- PE 150

- Posts

- Latin America Private Capital Fundraising Report

Latin America Private Capital Fundraising Report

From PE Dominance to Multi-Strategy Maturity: Capital Concentration, Manager Expansion, and the Rise of Real Assets (2006–1H 2025)

I. Introduction

Over the past two decades, Latin America’s private capital ecosystem has undergone a profound transformation. What began as a market largely defined by traditional private equity has evolved into a diversified, multi-strategy platform spanning infrastructure, private credit, venture capital, and real assets. Fundraising cycles have mirrored global liquidity conditions, regional macro volatility, and shifting investor risk appetite — but beneath those cycles lies a deeper structural story.

This report analyzes private capital fundraising across Latin America from 2006 through 1H 2025, examining not only total capital formation, but also how that capital has been allocated across strategies, manager experience levels, and fund vintages. It further explores the expansion of the manager base, the concentration of capital among experienced GPs, and the accelerating momentum in real assets strategies.

Taken together, the data reveals a market that is simultaneously maturing and consolidating. While participation has broadened and new strategies have institutionalized, capital allocation has become increasingly selective. Latin America is no longer a single-strategy private equity story — it is a multi-layered ecosystem shaped by diversification, discipline, and generational transition.

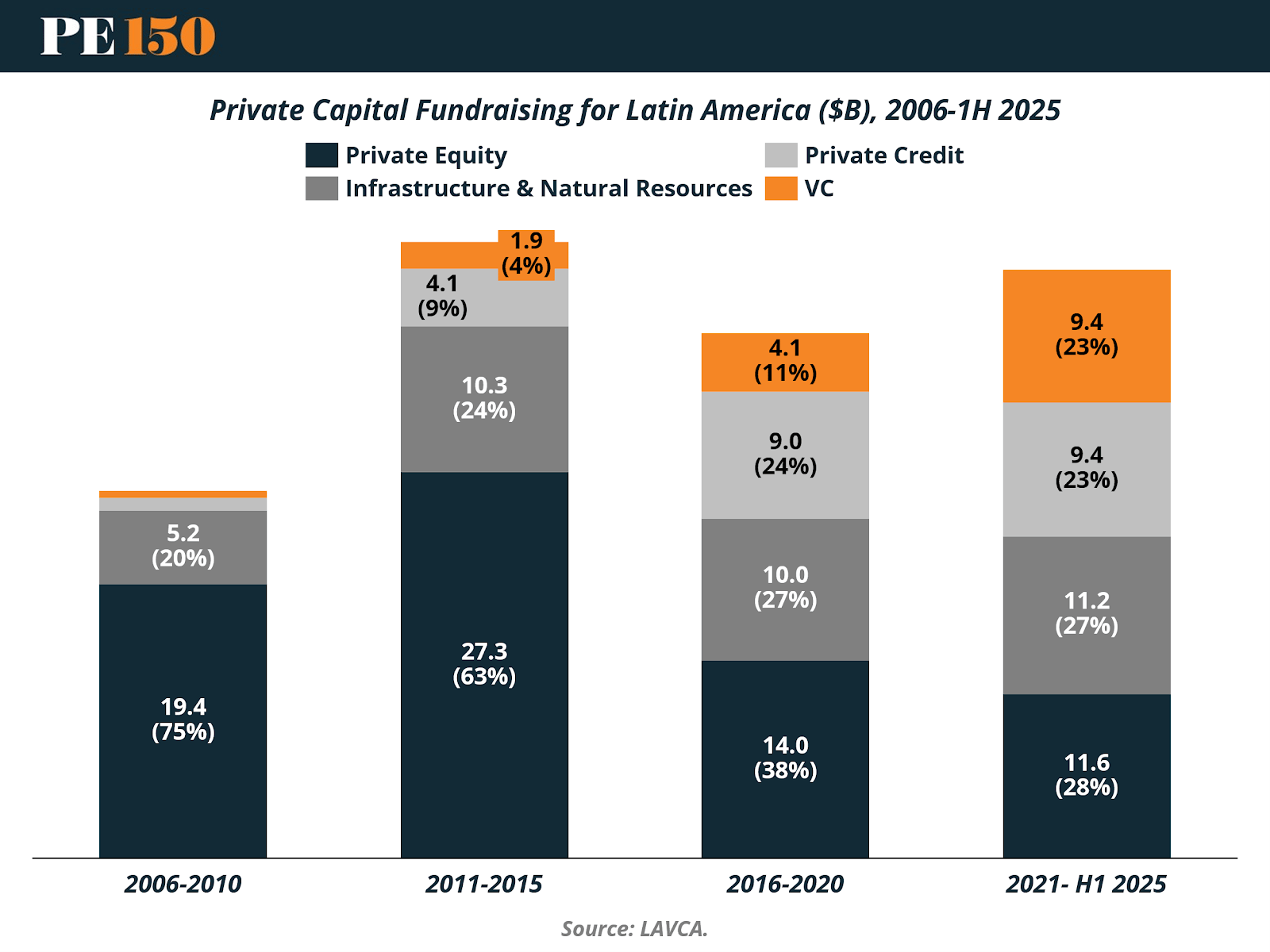

II. Fundraising Evolution by Strategy: A Structural Rebalancing of Private Capital in Latam

Beyond headline fundraising totals, the most important story in Latin America’s private capital market is the structural shift in composition over the past two decades. While overall volumes have fluctuated with global liquidity cycles, the regional ecosystem has evolved from a PE-dominated market into a far more diversified private capital landscape.

In the 2006–2010 period, total fundraising reached $25.8 billion, with traditional private equity (75%) accounting for $19.4 billion of capital raised. Infrastructure & Natural Resources (20%) represented the only meaningful alternative strategy at the time, while Private Credit and Venture Capital were still nascent and largely underdeveloped. At that stage, Latin America’s private markets were overwhelmingly synonymous with buyouts and growth equity.

The 2011–2015 cycle marked both a peak and a turning point. Total fundraising climbed to $43.5 billion, the highest level in the dataset. Although PE remained dominant at 63%, its relative share began to decline as other strategies scaled. Infrastructure & Natural Resources expanded to 24%, and both Private Credit and VC started attracting institutional capital in a more systematic way. The asset mix was still PE-heavy, but early signs of diversification were clearly emerging.

Following the commodity downturn and macro volatility of the mid-2010s, the 2016–2020 period saw fundraising moderate to $37.1 billion, but the capital structure meaningfully rebalanced. PE’s share fell sharply to 38%, while Infrastructure & Natural Resources held steady at 27%. Private Credit rose to 24%, reflecting growing demand for non-bank financing solutions, and VC expanded to 11%, supported by the rapid expansion of the region’s tech ecosystem.

The most recent period, 2021–1H 2025, reinforces this structural transformation. Total fundraising reached $41.6 billion, approaching prior cycle highs, but with a fundamentally different composition. PE now represents just 28% of total capital raised. Infrastructure & Natural Resources accounts for 27%, while both Private Credit and Venture Capital each capture 23%. For the first time, fundraising is evenly distributed across four major strategies rather than concentrated in one.

The implication is clear: Latin America’s private capital market has matured into a multi-strategy ecosystem. What began as a PE-centric fundraising environment has evolved into a balanced capital formation platform, signaling deeper institutionalization, greater strategy sophistication, and a market increasingly aligned with global private markets trends.

III. Manager Selection: Capital Concentration Among Experienced GPs

If the previous section highlighted strategy diversification, the manager data tells a different — and equally important — story: capital is concentrating in the hands of experienced fund managers.

Between 2020 and 1H 2025, fundraising in Latin America has increasingly favored Established GPs (Vintage VI+), reflecting a more risk-sensitive LP base and a flight to track record amid macro volatility.

In 2020, experienced managers accounted for 61% of capital raised, while Emerging managers (Vintage II–III) captured 23% and First-Time funds represented 15%. At that stage, capital allocation was relatively balanced, with meaningful room for new platforms to scale.

By 2021, experienced managers still led with 51%, but emerging managers saw a temporary spike to 37%, likely reflecting fundraising momentum from prior strong vintages and residual liquidity in global markets. However, that window proved short-lived.

From 2022 onward, the shift becomes decisive. Experienced GPs captured 62% in 2022, rising sharply to 74% in 2023, 80% in 2024, and reaching 88% in 1H 2025. In parallel, emerging managers saw their share fall to single digits in recent periods, while first-time funds declined to just 4% of capital raised in 1H 2025.

The message is clear: in a higher-rate, more selective fundraising environment, LPs are prioritizing track record, scale, and execution certainty. Re-ups with known managers are dominating allocations, while new entrants face increasingly high barriers to institutional capital.

This dynamic reinforces a broader theme across Latin America’s private markets. While the ecosystem has diversified by strategy, it has simultaneously consolidated by manager experience. The result is a market that is structurally more sophisticated — but also more competitive — where differentiation, performance history, and institutional credibility are critical to raising capital.

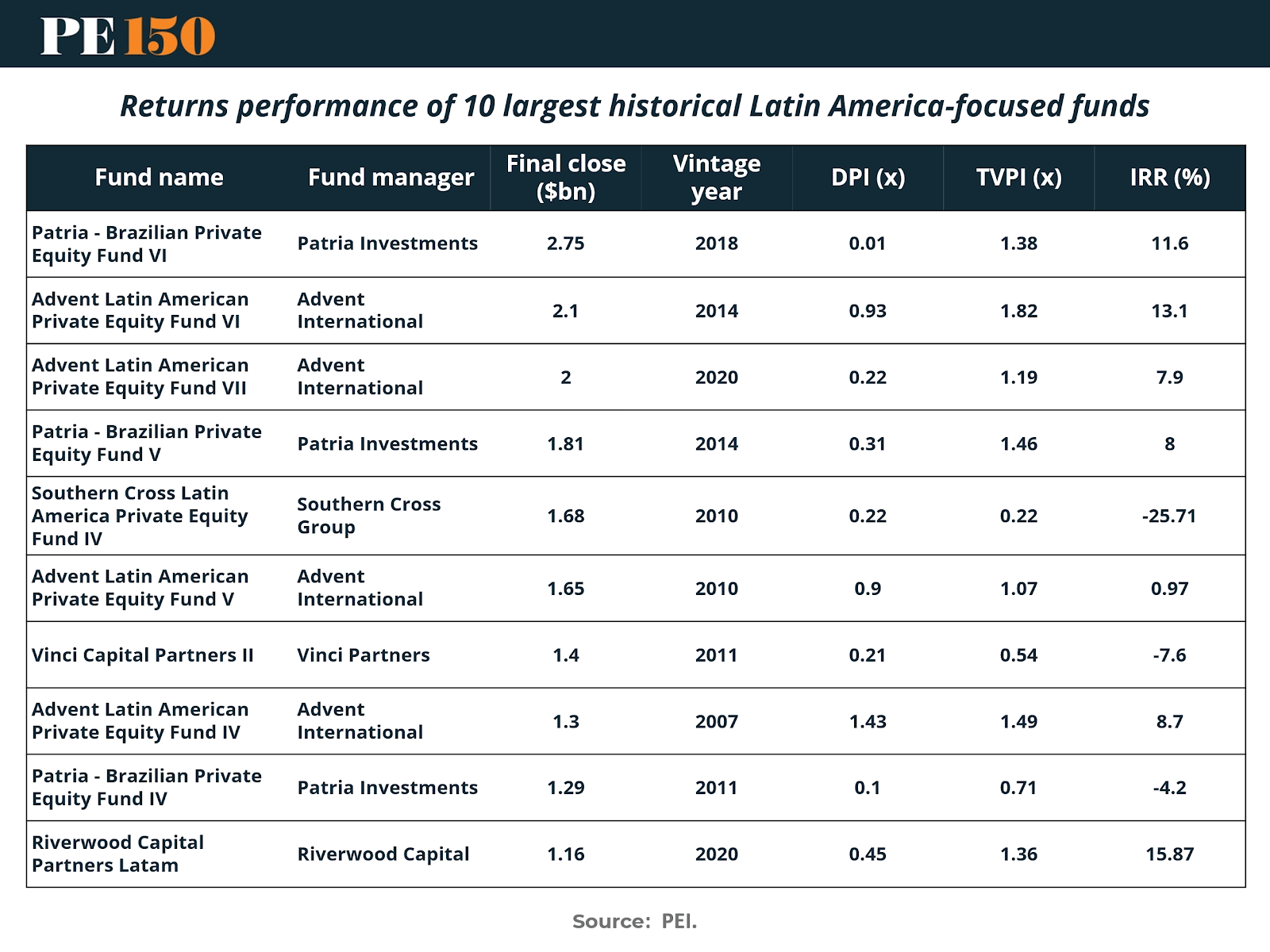

IV. Performance Dispersion Among the Largest Latin America Funds

While recent fundraising trends point to capital concentration among experienced managers, performance data across the region’s largest funds reveals why selectivity has intensified. Even among scaled, institutional platforms, outcomes vary meaningfully across vintages, strategies, and market cycles.

The ten largest Latin America-focused private equity funds for which performance data is available illustrate substantial dispersion in realized and unrealized returns. IRRs range from deeply negative outcomes to mid-teens performance, while total value multiples (TVPI) span from significant capital impairment to strong value creation. DPI ratios remain low for more recent vintages, reflecting the early stage of realization rather than necessarily weak underlying performance.

Several structural observations emerge from the data:

Dispersion Remains Material — Even at Scale

Performance variation is not limited to smaller or emerging managers. Among the largest, most established platforms in the region, IRRs range from negative double digits to approximately 16%, while TVPI multiples range from 0.22x to 1.82x. This underscores a defining characteristic of Latin America’s private capital market: scale does not eliminate performance variability.

Vintage Timing Is Critical

Funds raised in the 2010–2014 cycle generally show stronger DPI and more mature TVPI profiles, reflecting exposure to a more favorable entry environment and longer realization windows. By contrast, 2018 and 2020 vintages display lower DPI ratios — largely a function of lifecycle positioning — but also reveal more mixed early multiple development.

Realization Cycles Drive Perception

DPI remains limited in several recent large funds, reinforcing the importance of time horizon when evaluating headline returns. In emerging markets especially, longer realization timelines can materially affect interim performance metrics. As such, IRR dispersion partly reflects differences in exit timing rather than purely operational underperformance.

Strategy and Sector Exposure Matter

Underlying exposure — whether to Brazil-centric buyouts, pan-regional growth equity, or sector-specialized platforms — contributes to differentiated outcomes. Macroeconomic volatility, currency cycles, and regulatory shifts amplify the importance of sector positioning and execution discipline in Latin America relative to more stable developed markets.

Taken together, the data reinforces a central theme of this report: as Latin America’s private capital ecosystem has diversified by strategy, it has also become more discriminating by performance. In a market characterized by structural macro volatility and heterogeneous outcomes, LPs are increasingly rewarding managers with demonstrated execution capability across cycles.

Importantly, the dispersion observed among the largest funds suggests that track record depth, platform stability, and vintage management are not merely signaling mechanisms — they are risk mitigation tools. In a multi-strategy environment with widening performance dispersion, manager selection becomes as critical as strategy allocation itself.

This performance variability helps explain the fundraising dynamics observed in Section III. Capital concentration among experienced GPs is not simply a function of brand preference; it reflects a rational response to measurable return dispersion across the region’s largest vehicles.

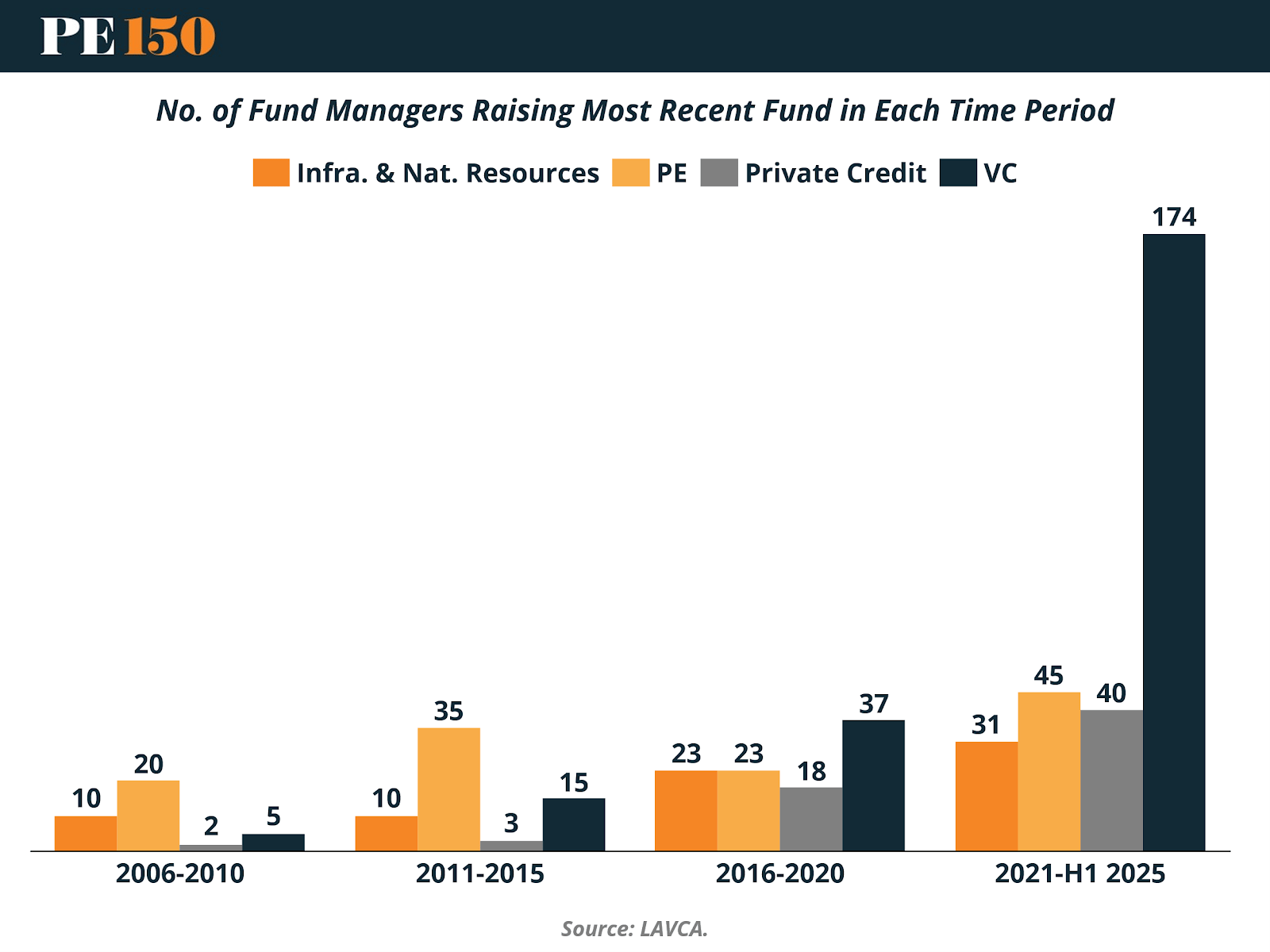

V. Manager Proliferation: The Expansion of the Fundraising Base

While capital composition and manager experience tell one side of the story, the evolution in the number of fund managers raising capital reveals another important structural shift: the steady broadening of Latin America’s private markets platform — particularly in venture capital.

In the 2006–2010 period, fundraising activity was relatively concentrated. Only 20 PE managers raised their most recent fund during the cycle, alongside 10 Infrastructure & Natural Resources managers, 2 Private Credit managers, and just 5 VC managers. The ecosystem was still small, with limited strategy breadth and a narrow manager base.

The 2011–2015 cycle saw moderate expansion. PE managers increased to 35, Infrastructure remained stable at 10, Private Credit edged up to 3, and VC rose to 15 managers. Although PE continued to dominate in manager count, early signs of platform diversification were visible.

The real acceleration occurred in 2016–2020. The number of PE managers raising capital reached 23, Infrastructure & Natural Resources climbed to 23, Private Credit expanded significantly to 18, and VC increased to 37 managers. This period marked the first time the manager base meaningfully broadened across multiple strategies rather than being centered primarily around buyout firms.

The most striking development comes in 2021–1H 2025. Infrastructure managers increased to 31, PE managers to 45, and Private Credit to 40. However, the standout figure is Venture Capital, with 174 managers raising funds during the period — an exponential expansion compared to prior cycles.

This sharp increase in VC managers reflects the region’s startup boom, the institutionalization of early-stage capital, and lower barriers to entry relative to traditional buyout or infrastructure strategies. At the same time, when viewed alongside the previous section, it underscores a paradox: while the number of managers has expanded, particularly in VC, capital has become more concentrated among experienced firms.

In other words, Latin America’s private capital ecosystem is simultaneously broadening in participation and tightening in capital allocation. More managers are entering the market, but LP capital is increasingly selective — favoring scale, track record, and established platforms. This dual dynamic defines the current fundraising environment across the region.

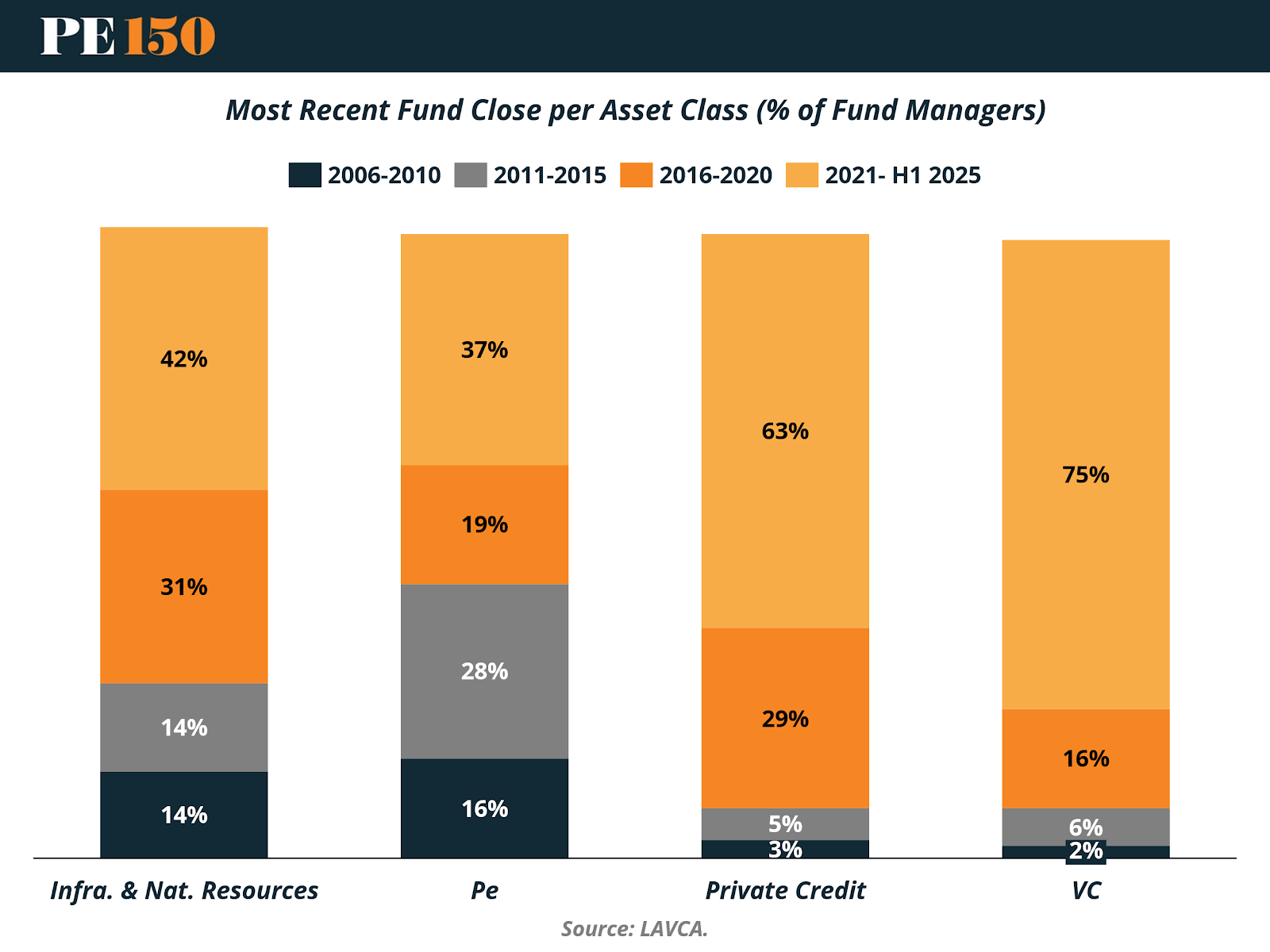

VI. Fundraising Momentum: Recency of Capital Formation by Asset Class

If prior sections highlighted diversification and capital concentration, the timing of most recent fund closes adds another important dimension: which asset classes are driving the current fundraising cycle.

The data clearly shows that Venture Capital is the most recent-cycle-driven strategy in the region. Fully 75% of VC managers (n=231) closed their most recent fund in the 2021–1H 2025 period. This is a striking acceleration compared to prior cycles and reflects the startup boom, increased global LP appetite for LatAm tech exposure, and the rapid institutionalization of the VC ecosystem.

Private Credit shows a similarly recent profile. 63% of Private Credit managers (n=63) closed their latest vehicle in the current cycle, with another 29% raised in 2016–2020. This confirms that private credit is not just growing in capital share — it is structurally a post-2016 phenomenon in Latin America, with most platforms still relatively young in vintage terms.

Infrastructure & Natural Resources presents a more balanced distribution. While 42% of managers (n=74) closed their most recent fund in 2021–1H 2025, a significant portion also raised capital in prior cycles. This suggests a more established and cyclically resilient manager base, rather than a recent surge of new entrants.

Private Equity stands somewhere in between. Among PE managers (n=123), 37% closed in 2021–1H 2025, with meaningful activity in 2011–2015 (28%) and 2016–2020 (19%). Unlike VC, PE fundraising appears more evenly distributed across cycles, reflecting its longer-standing institutional footprint in the region.

Taken together, the timing data reinforces two core themes. First, VC and Private Credit are the most cycle-sensitive and recently accelerated strategies. Second, Infrastructure and PE display deeper historical continuity, with fundraising activity spanning multiple vintages.

In other words, the evolution of Latin America’s private capital market is not just about diversification — it is also about generational turnover. Some strategies are in expansion mode, while others reflect a more mature, multi-cycle institutional base.

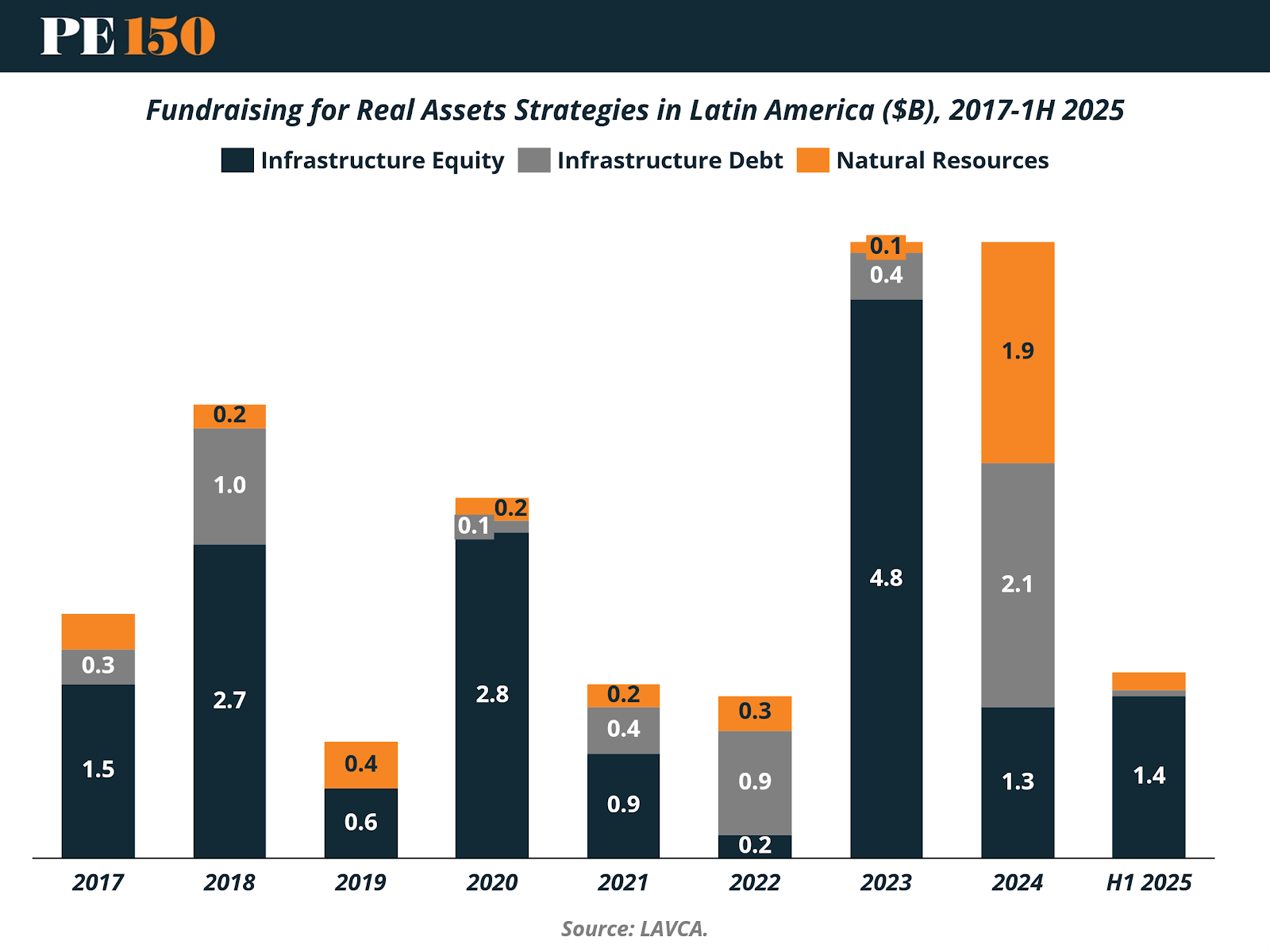

VII. Real Assets Fundraising: Infrastructure Resilience and the Rebound in Debt

Zooming into Real Assets strategies provides a more granular view of how capital has behaved within Infrastructure and Natural Resources since 2017. The data shows a market characterized by volatility, but also by structural resilience — particularly within infrastructure equity.

Between 2017 and 2018, fundraising expanded from $2.1bn to $3.9bn, driven primarily by Infrastructure Equity, which accounted for the majority of capital in both years. Infrastructure Debt and Natural Resources remained smaller contributors, though both were active components of the mix. The sharp pullback in 2019 — when total fundraising dropped to $1.0bn — reflected broader regional macro uncertainty and slower deployment cycles.

The 2020 rebound to $3.0bn highlighted infrastructure’s defensive characteristics, even amid global disruption. However, 2021 and 2022 saw another moderation phase, with totals of $1.4bn in each year, and a greater relative contribution from Infrastructure Debt, signaling growing investor appetite for yield-oriented, lower-volatility exposure.

The standout year is 2023, when real assets fundraising surged to $5.4bn, the highest level in the series. Notably, this spike was overwhelmingly driven by Infrastructure Equity ($4.8bn), suggesting renewed confidence in long-term hard asset strategies, potentially linked to energy transition, digital infrastructure, and essential services themes across the region.

In 2024, total capital remained elevated at $5.3bn, but the composition shifted meaningfully. Infrastructure Debt rose sharply to $2.1bn, while Infrastructure Equity moderated to $1.3bn. This rotation indicates a more cautious positioning by LPs in a higher-rate environment, favoring structured and downside-protected strategies over pure equity exposure.

In 1H 2025, fundraising stands at $1.6bn, largely driven by Infrastructure Equity, though the full-year trajectory will determine whether the market sustains its post-2023 momentum.

Overall, the real assets data reinforces two structural themes: first, Infrastructure Equity remains the backbone of the strategy in Latin America, demonstrating strong rebound capacity; and second, Infrastructure Debt is gaining institutional relevance, particularly in periods of macro uncertainty and elevated interest rates. Natural Resources, while present, appears more episodic and opportunity-driven rather than consistently dominant.

VIII. Landmark Fund Closes: Scale, Specialization, and Regional Depth (2024–1H 2025)

The most recent cycle confirms that real assets fundraising in Latin America is being driven by fewer, larger, and increasingly specialized vehicles, with Brazil firmly at the center of activity.

The largest close of the period was Patria Infrastructure Fund V, raising $2.36bn in March 2025. The size of the vehicle alone underscores both the depth of Brazil’s institutional market and LP appetite for scaled infrastructure platforms with established track records. Similarly, BTG Pactual Brazil Timberland Fund II reached $1.24bn in April 2024, highlighting growing investor interest in forestry and timberland strategies — a segment that blends real assets exposure with sustainability and climate-aligned themes.

Infrastructure debt also featured prominently. CAF-AM Ashmore Colombia Infrastructure Debt Fund II raised $440m, while CIFI Sustainable Infrastructure Debt Fund closed at $300m, and Mexico-based BEEL2CK 24 secured $310m. These raises reinforce the earlier trend: credit-oriented real assets strategies are institutionalizing, particularly in a higher-rate environment where downside protection and structured yields are attractive to LPs.

Geographically, Brazil continues to dominate the largest tickets — including Vinci Climate Change Infrastructure ($389m), BTG Pactual Infrastructure III ($326m), and Kinea Equity Infra I ($232m) — but there is meaningful regional diversification. Colombia, Mexico, the Andean region, Paraguay, and pan-regional Latin American vehicles all appear in the dataset. Funds such as Ashmore Andean Fund III ($420m) and Exagon XIC Latin America Fund I ($120m) demonstrate continued appetite for multi-country exposure.

Notably, sustainability-linked and climate-oriented mandates are increasingly visible across the strategy set — from climate infrastructure to sustainable debt and forestry impact funds — signaling that energy transition and ESG integration are no longer niche allocations but embedded themes within real assets fundraising.

Taken together, the 2024–1H 2025 closes illustrate a market that is both scaling and specializing. Large, established Brazilian managers are anchoring the top end of fundraising, while debt, forestry, and climate-focused strategies are expanding the real assets opportunity set across the broader region.

IX. Conclusion

The evolution of private capital fundraising in Latin America tells a story of structural maturation rather than cyclical fluctuation alone. Over time, the region has shifted from a PE-centric landscape to a balanced multi-strategy market in which infrastructure, private credit, and venture capital each play meaningful roles in capital formation.

At the same time, the fundraising environment has become more selective. While the number of managers — particularly in venture capital — has expanded significantly, capital is increasingly concentrated among experienced platforms with proven track records. This dual dynamic of broader participation and tighter capital allocation defines the current market structure.

Real assets further illustrate this shift. Infrastructure equity remains a core pillar, infrastructure debt is gaining institutional depth, and sustainability-linked mandates are now embedded across strategies rather than treated as niche themes. Large, scaled vehicles — particularly in Brazil — are anchoring the upper end of fundraising, signaling both LP confidence and market consolidation.

Ultimately, Latin America’s private capital market today is more diversified, more institutionalized, and more competitive than at any point in its history. The next phase will likely be shaped not by expansion alone, but by performance dispersion, strategic specialization, and disciplined capital deployment in an increasingly selective global environment.

Sources and References:

LAVCA, “Latin American Private Capital Industry Trends – October 2025”

PEI Group, “How Private Equity Could Reshape Latin America”

Premium Perks

Since you are an Executive Subscriber, you get access to all the full length reports our research team makes every week. Interested in learning all the hard data behind the article? If so, this report is just for you.

|