- PE 150

- Posts

- $38T Debt. 11.8x Multiples. €1B+ Exits Surge 28%. What’s Really Moving PE?

$38T Debt. 11.8x Multiples. €1B+ Exits Surge 28%. What’s Really Moving PE?

This week we're covering ESG’s shift from federal pause to state-level acceleration (with Scope 3 now in play)

Good morning, ! This week we're covering ESG’s shift from federal pause to state-level acceleration (with Scope 3 now in play), a tighter platform market where buyout multiples sit at 11.8x and only 20% of sponsors are paying up for scarcity, Europe’s exit rebound (+5% YoY, with €1B+ deals up 28%), America’s $38T debt load and ~6% deficit reality, and US investment into the UK falling from $55B (2021) to $33B (2025 YTD).

Want to advertise in PE 150? Check out our ad platform, here.

Know someone who would love this? Pass it along—they’ll thank you later! Here’s the link.

DATA DIVE

Platform Entry Is Getting Sharper, Not Smaller

Stat: 28% of sponsors are maintaining similar platform entry sizes but becoming more selective, while only 20% are willing to pay up for scarcity assets.

Context: Despite buyout multiples returning to 11.8x in 2025, platform investing has not retreated. It has tightened. The market is splitting. 36% of firms now prefer platforms below $100 million EV, while 25% target assets above $500 million. The traditional $100 to $250 million band attracts just 16% of respondents, suggesting a squeeze in the middle. Smaller platforms offer multiple arbitrage and operational runway. Larger platforms provide institutional stability and cleaner exit narratives. What has changed is not appetite, but conviction thresholds. Entry sizes remain intact for many funds, yet underwriting screens are stricter and pricing tolerance narrower.

Strategic Takeaway: Deal platforms still anchor strategy, but entry discipline now defines outcomes. Sponsors competing in crowded mid market lanes without sourcing edge or sector clarity risk overpaying for mediocrity. In this cycle, platform quality at entry matters more than leverage at exit.

TREND TO WATCH

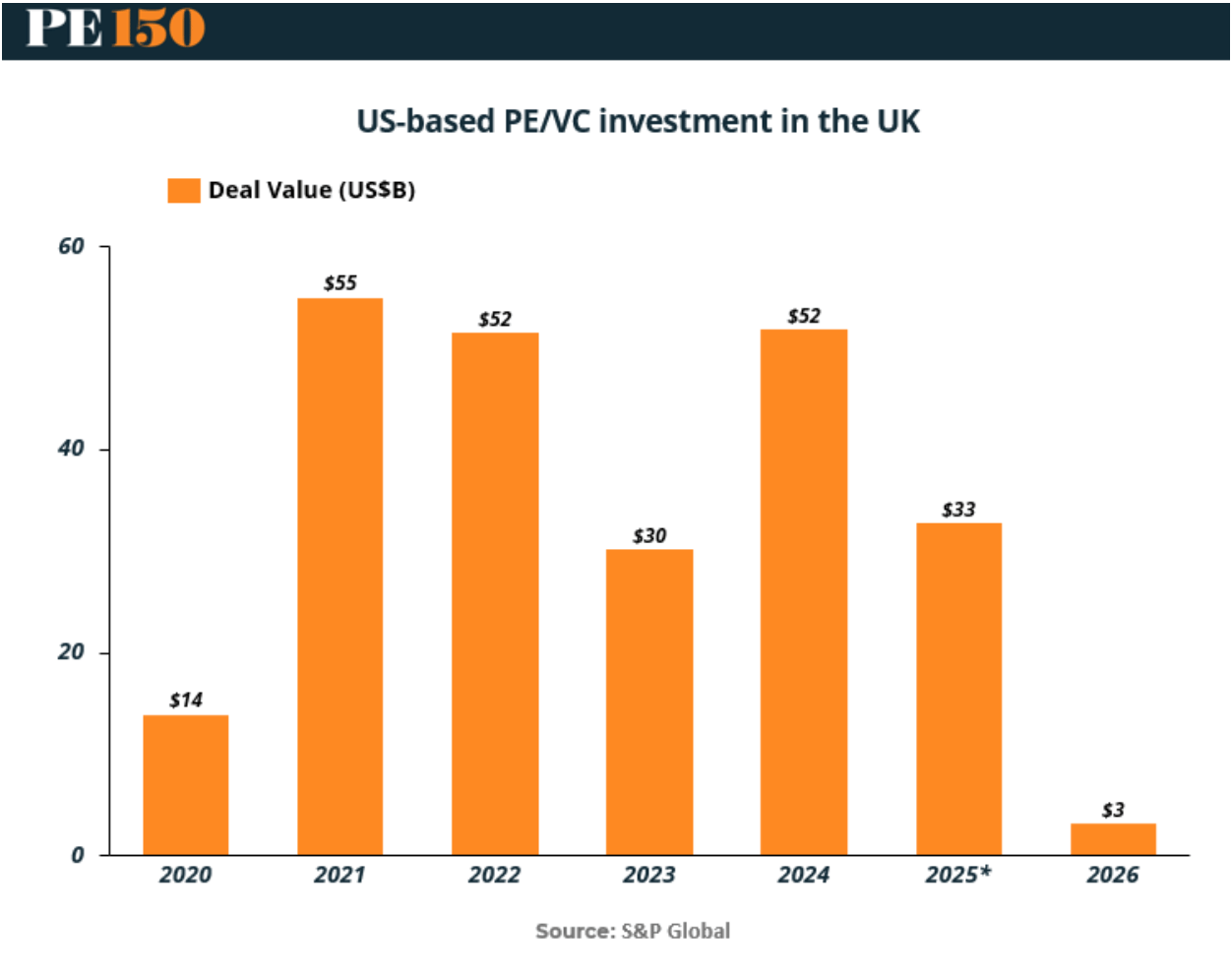

UK Deal Flow: The American Pullback

US private equity and venture capital investment into the UK is losing altitude.

After peaking at $55B in 2021, deal value slipped to $52B in 2022, fell sharply to $30B in 2023, briefly rebounded to $52B in 2024, and now sits at $33B in 2025 YTD, with just $3B recorded so far in 2026.

The volatility tells a bigger story than the absolute numbers. 2021 was a liquidity-fueled anomaly. The 2023 drop reflected global rate shock and exit paralysis. The 2024 rebound suggested renewed conviction. But the renewed softness in 2025 and early 2026 points to something structural, not cyclical.

US sponsors are becoming more selective about cross-border platform formation. Currency dynamics, slower UK growth, regulatory complexity, and thinner exit pathways versus the US are forcing higher conviction thresholds. Capital is not fleeing Europe, but it is demanding sharper theses and cleaner scale narratives.

For UK founders and management teams, the bar just moved higher. For US GPs, transatlantic deals now require true sourcing edge, not just global ambition. (More)

LIQUIDITY CORNER

Europe’s Exit Window Is Open. Selectively.

European exit activity rose 5 percent in 2025, marking a second straight year of improvement. The freeze is thawing, but liquidity remains highly concentrated. The rebound was driven by mega exits. €1 billion plus deals jumped 28 percent to 96 transactions, supported by a partial IPO reopening and standout listings like Verisure at €13.7 billion. Firms ready to sell are moving. CVC, for example, led the pack with 17 exits.

Yet the backlog persists. The average holding period in Europe now sits at 5.3 years, with several large managers well above six. That reflects lingering valuation overhang from peak 2021 entry prices. The 2021 vintage underscores the tension. Only 23% of deals have exited by year four, below the typical 26 to 27 percent historical range.

The takeaway: liquidity has returned for scaled, high quality assets with strong earnings visibility. For everything else, price discipline and patience still rule. (More)

MACROECONOMICS CORNER

From Emergency Tool to Operating Model

America no longer borrows for emergencies. It borrows as a lifestyle.

Indexed to 1966, Public Debt is up more than 11,000%. GDP? Roughly 3,800%. The gap is now 200%+ — and widening. The chart doesn’t show a spike. It shows a drift.

Post-2020 deficits were supposed to normalize. They didn’t. We’re still running ~6% of GDP deficits in a full-employment economy. That’s not stimulus. That’s structure.

For years, low rates masked the math. Now Treasury Yields sit materially higher, and Interest Expense is compounding on a $38T base. When borrowing costs exceed nominal growth, debt ratios rise mechanically.

The U.S. still enjoys Dollar Privilege. But privilege cannot be permanent with weak fundamentals. (More)

COMPLIANCE CORNER

ESG’s Federal Pause, State-Level Sprint

The SEC hit pause. The states hit accelerate.

With the SEC’s 2025 ESG rule withdrawal, federal disclosure mandates are effectively frozen. But don’t mistake silence in Washington for relief. California’s SB 253 and SB 261 now require expansive GHG emissions reporting, including phased Scope 3 data. New York and Colorado are circling with similar playbooks.

For private equity, this isn’t theoretical. Portfolio companies must comply, which means funds inherit the data burden—ready or not.

Meanwhile, LPs are sharpening pencils on workforce practices, diversity metrics, and supply-chain human rights. Add rising alignment with TCFD and ISSB, and ESG diligence is no longer optional footnote territory.

Bottom line: Strengthen Scopes 1 and 2 tracking, prepare for Scope 3, formalize social policies, and hardwire ESG cooperation into acquisition agreements. Federal uncertainty doesn’t equal regulatory risk reduction. It just shifts the map. (More)

"You'll never do a whole lot unless you're brave enough to try."

Dolly Parton