- PE 150

- Posts

- Banks vs. Private Credit: Who’s Actually Winning?

Banks vs. Private Credit: Who’s Actually Winning?

Today we're diving into the financing tug-of-war between banks and private credit.

Good morning, ! Today we're diving into the financing tug-of-war between banks and private credit, the next phase of risk in private debt, Africa’s overlooked PE upside, and Carlyle’s big bet on wealth.

Juniper Square helps PE GPs deliver a modern investor experience without giving up operational control — combining purpose-built software and fund administration services in one connected model. As investor expectations rise and fund structures grow more complex, firms need fewer handoffs, fewer failure points, and a stronger system of record behind every LP interaction. Book a demo →

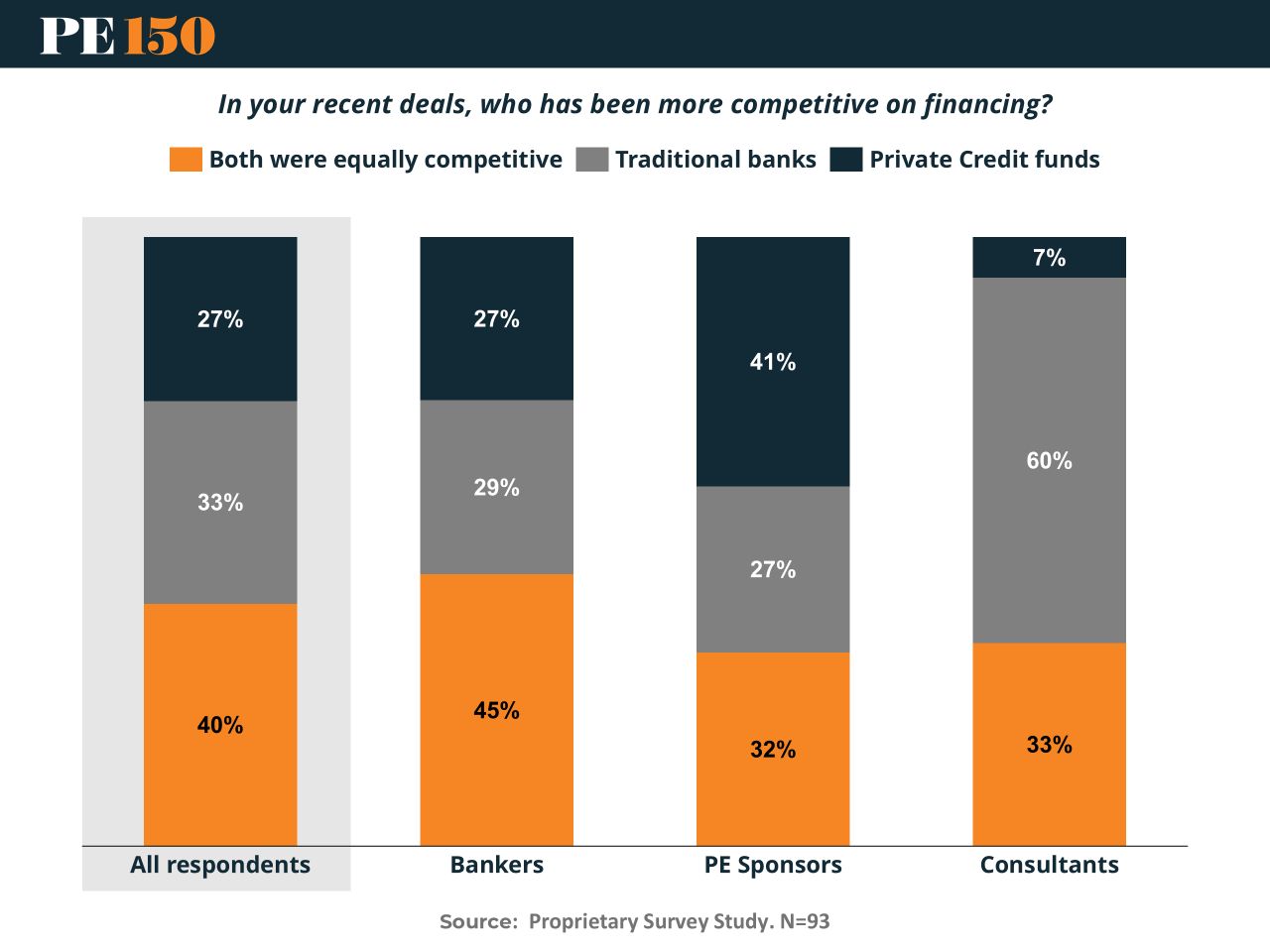

MICROSURVEY

Financing Tug-of-War

The private credit vs. banks debate is starting to look like a Rorschach test—everyone sees what they want.

The data: 40% call it a tie, 27% give the edge to private credit, and 33% still back banks.

Zoom in: PE sponsors are breaking ranks—41% favor private credit, citing speed, certainty, and flexibility. Bankers? Still confident, with 45% calling it even.

Plot twist: Consultants lean heavily toward banks (60%), likely anchored in larger, structured deals.

The bottom line: No knockout yet. But if execution is king, private credit is winning rounds—while banks still own the heavyweight division. (More)

PRIVATE CREDIT CORNER

Private Credit Risk: Faster Capital, Slower Stress

Private credit is entering a more demanding phase. Default rates are rising, not abruptly, but as a normalization after years of easy conditions. The key driver is not just higher rates, but the speed of capital deployment, especially into sectors facing AI-driven disruption.

The tension is clear: capital is moving fast into long-duration, uncertain outcomes, while borrowers face near-term refinancing pressure. This increases the likelihood of credit deterioration, often expressed through restructurings or payment-in-kind interest rather than immediate defaults.

This is not a classic banking risk. Private credit is funded by long-term institutional capital, limiting rapid liquidity contagion. Stress emerges gradually (but does not disappear), through earnings pressure and refinancing constraints. The more relevant systemic channel is banks. Their growing exposure, via credit lines and financing, creates a second-order risk. If liquidity is mismatched, stress in private credit can transmit to bank balance sheets.

Bottom line: risks are real and rising, but slow-moving and credit-driven, not sudden or systemic—unless amplified by weak bank liquidity discipline. (More)

PRESENTED BY JUNIPER SQUARE

Stop adding more tools or service providers. Get the best of both with a fund operations partner.

The LP experience can make or break fundraising because investors remember how it feels to work with your firm: onboarding, responsiveness, reporting, and the confidence they have in the numbers.

That experience is only as strong as the operating model behind it. When fund and investor data live across disconnected systems, delays and inconsistencies show up fast.

Juniper Square is the fund operations partner for PE GPs, combining software + fund administration services built on a common data foundation. That means fewer failure points, clearer visibility across investor workflows, and a modern investor experience powered by a single source of truth.

Book a demo to see how a fund operations partner

REGIONAL FOCUS

Africa’s PE Gap Is Still the Opportunity

Africa accounts for less than 1% of global private equity AUM despite representing a far larger share of global GDP. In contrast, other regions typically capture 5% to 7% of AUM relative to their economic weight.

The imbalance is not new but it is persistent. Limited local capital pools, smaller deal sizes, and exit constraints have kept global sponsors on the sidelines. At the same time, structural growth across consumer, infrastructure, and financial services continues to outpace developed markets. The result is a region where economic activity is expanding faster than capital formation.

For private equity, this is less about catching up and more about timing. Early entrants face friction around execution and liquidity, but they also avoid the multiple compression seen in saturated markets. As global capital searches for differentiation and growth, Africa remains one of the few regions where penetration is still low enough to matter.

Strategic takeaway: This is not an allocation story yet. It is a sourcing and conviction story for managers willing to build local edge before capital crowds in. (More)

DEAL OF THE WEEK

Carlyle Doubles Down on Wealth

Carlyle is leaning further into the wealth management arms race, agreeing to acquire a majority stake in MAI Capital Management at a $2.8bn+ valuation.

Why it matters: This isn’t a cold start. Carlyle already had exposure via Galway Holdings, making this a classic “know your asset, then scale it” play.

Zoom in: MAI brings $72.6bn in AUM/AUA and a focus on high-net-worth and family office clients—exactly where consolidation is heating up.

The angle: Carlyle is betting on integrated advisory platforms as the future, where scale + services = stickier clients.

The bottom line: Existing sponsors exit, Carlyle doubles down, and wealth management keeps looking less like a cottage industry—and more like private equity’s next roll-up frontier. (More)

See how PE GPs deliver a modern investor experience with a connected operating model. Book a demo →

"There is only one boss. The customer. And he can fire everybody in the company... simply by spending his money somewhere else"

Sam Walton