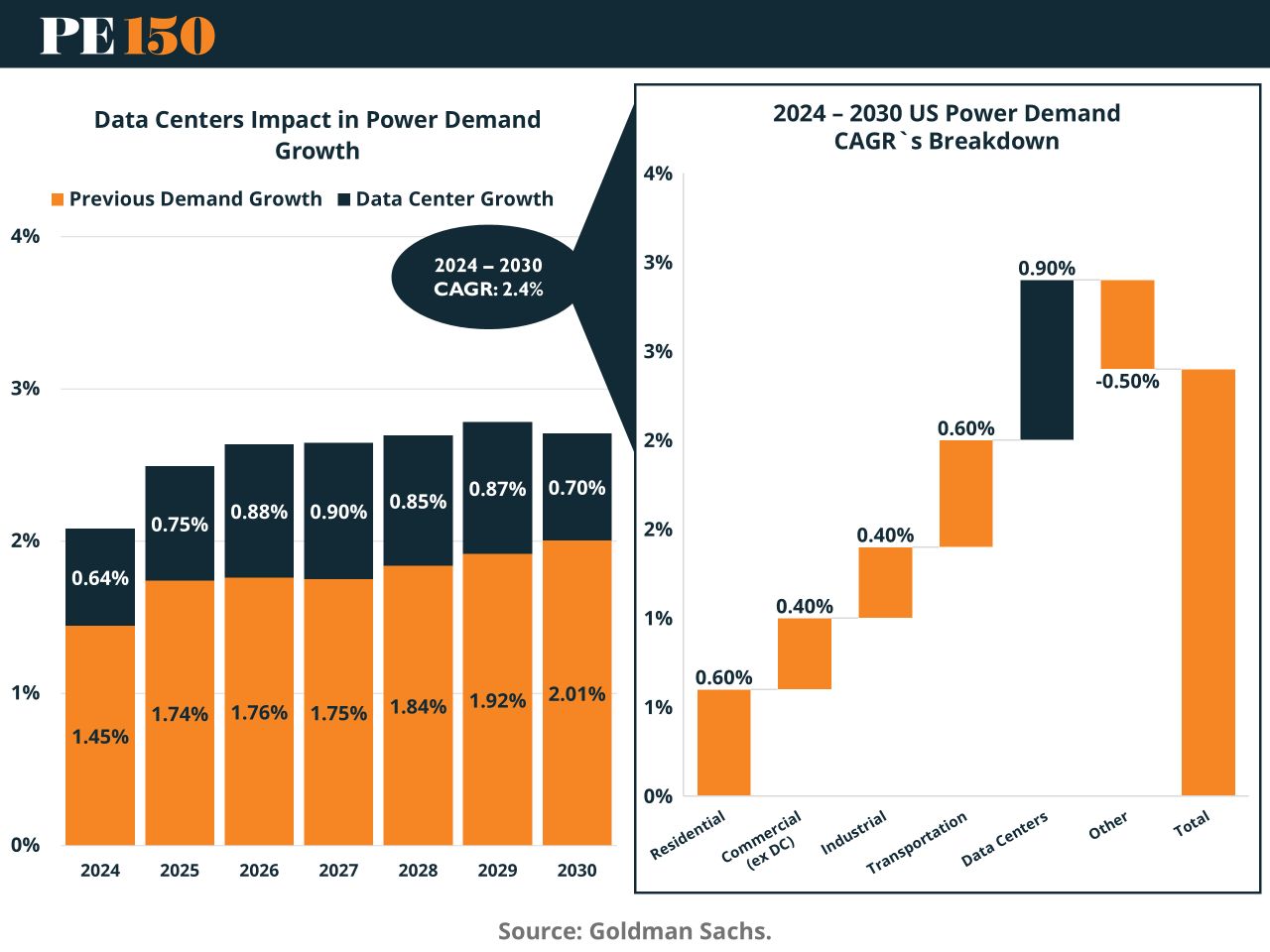

For more than a decade, electricity demand in developed markets barely moved. Efficiency gains quietly offset growth. Then AI showed up.

Data centers are becoming one of the largest drivers of incremental power demand globally. Total data center electricity consumption is expected to jump from ~399 TWh in 2023 to 1,070 TWh by 2030, a 15% CAGR. The real kicker: AI workloads alone are projected to increase power consumption 35x over that same period.

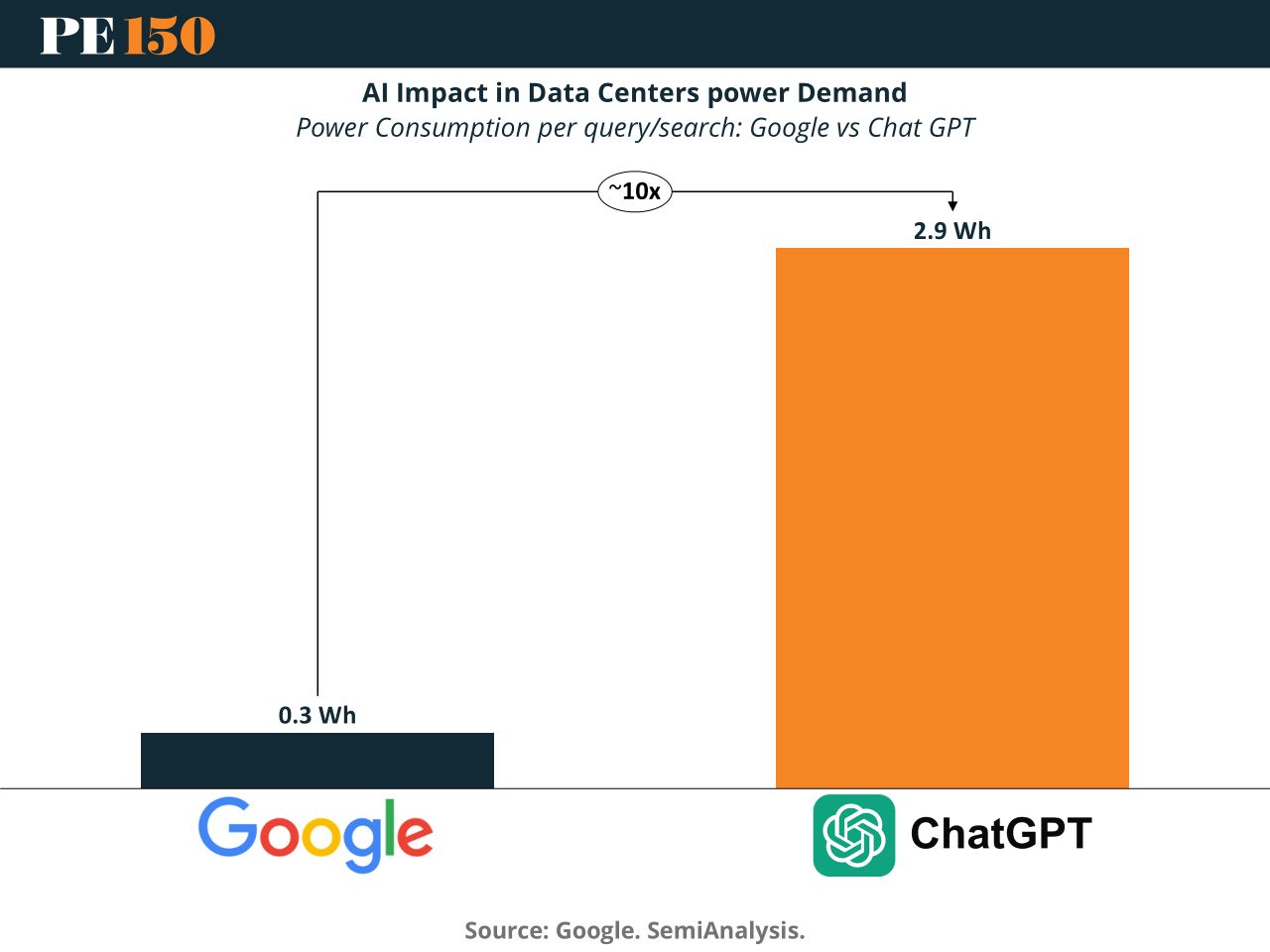

Why the surge? AI queries are energy hungry. A traditional search uses roughly 0.3 watt-hours, while an AI query consumes ~2.9 watt-hours—nearly 10x more power per request.

The bottom line: The next digital infrastructure boom isn’t just about GPUs and chips. It’s about power generation, transmission, and grid capacity—an investment cycle tailor-made for private equity infrastructure capital.

PRESENTED BY JUNIPER SQUARE

New fund formats call for a new operating model: fund operations partner.

Our report on the rise of new fund formats shows a clear shift: operating cadence is increasing, investor workflows are getting more complex, and expectations are moving toward to “always-on.”

That’s why leading PE firms are shifting to a fund operations partner model: one system of record + embedded expertise to run fundraising, investor operations, reporting, and administration with consistent data.

Juniper Square combines purpose-built software + expert fund administration services into a single connected operating model, delivering clearer visibility, fewer failure points, and a modern investor experience.

Read the full breakdown in the report.

Supporting our sponsors supports our free newsletters. Please support our sponsors!

TREND TO WATCH

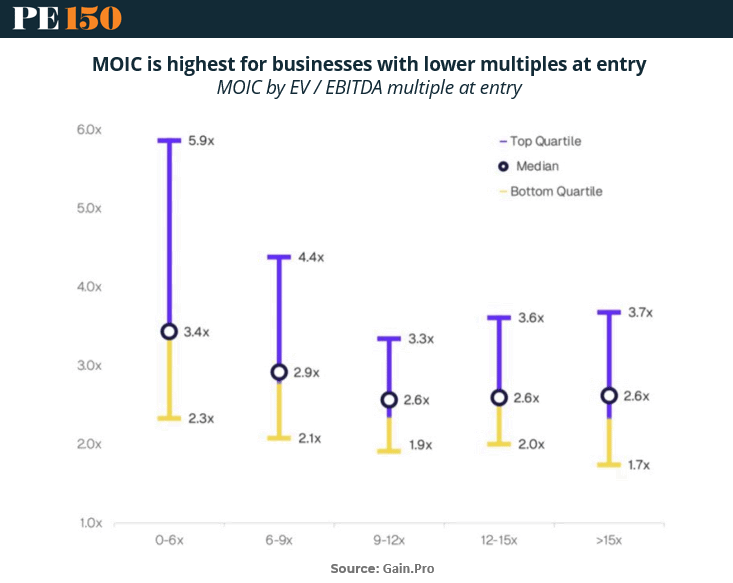

Cheap Entry, Expensive Outcomes

Private equity loves a turnaround story, but the real alpha often begins with the price you pay. Data on MOIC by entry multiple shows a clear pattern: deals bought at 0 to 6x EBITDA generate a median 3.4x MOIC, with top quartile outcomes reaching 5.9x. As entry prices climb, returns compress. Investments made at 6 to 9x deliver about 2.9x median MOIC, while deals above 9x EBITDA settle around 2.6x.

The implication is simple but uncomfortable. In an era where sponsors routinely pay double digit multiples, the math of private equity is getting harder. Higher entry prices leave less room for operational improvement, multiple expansion, or leverage driven upside.

This is why distressed and turnaround investing is quietly returning to favor. Buying broken or overlooked companies at sub 7x EBITDA restores the margin of safety that powered private equity’s best vintages.

In other words, the next cycle’s winners may not be the firms paying the highest multiples. They will likely be the ones willing to buy the messiest companies at the lowest prices. (More)

COMPLIANCE CORNER

The Illiquidity Problem

Private equity loves Illiquid Assets. Regulators are now paying closer attention to how they’re priced.

The SEC’s 2025–2026 Examination Priorities place a sharp focus on Fair Value Valuation, particularly for portfolios heavy in Private Equity, Real Estate, and Private Credit. The challenge: these assets lack daily market pricing, making valuations heavily reliant on judgment under ASC 820 and governance expectations under Rule 2a-5.

Regulators increasingly expect firms to prove—not just claim—that valuations are sound. That means independent third-party valuation expertise, consistent application of methodologies, and thorough documentation of decisions.

Guidelines like the IPEV Guidelines and SBAI governance frameworks emphasize transparency, valuation committee oversight, and investor-focused disclosures.

The bottom line: valuation is no longer just an accounting exercise—it’s a fiduciary and regulatory risk management function. (More)

PRESENTED BY 9FIN

The best PE investors know the debt. 9fin helps you know it faster.

Get AI-powered intelligence on leveraged loans, high yield bonds, private credit, and distressed debt, all in one platform.

From deal financials to covenant analysis to real-time news, 9fin gives PE professionals the edge when it matters most. Start your free 30-day trial now.

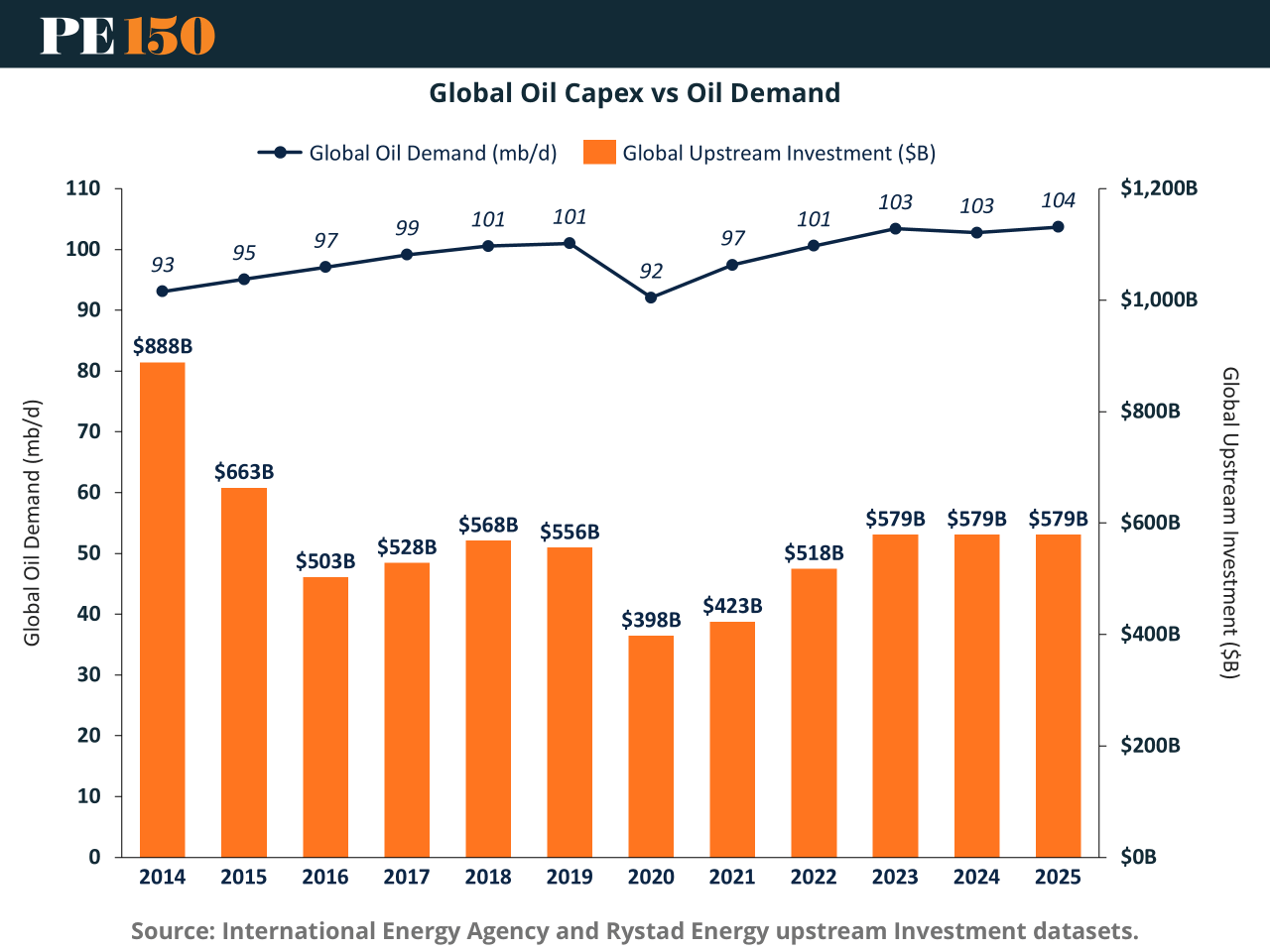

MACROVIEW

The Capital Cycle in Oil

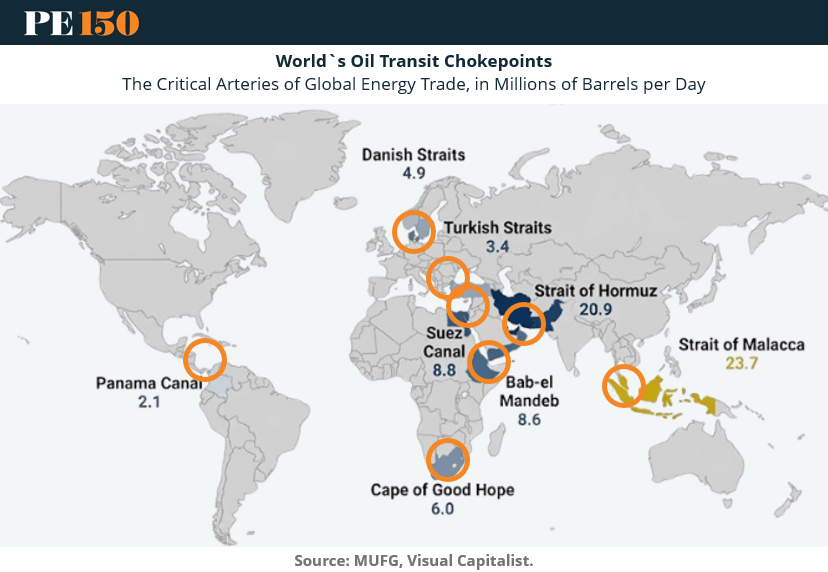

Oil is moving back toward $100 per barrel, but the real story isn’t price — it’s capital. After the 2014 crash and the 2020 pandemic, investment in oil collapsed. Exploration slowed, drilling budgets were cut, and capital moved elsewhere. Demand, however, kept growing. The result: today’s tightening supply.

Layer on top the physical reality of oil markets. Nearly 20% of global supply moves through the Strait of Hormuz, alongside other critical chokepoints like the Strait of Malacca and the Suez Canal. These corridors were built for efficiency, not resilience — meaning disruptions can push prices higher very quickly.

The key takeaway: price is a lagging signal; capital flows are the leading one.

By the time oil reaches $100, the real opportunity in energy has usually already happened — when prices were low, capital had fled, and nobody wanted the assets. (More)

LIQUIDITY CORNER

Evergreen Funds Rewrite the Liquidity Playbook

Private markets are quietly experimenting with a new promise: liquidity without exits.

Semi liquid evergreen funds are approaching $500 billion in assets, with AUM growing more than 30% in the twelve months through September 2025. Even more notable, wealth investors now account for about 20% of assets, marking a structural shift in who participates in private markets.

The appeal is obvious. Evergreen vehicles eliminate the traditional fund cycle of capital calls and decade long lockups. Instead, they offer continuous capital deployment and periodic redemption windows. For investors accustomed to public market liquidity, the model feels familiar.

But the structure introduces a delicate balance. Managers must constantly manage the tension between deploying capital into illiquid assets and meeting redemption requests. Because subscriptions and redemptions occur at NAV, valuation discipline becomes far more consequential.

Performance data shows promise. Evergreen private credit funds outperformed closed end funds by roughly 160 basis points over the past year, though results have varied across cycles.

The bigger implication is structural. If evergreen vehicles continue scaling, the private markets industry may shift from episodic fundraising to continuous capital.

Liquidity, in other words, is no longer just an exit strategy. It is becoming a product feature. (More)

Get the new Juniper Square report to see why new fund formats are changing what best-in-class GP operations looks like. Get the report →

Supporting our sponsors supports our free newsletters. Please support our sponsors!

“The four most dangerous words in investing are: ‘This time it’s different.’”

Sir John Templeton