- PE 150

- Posts

- Why Private Credit Keeps Winning (Plus Brazil PE & AUM Insights)

Why Private Credit Keeps Winning (Plus Brazil PE & AUM Insights)

Performance holds, capital flows persist — and emerging market data adds context.

Good morning, ! This week we cover private credit evergreen AUM by category, the number of private equity firms in Brazil, and the operational implications for GPs as bank retrenchment continues to create tailwinds for private credit.

Juniper Square shares how Avanath Capital Management modernized operations as fund complexity increased — replacing fragmented processes with a more connected operating model across fund accounting, reporting, and investor servicing. See how one GP reduced friction, improved visibility, and strengthened the investor experience with infrastructure built to scale. Read the Avanath story →

PRIVATE CREDIT

Evergreen Capital Goes Mainstream

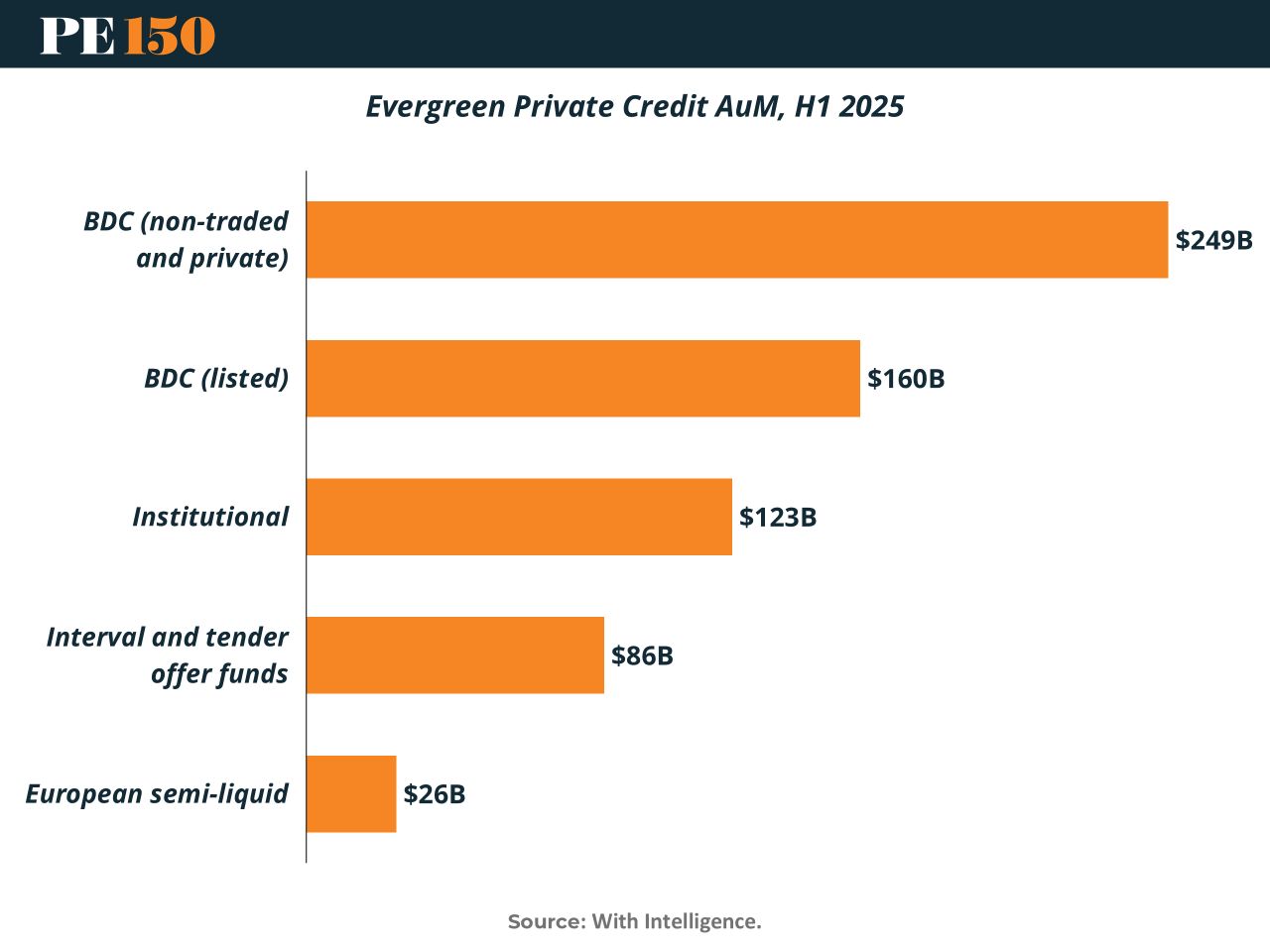

Evergreen private credit is no longer a niche—it’s becoming the default setting. As of H1 2025, the market hit $644B in AuM, driven by continuous fundraising and fewer vintage-year headaches.

BDCs still run the table, controlling 60%+ of assets, with non-traded BDCs ($249B) leading the charge. Chalk it up to regulatory clarity and retail-friendly access—yield-hungry investors aren’t complaining.

But the real shift is structural. Institutional capital ($123B) is embracing open-ended exposure, while interval and tender offer funds ($86B) are threading the liquidity needle.

The takeaway: distribution is destiny. Private credit is moving beyond institutions into wealth channels and retail wrappers.

Bottom line: Evergreen capital offers stickier AuM for managers and consistent income for investors—but liquidity remains more promise than guarantee. (More)

PRESENTED BY JUNIPER SQUARE

New fund formats call for a new operating model: fund operations partner.

Our report on the rise of new fund formats shows a clear shift: operating cadence is increasing, investor workflows are getting more complex, and expectations are moving toward to “always-on.”

That’s why leading PE firms are shifting to a fund operations partner model: one system of record + embedded expertise to run fundraising, investor operations, reporting, and administration with consistent data.

Juniper Square combines purpose-built software + expert fund administration services into a single connected operating model, delivering clearer visibility, fewer failure points, and a modern investor experience.

Read the full breakdown in the report.

Supporting our sponsors supports our free newsletters. Please support our sponsors!

REGIONAL FOCUS

Brazil’s PE Market Grows Up

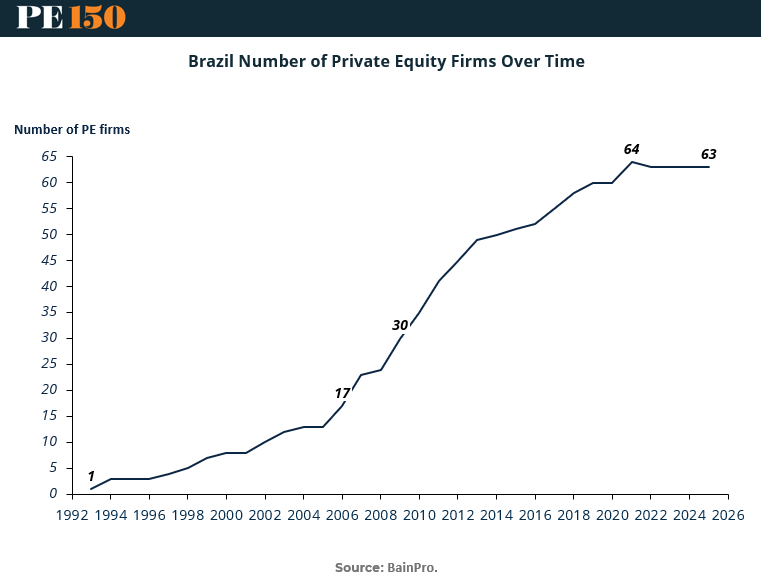

Brazil’s private equity ecosystem has expanded from 1 firm in the early 1990s to 63 today, with the most aggressive buildout occurring between 2006 and 2013. The market nearly tripled during that stretch, jumping from 17 firms to nearly 50, before settling into a slower growth phase over the past decade.

That plateau around 63 to 64 firms is the signal. Brazil is no longer in discovery mode. It has reached a level of sponsor density that begins to resemble more mature markets, where competition, not access, defines outcomes.

For GPs, this shifts the edge away from simply being early. Winning now requires differentiated sourcing, sector specialization, and operational capability on the ground. For LPs, the implication is just as important. Brazil is no longer a broad macro allocation. Manager selection risk has increased, dispersion will widen, and backing local expertise over global generalists will likely drive returns. (More)

MICROSURVEY

What percentage of your portfolio would you be comfortable rolling into GP led continuation vehicles? |

DEAL OF THE WEEK

Goldman Reloads the Mezz Machine

Goldman Sachs Asset Management is back in the market, eyeing $13B for GS Mezzanine Partners IX—its latest play in subordinated debt.

The pitch is familiar: lend to PE-backed companies across North America and Europe, sit between senior debt and equity, and target 11%–13% leveraged returns.

Why now? Credit dislocation. Turbulence—particularly in software amid AI disruption—is creating entry points across the $1.8T private credit market.

This isn’t Goldman’s first rodeo. The firm has been running mezz since 1996, and this marks fund number nine.

Bottom line: When volatility rises, mezzanine capital tends to follow—and Goldman is betting this cycle has legs. (More)

PRESENTED BY 9FIN

The best PE investors know the debt. 9fin helps you know it faster.

Get AI-powered intelligence on leveraged loans, high yield bonds, private credit, and distressed debt, all in one platform.

From deal financials to covenant analysis to real-time news, 9fin gives PE professionals the edge when it matters most. Start your free 30-day trial now.

Fund Ops Corner

How Bank Retrenchment Creates Tailwinds for Private Credit

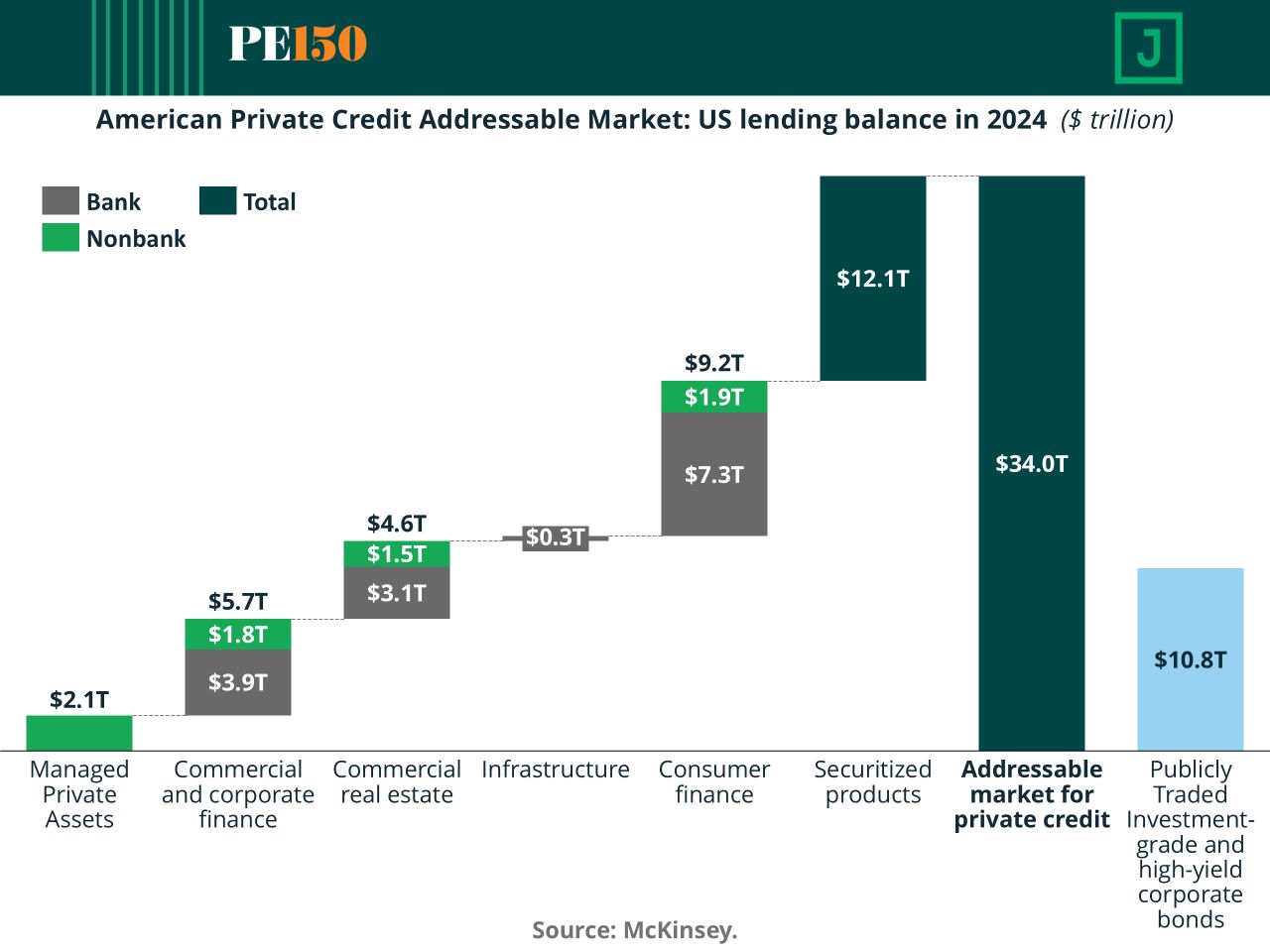

Bank retrenchment is no longer cyclical—it is structural. As regulatory capital constraints reduce banks’ appetite for middle-market and specialized lending, private credit has stepped in as a primary financing channel. What was once opportunistic is now systemic. With ~$34T of U.S. lending outstanding and only a fraction currently intermediated by nonbanks, the runway for private credit expansion remains substantial.

The implication is clear: even incremental share gains across commercial finance, real estate, and consumer lending translate into trillions of additional deployable opportunity. This is not just growth—it is a reallocation of credit intermediation.

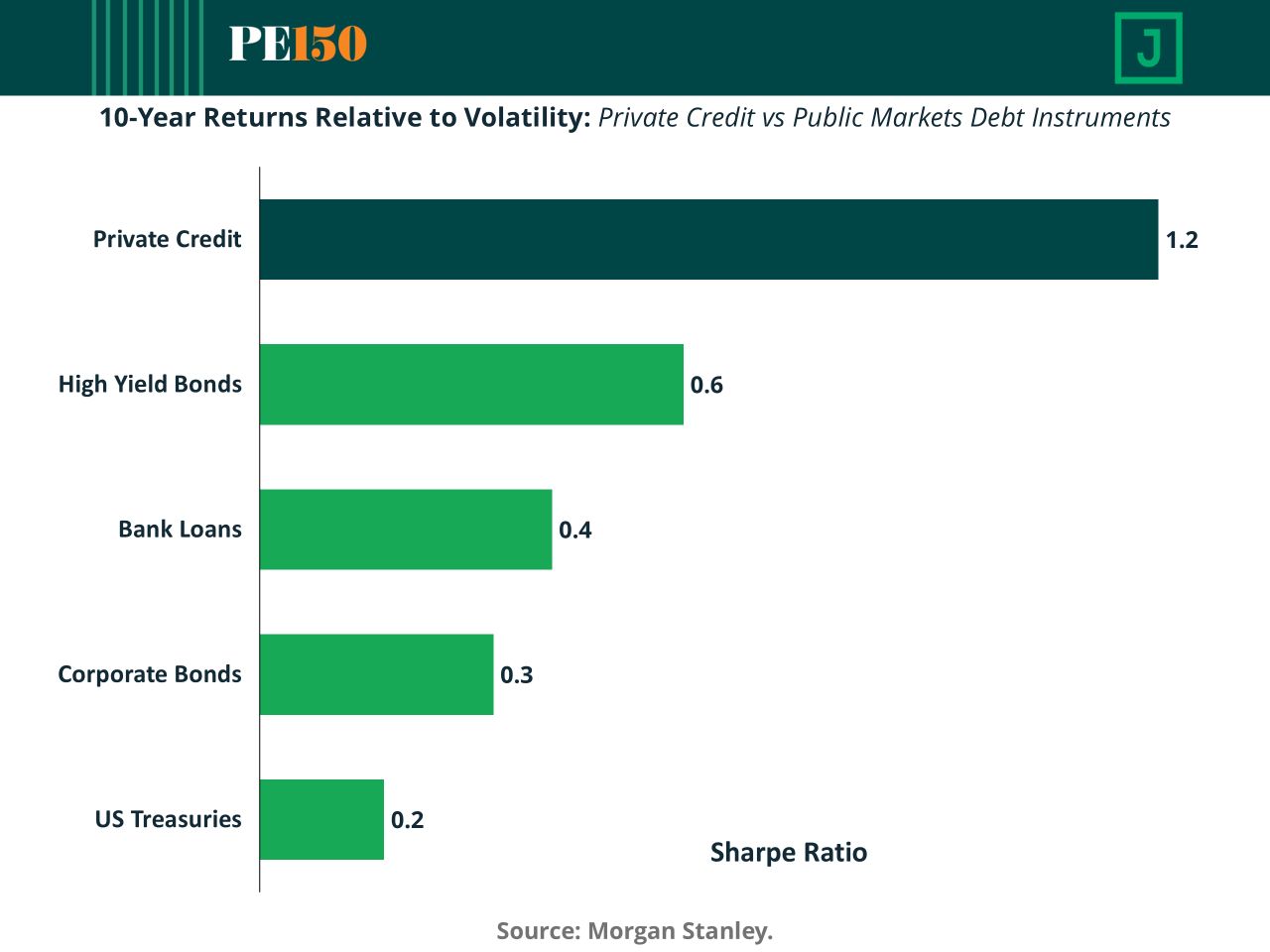

At the same time, performance data reinforces allocator demand. Private credit’s ~1.2 Sharpe ratio materially exceeds public debt alternatives, supported by floating-rate structures, covenant protection, and seniority in the capital stack.

Operational Impact for GPs

This shift requires a fundamental upgrade in GP operating models:

Credit Platform Buildout: Origination, underwriting, and portfolio monitoring must scale with bank-like rigor. Sector specialization and data-driven credit analytics are now core capabilities.

Continuous Risk Management: Covenant tracking, scenario modeling, and early warning systems move from back-office to front-line functions.

Liquidity Engineering: Active management of credit facilities, subscription lines, and maturity ladders becomes critical, particularly as platforms adopt evergreen and semi-liquid structures.

Workout Readiness: Restructuring expertise is no longer episodic—it is embedded infrastructure.

In short, private credit GPs are evolving into integrated credit institutions. Sustained performance will increasingly depend less on asset selection alone and more on institutional-grade operations, governance, and balance sheet discipline.

Read the Avanath story to see how one GP modernized operations for a more complex fund structure. Read the story →

Supporting our sponsors supports our free newsletters. Please support our sponsors!

“The four most dangerous words in investing are: ‘This time it’s different.’”

Sir John Templeton