- PE 150

- Posts

- The New Operating Model for GPs (Evergreen Is Forcing It)

The New Operating Model for GPs (Evergreen Is Forcing It)

Today we're covering GPs operational implications of the rise of Evergreen vehicles.

Good morning, ! Today we're covering GPs operational implications of the rise of Evergreen vehicles, European buyout Funds strongly outperform public markets, while US funds perform similar to the S&P500.

Juniper Square helps PE GPs deliver a modern investor experience without giving up operational control — combining purpose-built software and fund administration services in one connected model. As investor expectations rise and fund structures grow more complex, firms need fewer handoffs, fewer failure points, and a stronger system of record behind every LP interaction. Book a demo →

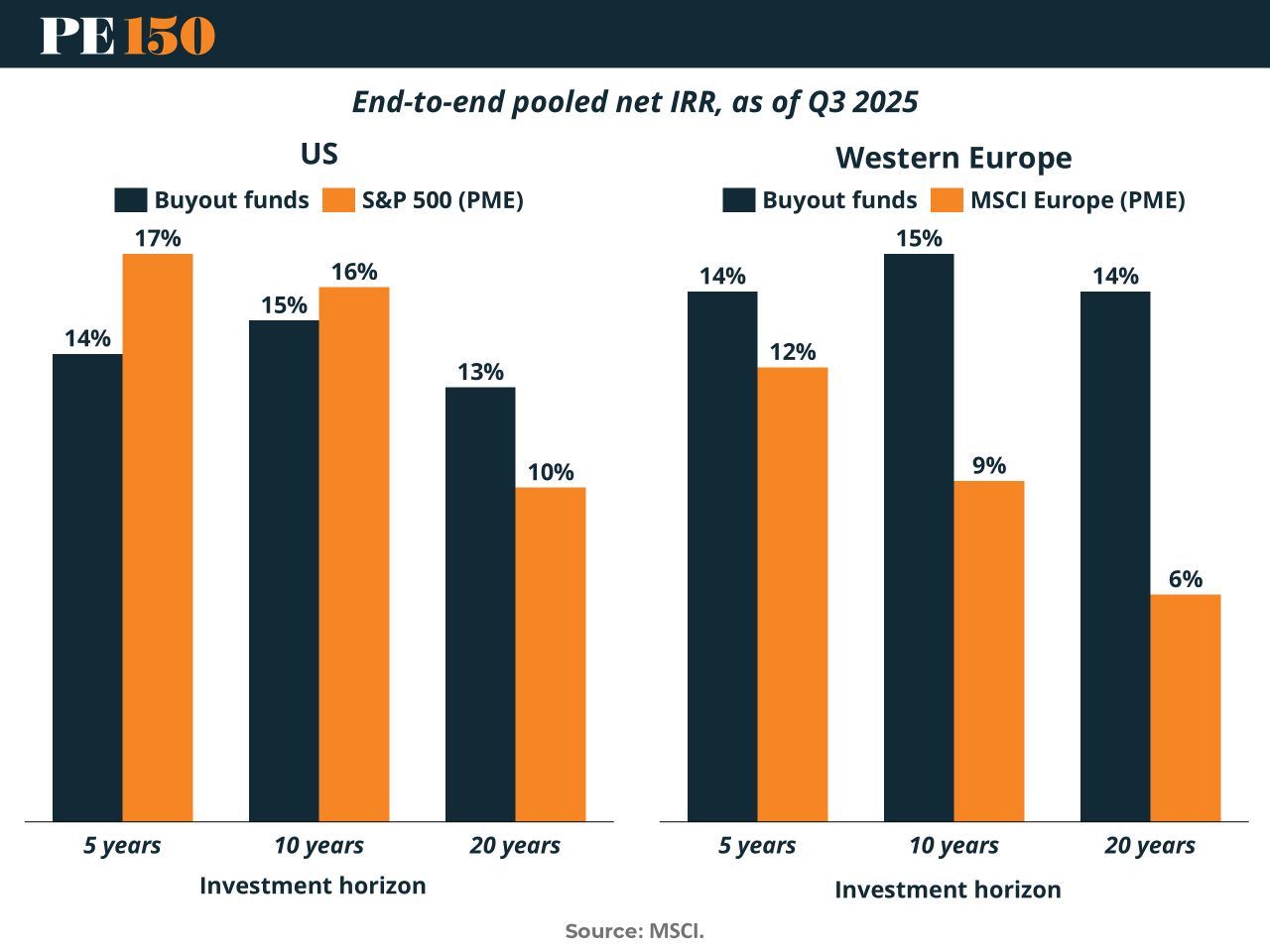

REGIONAL FOCUS

Europe Still Has the Edge

For all the noise around private equity underperformance, geography matters. A lot.

In the U.S., buyout funds are trailing public markets across most time horizons—~14% vs. ~17% over five years, with similar gaps at 10 years. Only at 20 years does PE barely pull ahead.

Cross the Atlantic, and it’s a different asset class. In Western Europe, PE consistently outperforms public benchmarks, with spreads as wide as 600bps over 20 years.

What’s driving it? A less efficient market, more room for operational alpha, and less reliance on multiple expansion.

The bottom line: This isn’t a cyclical blip—it’s a regional divergence. And for LPs, the question is getting louder: why chase U.S. beta when European alpha is still on offer? (More)

PRIVATE CREDIT CORNER

Banks Smell Blood in Private Credit

Private credit’s decade-long run may be hitting its first real speed bump—and Wall Street banks are quietly stretching. After ceding ground post-2023, banks are reclaiming share in leveraged buyouts, with volumes rebounding from 39% to >50%.

What changed? A mix of easing regulation, lower rates, and cracks in private credit’s foundation—namely rising defaults, liquidity pressure, and the hangover from aggressive underwriting.

The catch: this isn’t a knockout punch. Direct lenders still win on speed, certainty, and flexibility, especially in choppy markets.

The bottom line: This is less a comeback story and more a reopening of competition. For banks to fully reassert dominance, they’ll need tighter spreads, more deal flow, and a macro tailwind that—so far—remains theoretical. (More)

PRESENTED BY JUNIPER SQUARE

Stop adding more tools or service providers. Get the best of both with a fund operations partner.

The LP experience can make or break fundraising because investors remember how it feels to work with your firm: onboarding, responsiveness, reporting, and the confidence they have in the numbers.

That experience is only as strong as the operating model behind it. When fund and investor data live across disconnected systems, delays and inconsistencies show up fast.

Juniper Square is the fund operations partner for PE GPs, combining software + fund administration services built on a common data foundation. That means fewer failure points, clearer visibility across investor workflows, and a modern investor experience powered by a single source of truth.

Book a demo to see how a fund operations partner

MICROSURVEY

In your recent deals, who has been more competitive on financing? |

DEAL OF THE WEEK

KKR Buys a Franchise Flywheel

KKR’s acquisition of Nothing Bundt Cakes at a reported $2 billion valuation is less about cake and more about cash flow quality. The 700 unit franchise system is approaching $1 billion in systemwide sales, with average unit volumes around $1.4 million, and has nearly doubled its footprint since Roark Capital acquired it in 2021.

This is a rare exit for Roark, a firm known for long duration holds, which makes the timing notable. Growth has been driven by a franchised model that shifts capex to operators while preserving high margin royalty streams. In a market where exits remain selective, scaled franchise platforms continue to clear at premium valuations.

For KKR, the bet is straightforward. Predictable unit economics plus continued white space expansion equals compounding cash flows without heavy reinvestment needs.

Why it matters: In an environment shaped by liquidity pressure and delayed exits, assets that combine growth with capital efficiency are becoming the most reliable path to realizations. Franchise models are not just resilient, they are increasingly exit ready. (More)

Fund Ops Corner

Evergreen Scale Meets Liquidity Engineering

The shift to evergreen structures is no longer incremental—it’s a structural redesign of private markets. US evergreen AUM has nearly doubled (2022–2025), while interval and tender-offer funds surpassed $225B, reflecting strong demand for semi-liquid access.

Critically, structure drives outcomes. Higher capital deployment (~90%) versus drawdown (~29%) materially boosts returns via reduced cash drag and continuous reinvestment, enhancing geometric compounding. This is echoed in performance dispersion across evergreen categories, where secondaries and private debt lead.

In parallel, continuation funds have become core tools amid a constrained exit cycle. With exits still ~50% below 2021 peaks and holding periods extending (6–7+ years), GPs are using continuation vehicles to reset duration, provide LP liquidity, and retain high-conviction assets. Demand is structural, with liquidity needs outpacing supply (~5.5x).

Operational Implications for GPs

Build continuous capital deployment engines (treasury + pacing discipline)

Upgrade liquidity management for periodic redemptions (forecasting, buffers)

Enhance valuation governance for evergreen NAV integrity

Develop secondary/continuation playbooks (pricing, conflicts, LP options)

Align data & reporting cadence with semi-liquid expectations (monthly/quarterly NAV)

Invest in transfer agency & investor servicing capabilities

Bottom line: operations must evolve from episodic fund cycles to always-on capital platforms.

See how PE GPs deliver a modern investor experience with a connected operating model. Book a demo →

"Innovation distinguishes between a leader and a follower"

Steve Jobs