- PE 150

- Posts

- The Next Energy Frontier

The Next Energy Frontier

How AI, Data Centers, and Infrastructure Constraints Are Reshaping Power Markets and Creating a New Opportunity Set for Private Equity

Introduction: A Structural Shift in Electricity Demand

For more than a decade, electricity demand in developed economies remained largely stagnant. Improvements in efficiency, the shift toward service economies, and technological upgrades such as LED lighting offset incremental consumption. That dynamic is now reversing.

The rapid expansion of artificial intelligence, cloud computing, and hyperscale data infrastructure is creating a structural step change in electricity demand. Data centers are no longer a marginal consumer of power. They are becoming one of the largest incremental drivers of load growth across developed power markets.

This shift is creating an investment cycle across the energy ecosystem. New generation capacity, natural gas supply, transmission infrastructure, nuclear energy, and advanced grid technologies are all required to support this expansion. Capital requirements are substantial and project timelines are long. These characteristics align closely with the investment horizon and capital structure expertise of private equity.

The energy sector is entering a new phase where power availability becomes a competitive advantage for technology infrastructure. Investors that can finance and develop generation capacity, grid expansion, and firm baseload power are positioned to capture the economic value created by the next wave of digital infrastructure.

The AI Revolution Is Driving a New Power Demand Cycle

The first step in understanding the new energy landscape is recognizing the magnitude of electricity demand generated by artificial intelligence and hyperscale computing.

Generative AI is expected to expand into a trillion-dollar market over the coming decade. Large language models, machine learning infrastructure, and inference workloads require significant computational power and large-scale data processing.

Data centers provide the physical infrastructure for this digital economy. They host the processors, GPUs, storage systems, and networking capacity required to train and run AI models.

As AI adoption accelerates across industries, electricity consumption within these facilities is expanding rapidly.

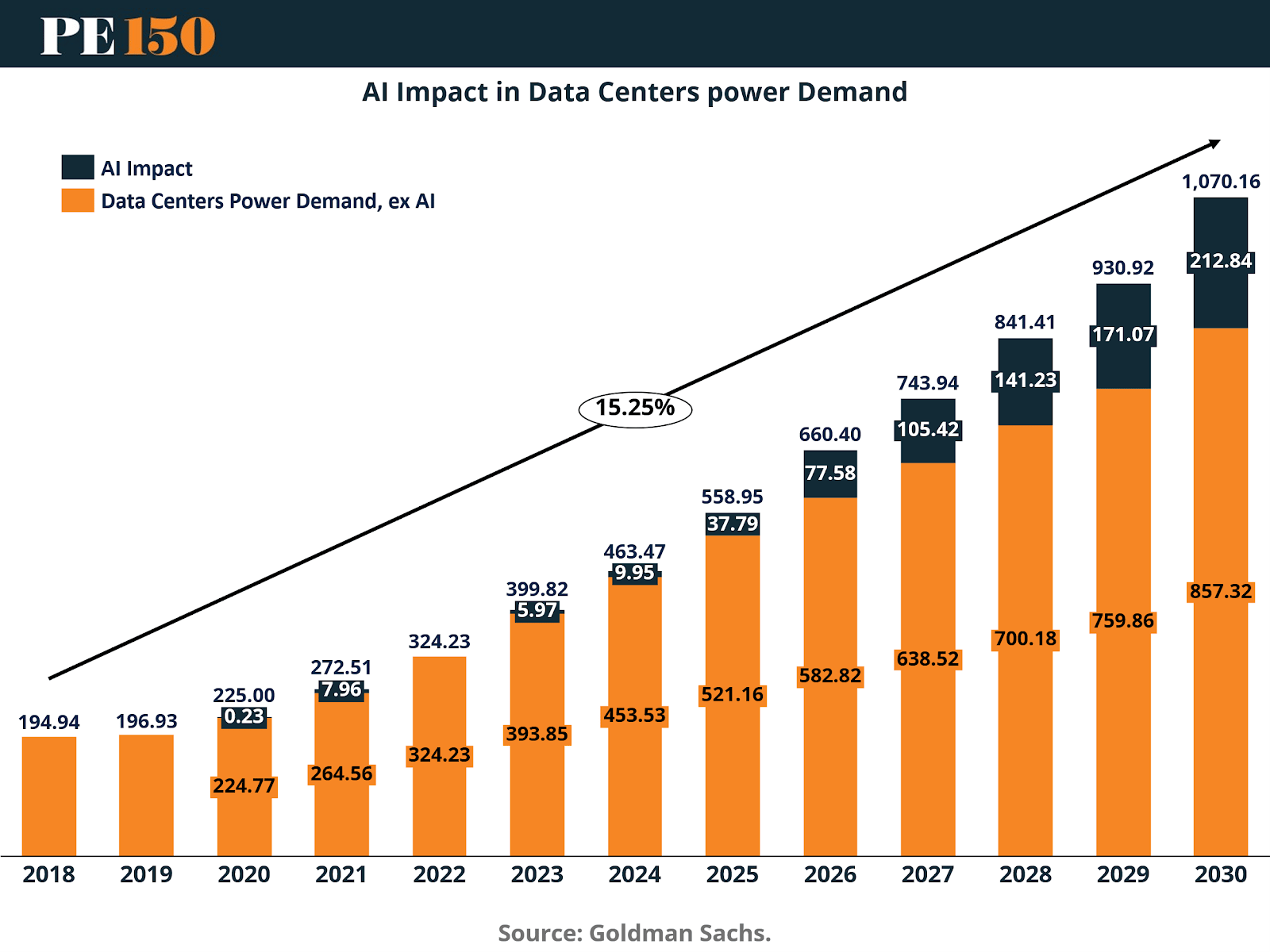

AI Workloads Are Rapidly Expanding Data Center Electricity Demand

This chart illustrates the scale of expected growth in electricity consumption from data centers.

Total data center power demand rises from approximately 399 TWh in 2023 to 1,070 TWh by 2030, implying a 15.25% compound annual growth rate.

Within this total, the contribution from AI workloads grows dramatically.

AI electricity consumption increases from 5.97 TWh in 2023 to 212.84 TWh by 2030. This represents more than a 35-fold increase in energy consumption associated with AI processing.

Even traditional data center workloads grow significantly. Non-AI demand rises from 393.85 TWh in 2023 to 857.32 TWh in 2030, reflecting the continued expansion of cloud computing, enterprise data storage, and digital services.

By the end of the decade, AI alone accounts for roughly 20% of total data center electricity demand.

This surge in energy requirements is forcing utilities, developers, and policymakers to reassess the future structure of power generation.

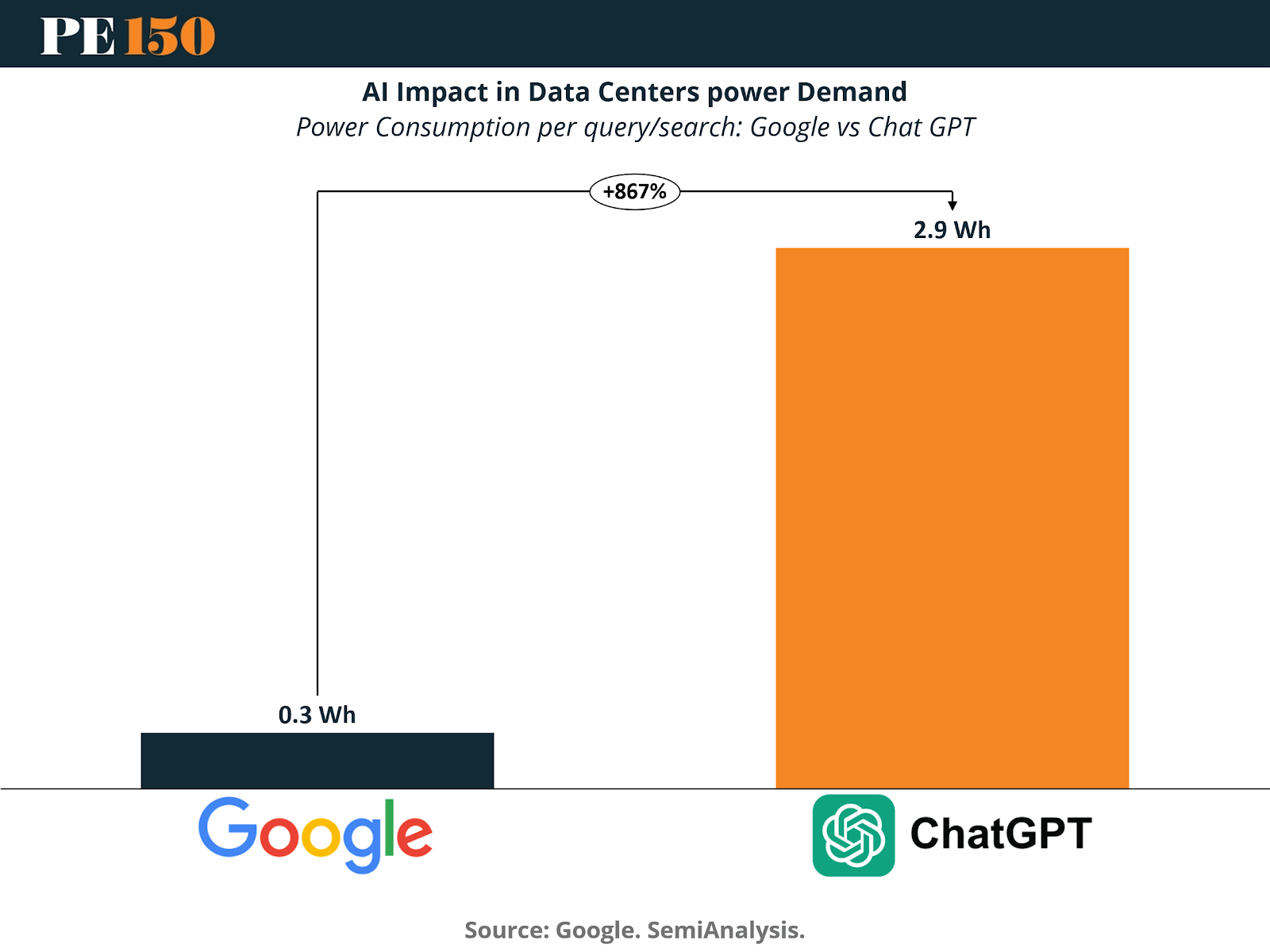

AI Queries Are Significantly More Energy Intensive

One reason electricity demand is accelerating is the significantly higher energy intensity of AI computation.

A traditional Google search requires approximately 0.3 watt-hours of electricity.

A ChatGPT query consumes approximately 2.9 watt-hours, almost ten times more power per request.

The implication is that even modest behavioral shifts toward AI-assisted search, coding, and enterprise workflows will substantially increase electricity consumption across the digital economy.

When multiplied across billions of daily queries and enterprise applications, the energy impact becomes enormous.

This dynamic explains why power procurement has become a strategic priority for data center developers and hyperscale cloud providers.

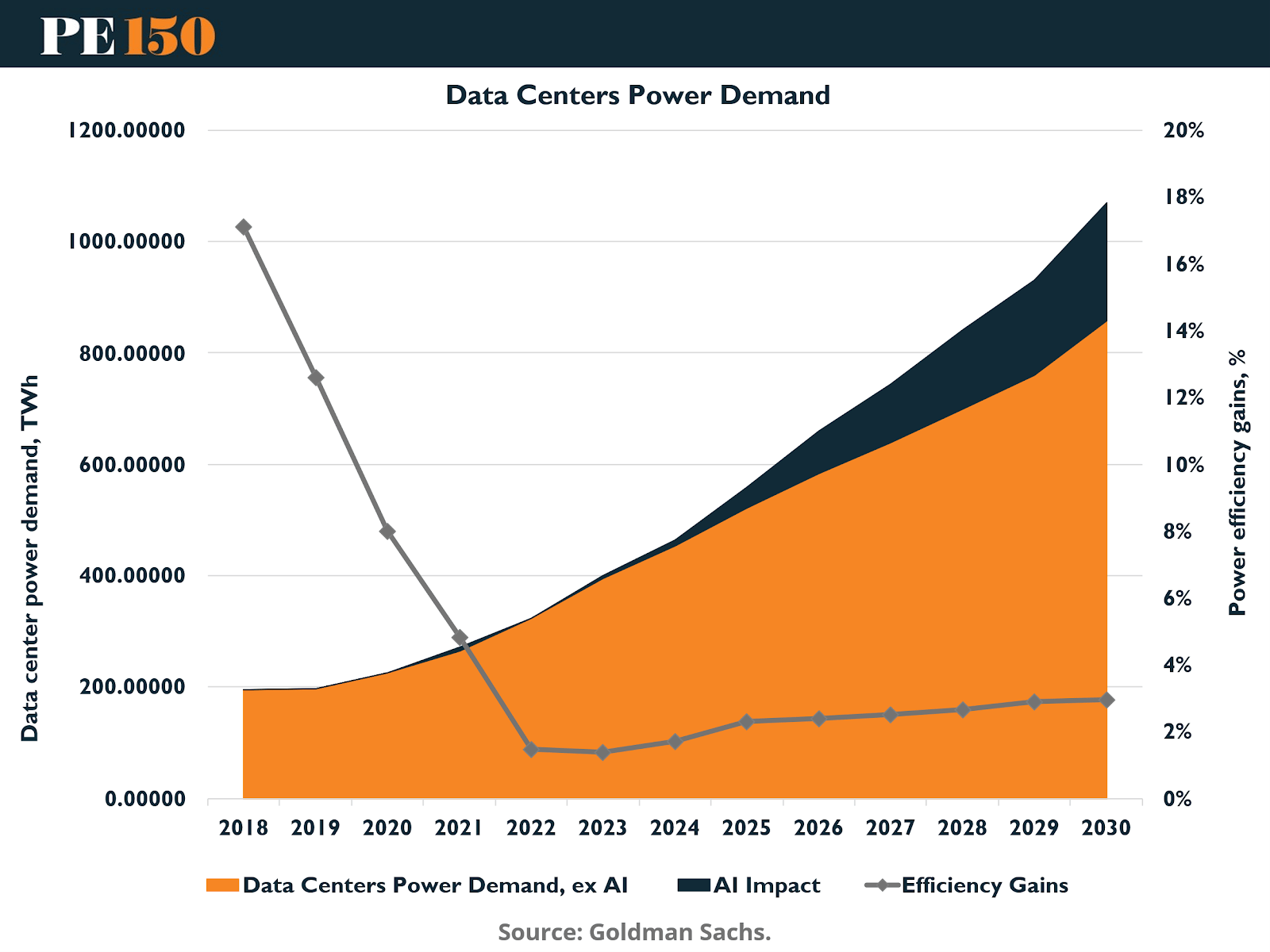

Efficiency Improvements Are No Longer Offsetting Demand Growth

Efficiency gains historically kept electricity demand from data centers manageable.

However, the chart demonstrates that efficiency improvements are now slowing while demand growth accelerates.

Total data center electricity consumption increases from about 200 TWh in 2018 to more than 1,000 TWh by 2030.

Meanwhile, power efficiency gains decline sharply. Efficiency improvements fall from approximately 17% in 2018 to roughly 3% by 2030.

The result is that improvements in cooling systems, server utilization, and chip design are no longer sufficient to offset the rapid growth in compute requirements.

Electricity supply must expand to meet demand.

Data Centers Are Becoming the Largest Driver of Power Demand Growth

The expansion of AI infrastructure is now reshaping national electricity demand forecasts. After nearly a decade of flat consumption, the United States is entering a period of sustained power demand growth.

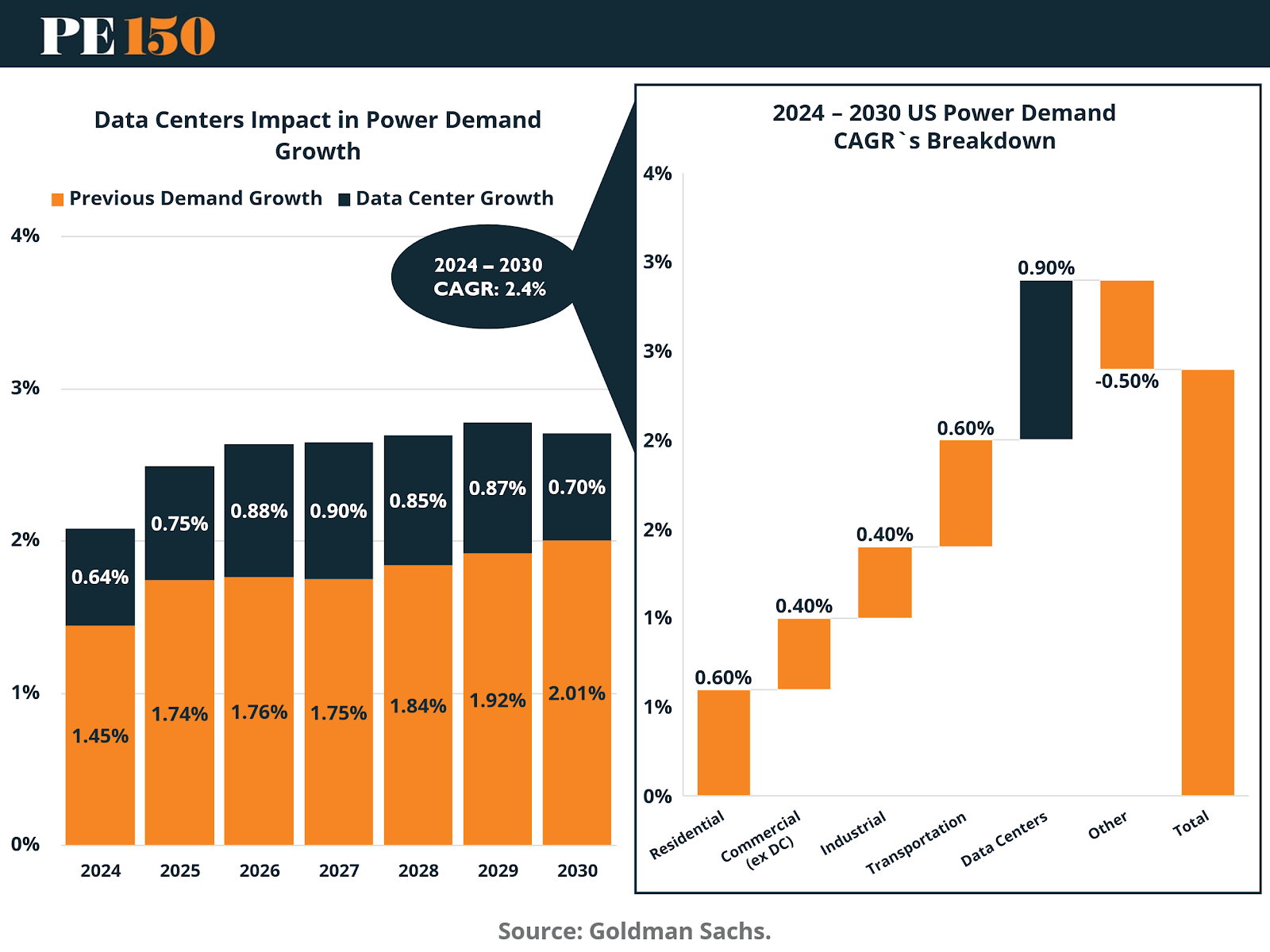

Data Centers Will Drive the Majority of U.S. Demand Growth

The chart breaks down the drivers of U.S. electricity demand growth between 2024 and 2030.

Total power demand is expected to grow at 2.4% annually, compared with roughly zero growth over the previous decade.

Within that growth:

Data centers contribute 0.90% CAGR

Residential demand contributes 0.60%

Transportation electrification contributes 0.60%

Commercial demand contributes 0.40%

Industrial demand contributes 0.40%

Data centers therefore represent the single largest contributor to U.S. electricity demand growth.

By 2030, they are expected to account for 8% of total national electricity consumption, compared with roughly 3% today.

Meeting this demand will require new generation capacity, transmission upgrades, and significant grid investment.

Meeting the Demand: The Next Wave of Generation Investment

Supporting the rapid expansion of electricity consumption requires a massive buildout of power generation capacity.

Utilities and developers are already planning record levels of new capacity additions.

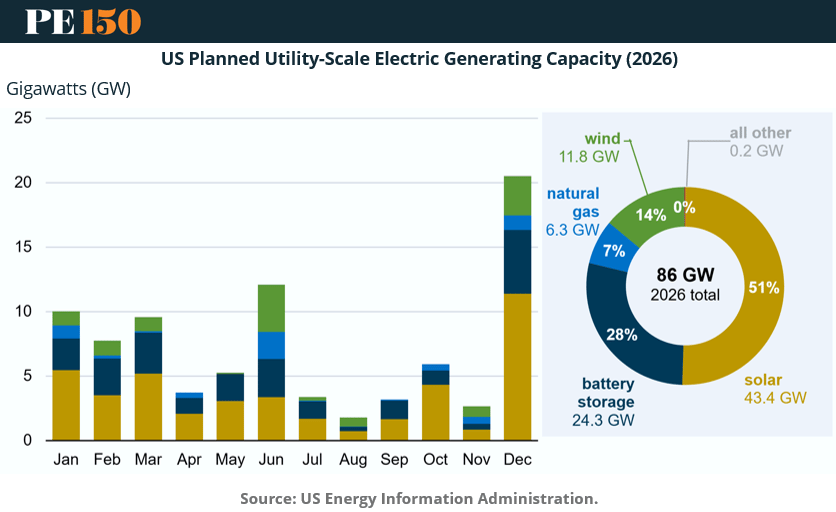

Renewable Energy and Storage Lead Capacity Additions

Developers plan to add 86 gigawatts of new utility-scale capacity in 2026, representing the largest annual addition in decades.

The composition of this capacity reflects the evolving energy mix:

Solar: 43.4 GW (51%)

Battery Storage: 24.3 GW (28%)

Wind: 11.8 GW (14%)

Natural Gas: 6.3 GW (7%)

Solar and battery storage dominate new capacity installations due to declining costs and supportive policy frameworks.

However, intermittent renewable energy sources require complementary generation technologies capable of providing reliable power during periods when solar and wind output decline.

Natural gas and nuclear energy therefore remain essential components of the future power mix.

Natural Gas Remains a Critical Bridge Fuel

Despite the expansion of renewables, natural gas continues to play an important role in electricity generation.

Gas plants provide dispatchable power, fast ramping capability, and reliability that complements intermittent renewable resources.

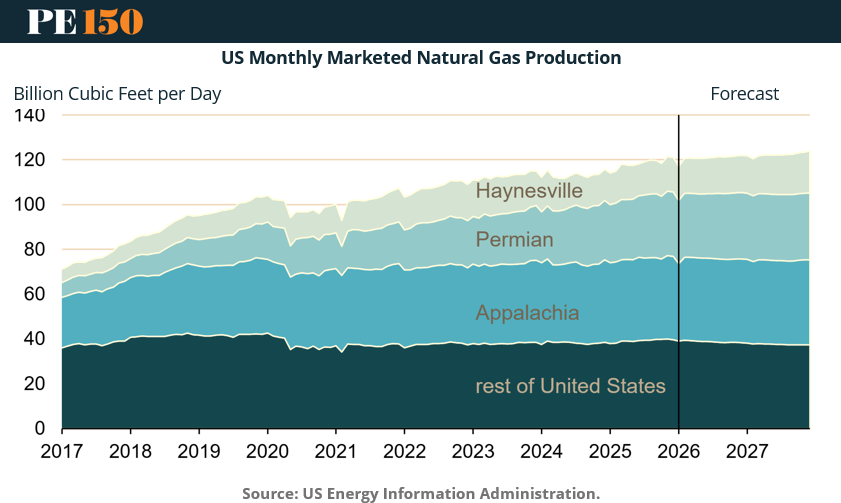

U.S. Natural Gas Production Continues to Expand

U.S. marketed natural gas production has grown steadily from roughly 70 billion cubic feet per day in 2017 to more than 100 Bcf/d in 2024.

Production is expected to continue rising toward 120 Bcf/d by 2027.

Several major shale basins drive this growth:

Appalachia remains the largest producing region

The Permian Basin continues expanding alongside oil production

The Haynesville basin is increasing output to supply LNG and power markets

Growing domestic gas supply provides a relatively low-cost fuel source for new power plants needed to support data center expansion.

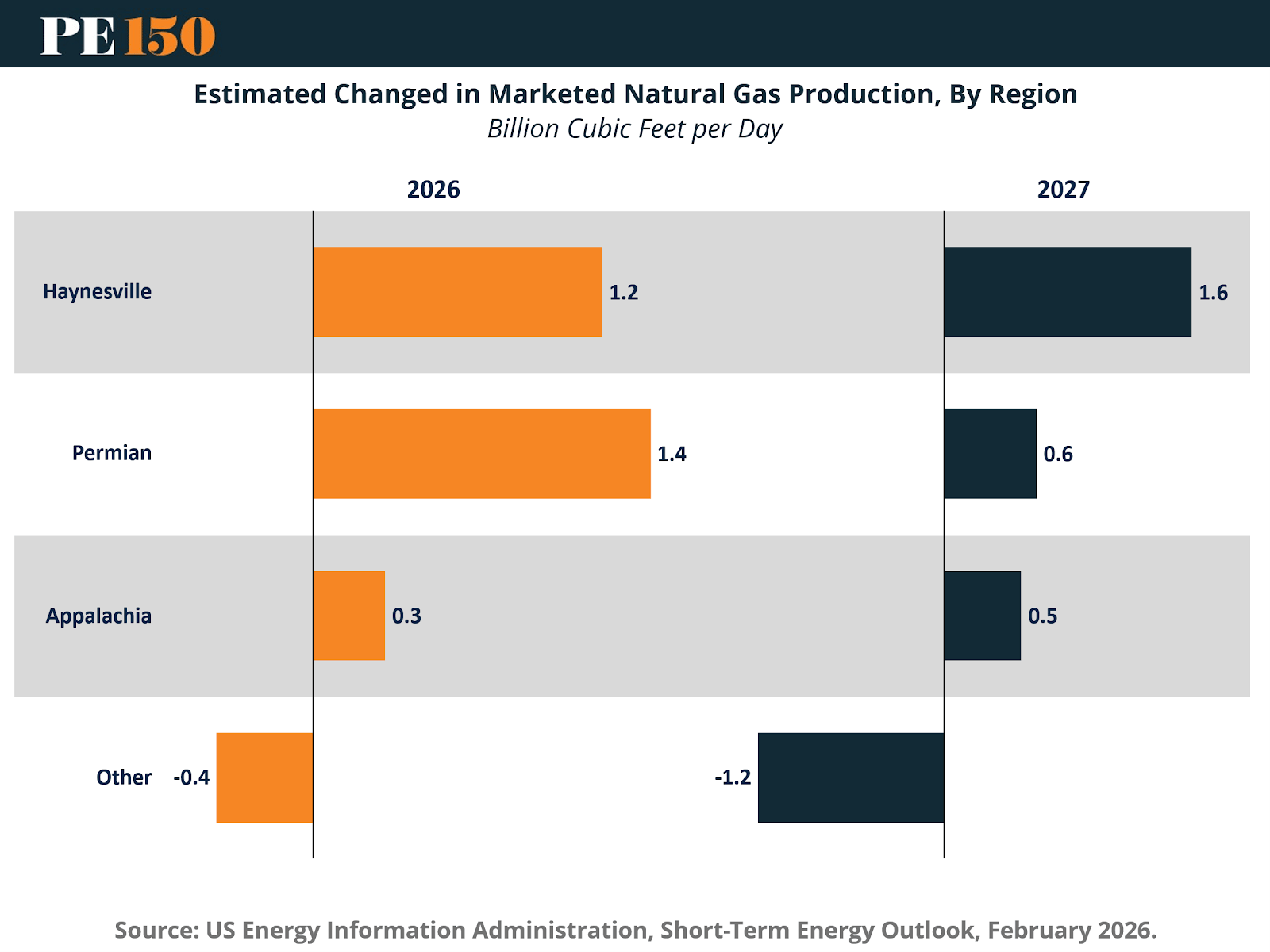

Regional Production Growth Supports Power Generation Expansion

The regional breakdown of production growth highlights where incremental supply is emerging.

In 2026:

Permian Basin production increases by 1.4 Bcf/d

Haynesville increases by 1.2 Bcf/d

Appalachia increases by 0.3 Bcf/d

In 2027:

Haynesville adds 1.6 Bcf/d

Permian adds 0.6 Bcf/d

Appalachia adds 0.5 Bcf/d

These regions provide the natural gas supply necessary for new generation capacity in power markets experiencing rapid load growth.

For investors, midstream infrastructure and gas-fired generation remain critical components of the energy investment landscape.

Nuclear Energy Is Re-Emerging as a Strategic Power Source

While natural gas provides near-term flexibility, nuclear energy offers a long-term solution for reliable, carbon-free baseload electricity.

The nuclear sector experienced decades of stagnation after reaching peak generation levels in the early 2000s. Aging reactor fleets, high construction costs, and regulatory hurdles slowed new development.

However, rising electricity demand and decarbonization goals are bringing nuclear power back into focus.

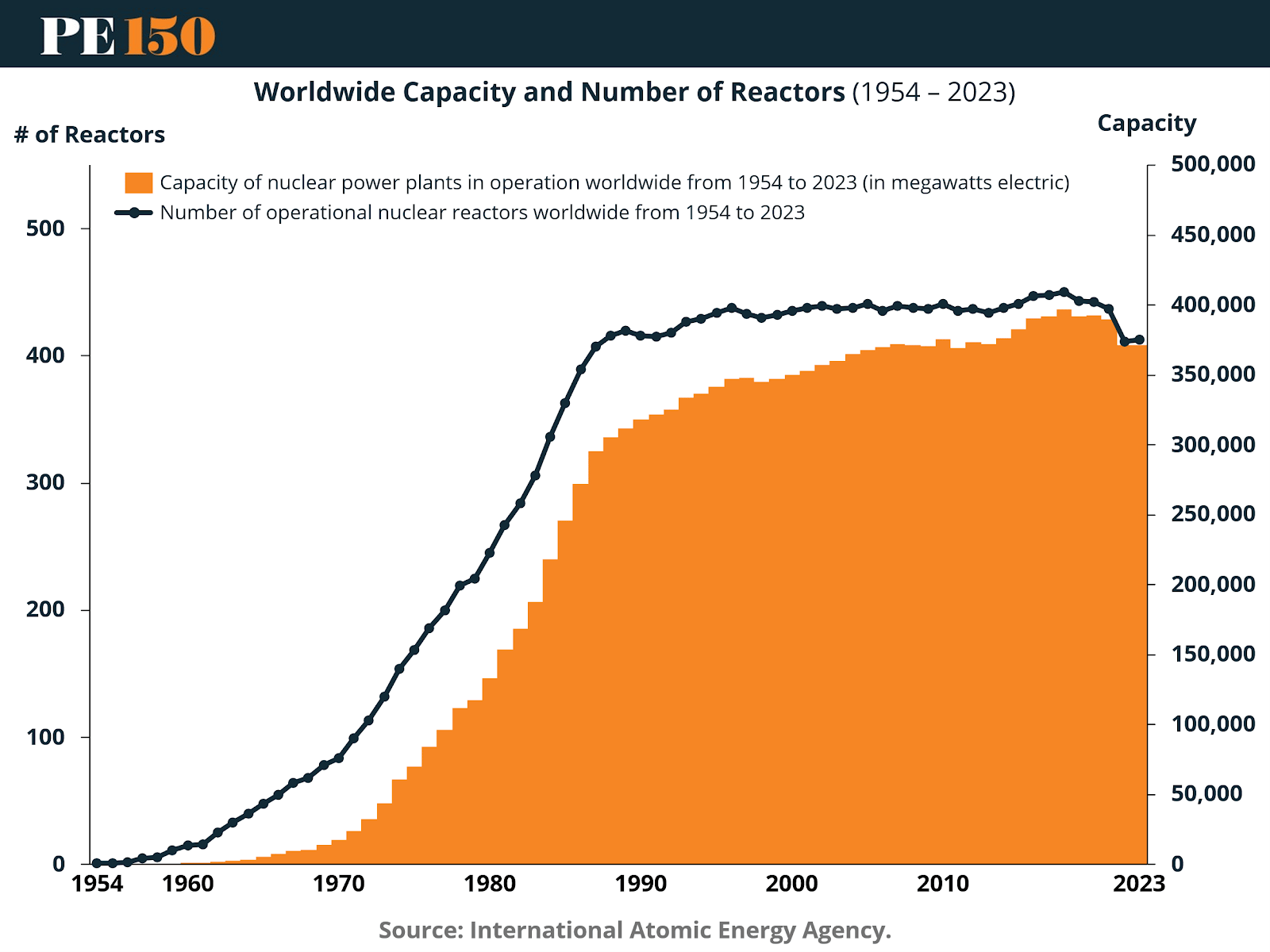

Nuclear Capacity Has Plateaued but Could Expand Significantly

Global nuclear capacity grew rapidly from the 1960s through the early 2000s.

By the mid-2000s, the world operated roughly 440 nuclear reactors with total capacity exceeding 400 GW.

Since then, the number of operational reactors has remained relatively stable. Aging plants have been retired while relatively few new facilities were built.

Total global nuclear capacity has therefore plateaued over the past two decades.

This stagnation reflects high capital costs and long development timelines, rather than technological limitations.

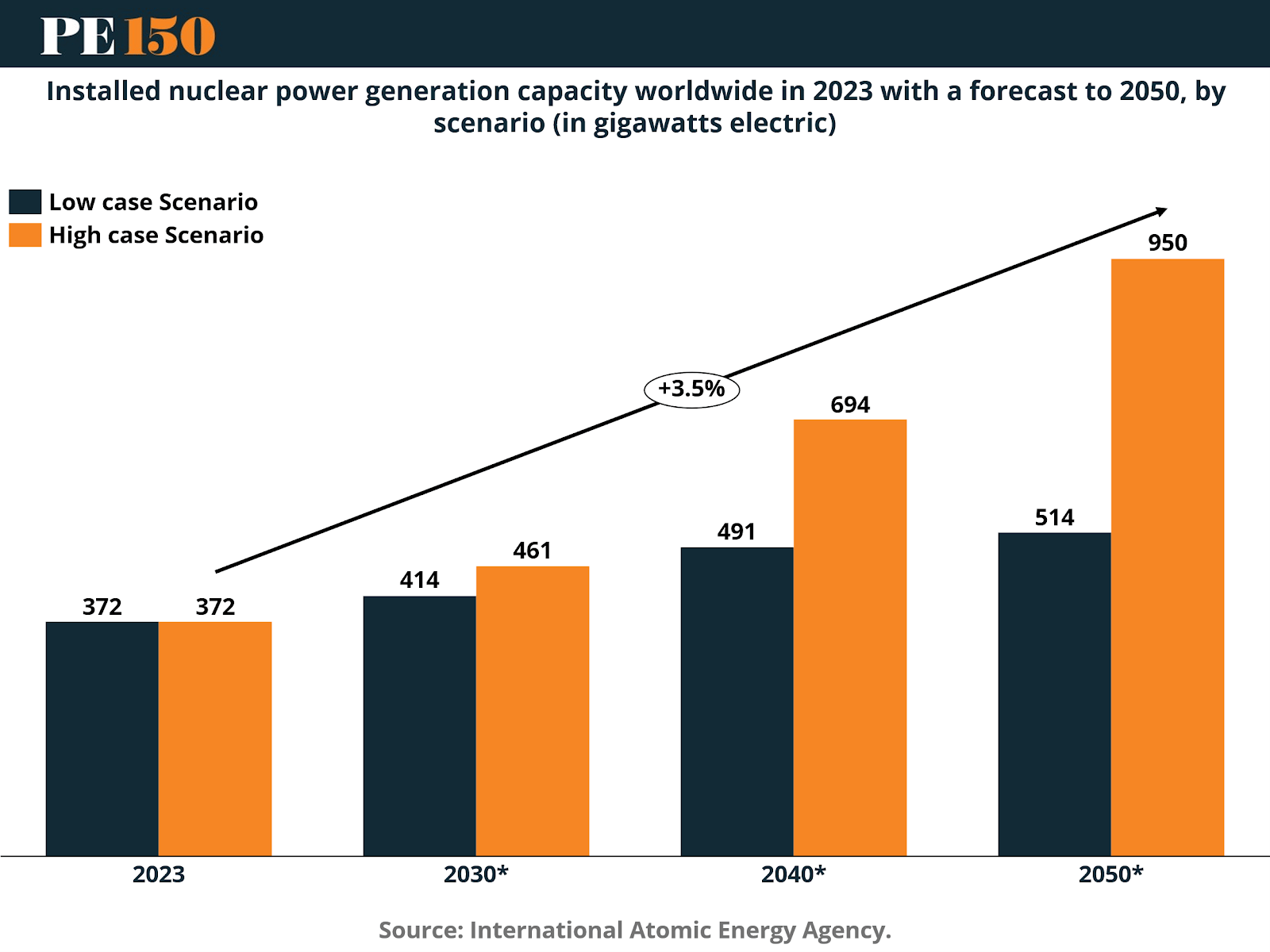

Nuclear Could Double Global Capacity by 2050

Future nuclear growth depends heavily on policy decisions and investment.

Under conservative projections, global nuclear capacity rises from 372 GW in 2023 to 514 GW by 2050.

Under an aggressive expansion scenario, capacity could reach 950 GW by 2050, more than doubling current levels.

This high-growth scenario assumes supportive regulatory frameworks and increased capital investment in nuclear development.

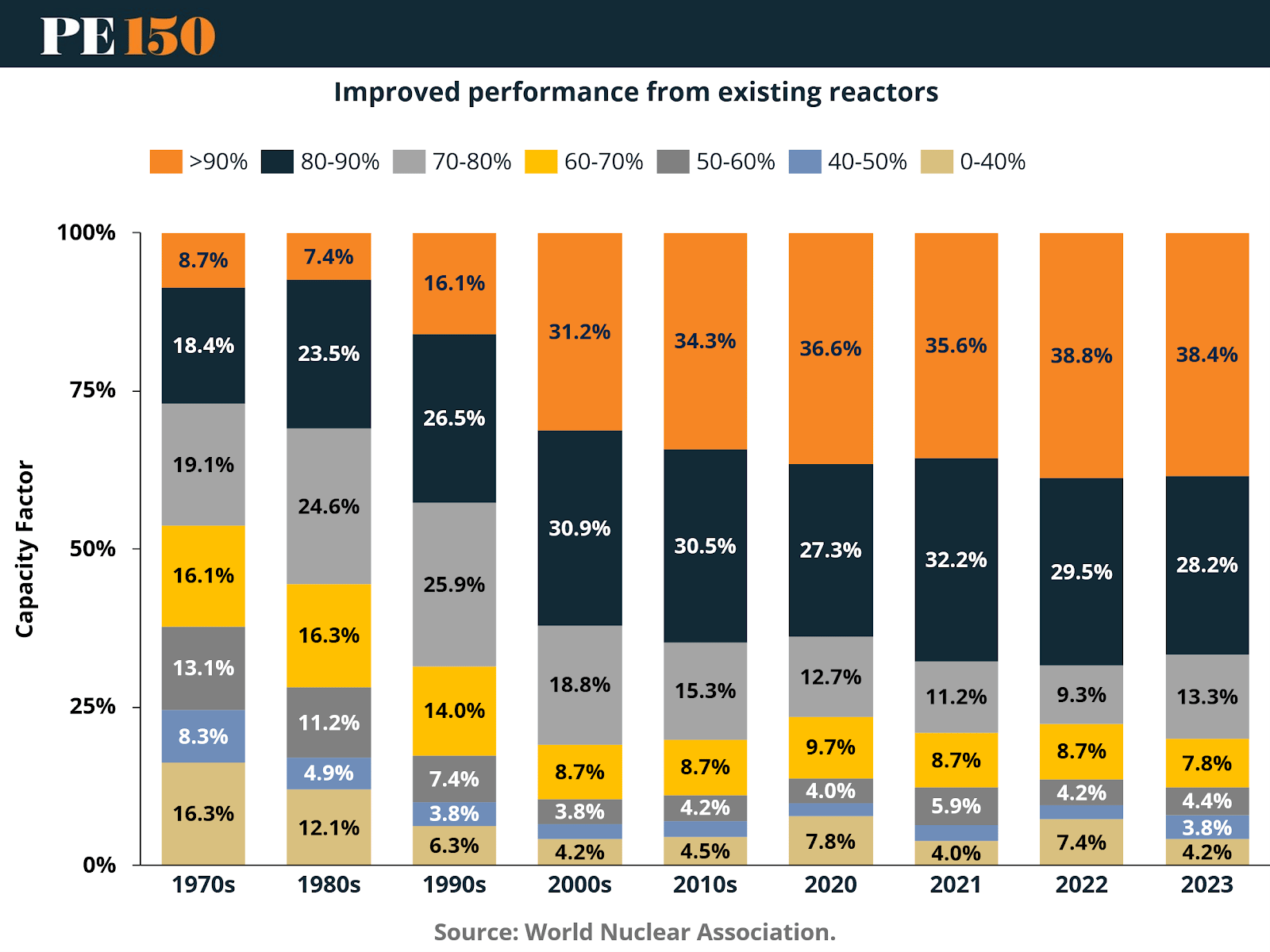

Existing Reactors Are Becoming More Efficient

Operational performance of nuclear reactors has improved dramatically over time.

In the 1970s, only 8.7% of reactors operated above 90% capacity factor.

By 2023, nearly 40% of reactors achieve capacity factors above 90%.

At the same time, reactors operating below 60% capacity have declined sharply.

These improvements reflect advances in reactor maintenance, operational management, and digital monitoring systems.

Higher utilization rates allow existing facilities to generate more electricity without building new reactors.

Grid Infrastructure Is the Next Bottleneck

Expanding generation capacity alone will not solve the electricity supply challenge.

Transmission infrastructure and grid interconnection processes are increasingly becoming the limiting factors in deploying new generation assets.

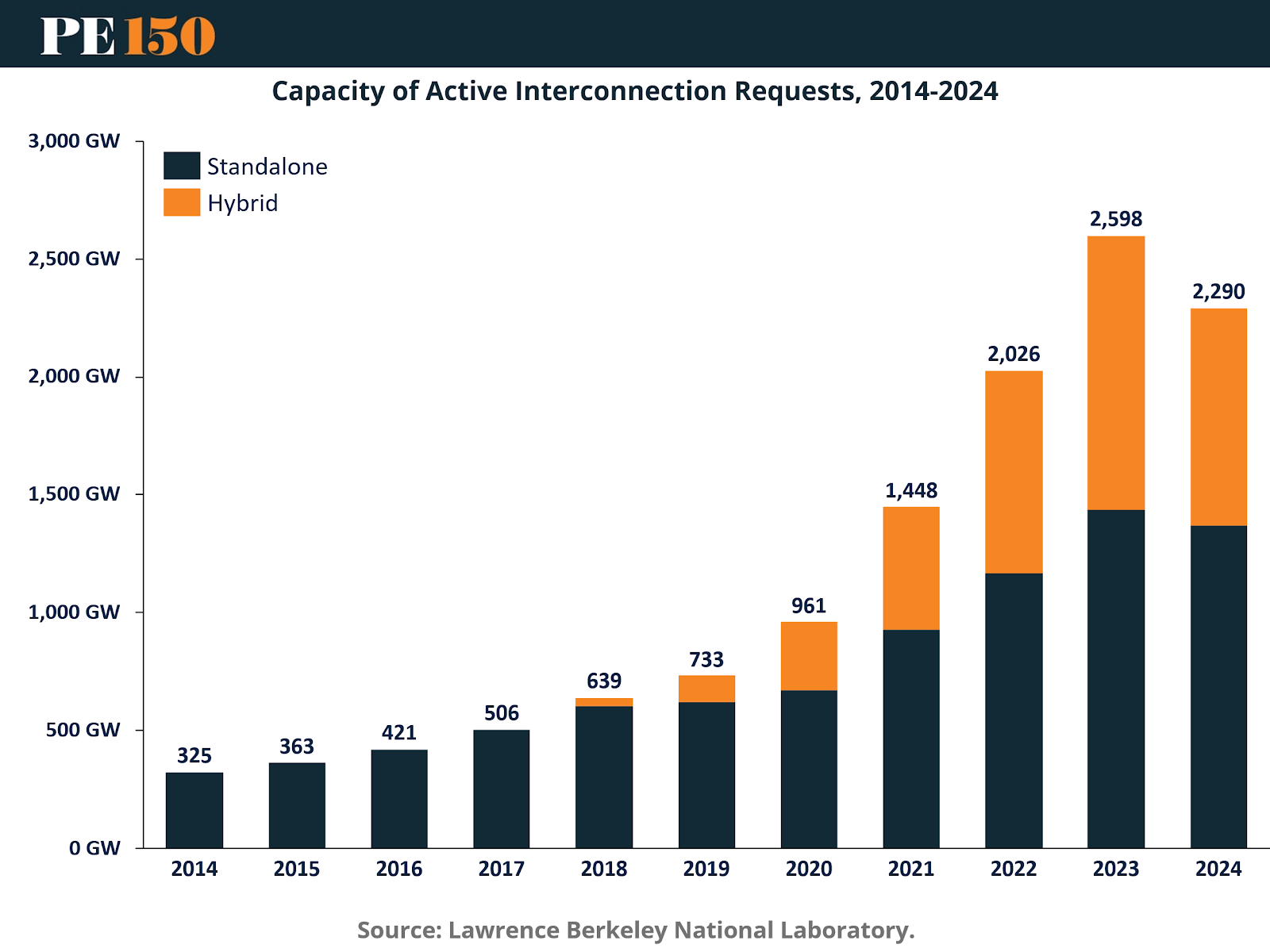

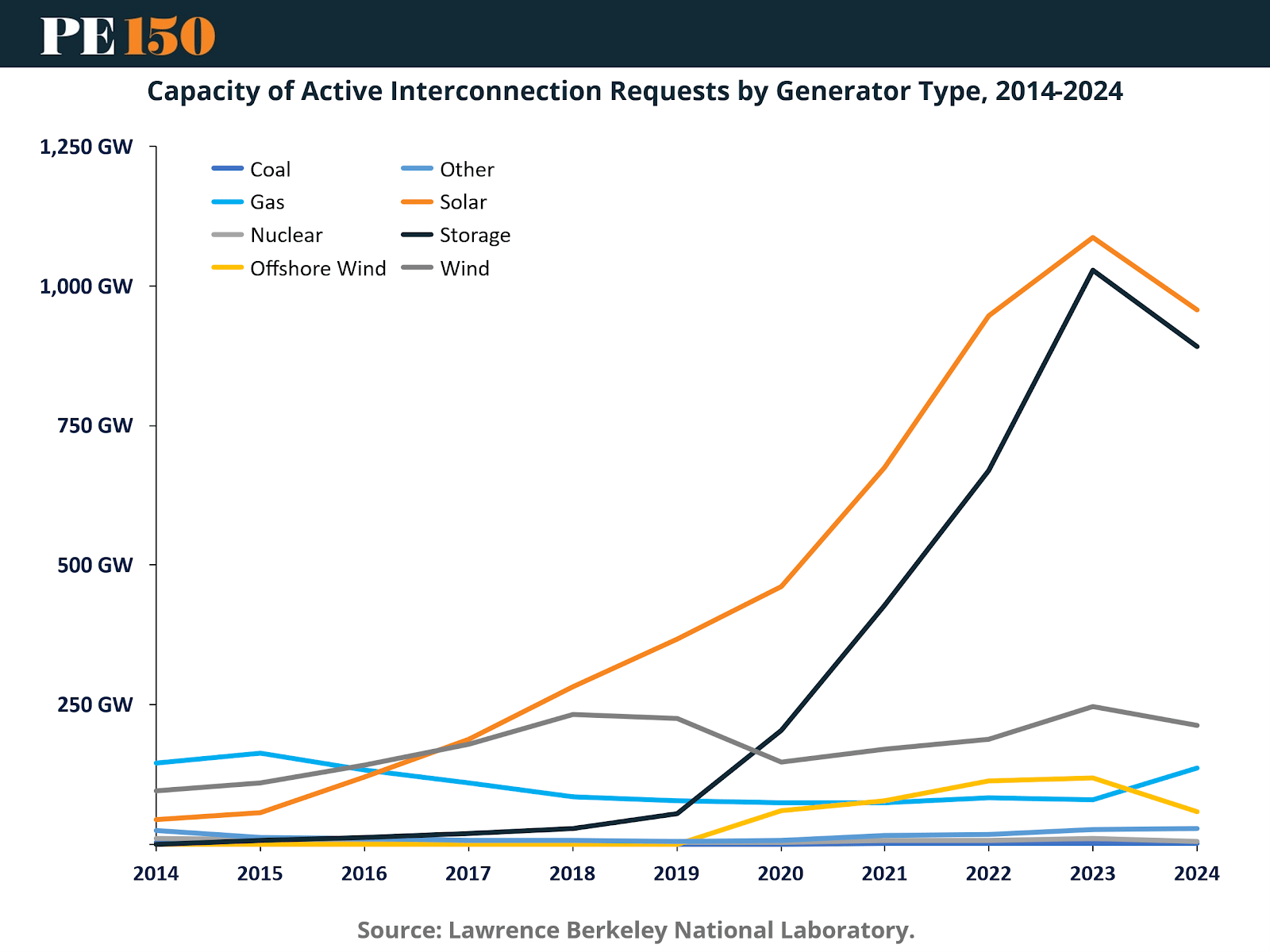

Interconnection Queues Have Reached Record Levels

The chart shows the dramatic growth in power generation projects seeking connection to the U.S. grid.

Active interconnection requests increased from 325 GW in 2014 to 2,598 GW in 2023, before declining slightly to 2,290 GW in 2024.

This represents more than a sevenfold increase in proposed generation capacity.

The majority of these projects involve renewable energy and energy storage systems.

However, many of these projects will never be built due to transmission constraints, regulatory delays, and financing challenges.

Solar and Storage Dominate Interconnection Pipelines

Solar generation has grown dramatically in interconnection queues.

Solar requests rise from less than 50 GW in 2014 to more than 1,000 GW by 2023.

Battery storage projects also expand rapidly, exceeding 1,000 GW of proposed capacity by 2023.

Wind projects remain significant but grow at a slower pace.

These trends highlight both the scale of planned energy investment and the bottlenecks in transmission infrastructure required to connect these resources to the grid.

Private Equity and the Financing of the New Energy System

The scale of capital required to support the next generation of electricity infrastructure is enormous.

Data center growth alone is expected to require tens of gigawatts of new generation capacity and hundreds of billions of dollars in grid investment.

Transmission upgrades, power plant construction, nuclear development, and gas infrastructure all require large upfront capital commitments and long investment horizons.

Private equity firms are well positioned to finance these assets due to their expertise in infrastructure investing, operational optimization, and complex project structuring.

Investors are already deploying capital into:

Data center development and operators

Natural gas infrastructure and generation assets

Grid modernization technologies

Advanced nuclear companies and small modular reactor developers

Battery storage and renewable energy platforms

These investments provide exposure to one of the most powerful structural trends shaping the global economy.

Conclusion: Energy Infrastructure Is the Backbone of the AI Economy

Artificial intelligence is reshaping the digital economy. But its expansion depends on a physical foundation of electricity generation, transmission networks, and computing infrastructure.

The next decade will require unprecedented investment in power generation and grid modernization.

Electricity demand growth driven by AI, data centers, and electrification is transforming the energy sector into one of the most important infrastructure investment opportunities of the decade.

Private equity investors that deploy capital into power infrastructure today are not simply financing energy assets.

They are financing the energy backbone of the AI economy.

Sources & References

Bloomberg. (2023). Generative AI to Become a $1.3 Trillion Market by 2032, Research Finds. https://www.bloomberg.com/company/press/generative-ai-to-become-a-1-3-trillion-market-by-2032-research-finds/

Energy Markets & Planning. Queued Up: Characteristics of Power Plants Seeking Transmission Interconnection. https://emp.lbl.gov/queues

FERC. (2024). Explainer on the Transmission Planning and Cost Allocation Final Rule. https://www.ferc.gov/explainer-transmission-planning-and-cost-allocation-final-rule

FERC. (2024). State of Markets Report. https://www.ferc.gov/sites/default/files/2025-03/25_State-of-the-Market_0320_1200.pdf

Goldman Sachs. (2024). AI, data centers and the coming US power demand surge. https://www.goldmansachs.com/pdfs/insights/pages/generational-growth-ai-data-centers-and-the-coming-us-power-surge/report.pdf

International Atomic Energy Agency. (2024). Energy, Electricity and Nuclear Power Estimates for the Period up to 2050. https://www-pub.iaea.org/MTCD/Publications/PDF/RDS-1-44_web.pdf

International Atomic Energy Agency. (2025). In Operation & Suspended Operation. https://pris.iaea.org/PRIS/WorldStatistics/OperationalReactorsByCountry.aspx

International Atomic Energy Agency. (2025). Nuclear Power Capacity Trend. https://pris.iaea.org/PRIS/WorldStatistics/WorldTrendNuclearPowerCapacity.aspx

International Atomic Energy Agency. (2024). Nuclear Power Reactors in the World. https://www-pub.iaea.org/MTCD/Publications/PDF/p15748-RDS-2-44_web.pdf

S&P Global. (2025). Private equity flows to advanced nuclear companies hit record high in 2024. https://www.spglobal.com/market-intelligence/en/news-insights/articles/2025/2/private-equity-flows-to-advanced-nuclear-companies-hit-record-high-in-2024-87302728

US Energy Information Administration. (2021). International Energy Outlook 2021. https://www.eia.gov/outlooks/ieo/tables_side_xls.php

US Energy Information Administration. (2025). Nuclear Energy Overview. https://www.eia.gov/totalenergy/data/monthly/pdf/sec8_3.pdf

US Energy Information Administration. (2026). U.S. natural gas production to reach record highs in 2026 and 2027. https://www.eia.gov/todayinenergy/detail.php?id=67166&

US Energy Information Administration. (2026). New U.S. electric generating capacity expected to reach a record high in 2026. https://www.eia.gov/todayinenergy/detail.php?id=67205

World Nuclear Association. (2025). Nuclear Power in the World Today. https://world-nuclear.org/information-library/current-and-future-generation/nuclear-power-in-the-world-today#key-statistics

IMF. (2024). Global GDP.

McKinsey. (2023). The Economic Potential of Generative AI. The Next productivity frontier. https://www.mckinsey.com/~/media/mckinsey/business%20functions/mckinsey%20digital/our%20insights/the%20economic%20potential%20of%20generative%20ai%20the%20next%20productivity%20frontier/the-economic-potential-of-generative-ai-the-next-productivity-frontier.pdf

Statista. (2024). Artificial Intelligence – Worldwide. https://www.statista.com/outlook/tmo/artificial-intelligence/worldwide

S&P Global Intelligence. (2023). 2024 Generative AI Outlook. https://sandpglobal-spglobal-live.cphostaccess.com/marketintelligence/en/news-insights/blog/infographic-the-big-picture-2024-generative-ai-outlook

S&P Global Intelligence. (2023). Private equity bets on AI gold rush with billions pumped into datacenters. https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/private-equity-bets-on-ai-gold-rush-with-billions-pumped-into-datacenters-79666528