- PE 150

- Posts

- Global Interest Rate Divergence and the Repricing of Sovereign Risk

Global Interest Rate Divergence and the Repricing of Sovereign Risk

Gaston Brizuela Bosio

April 06, 2026 • Estimated Reading Time: 3 minutes

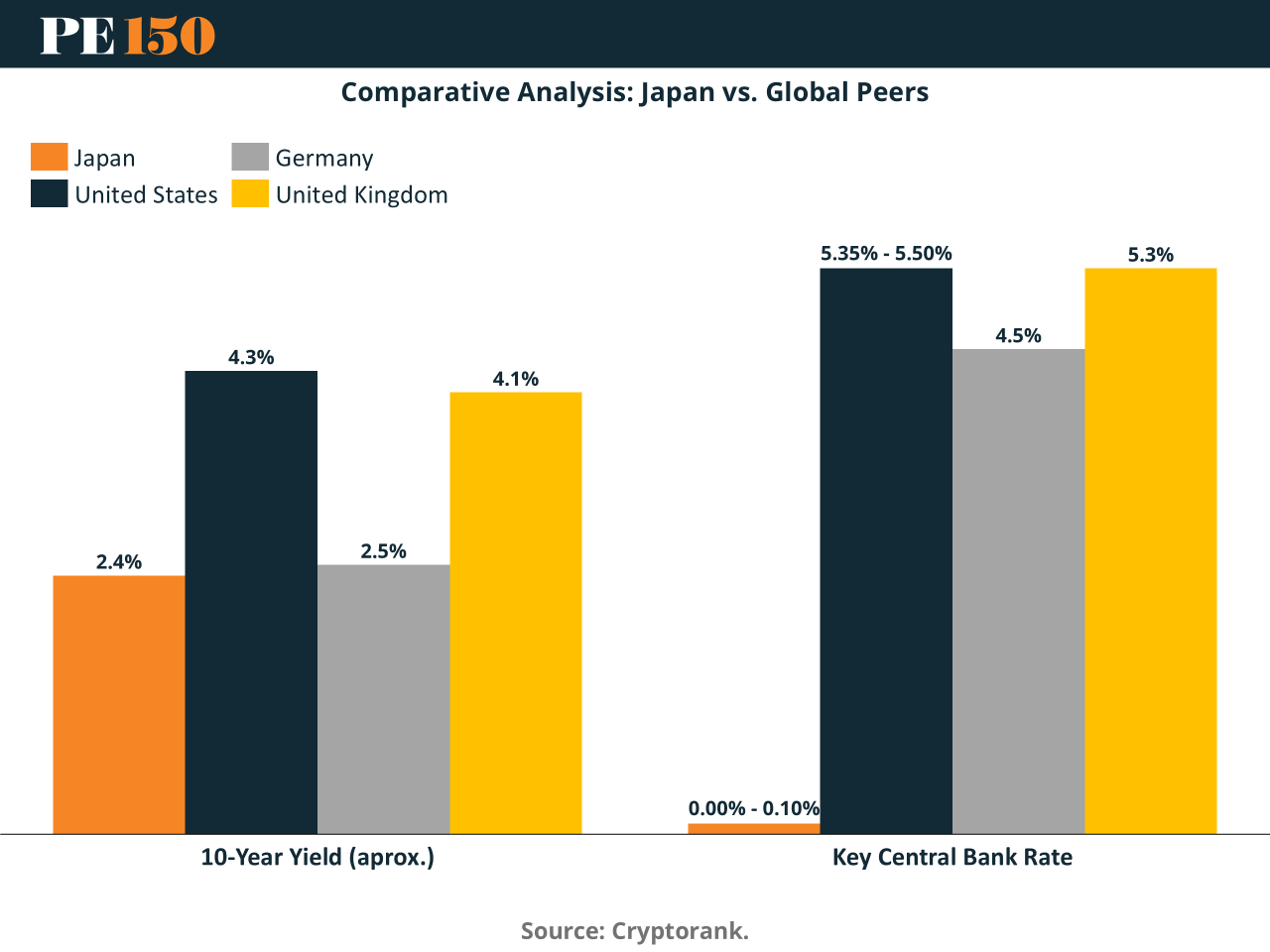

The global economic landscape is entering a period of meaningful transition, characterized by diverging interest rate paths, shifting inflation dynamics, and a reassessment of sovereign bond markets. The comparative data in the chart highlights a striking imbalance between Japan and its major developed peers, particularly in long-term yields and central bank policy rates. These differences are not merely statistical—they reflect fundamentally different stages of the monetary policy cycle and carry significant implications for capital flows, currency valuation, and global financial stability.

Japan’s position stands out most clearly. With a 10-year government bond yield at approximately 2.4%, the country has reached levels not seen in decades. This marks a structural break from its long-standing ultra-low rate environment. For years, Japan maintained near-zero yields through aggressive monetary easing, including yield curve control. The recent rise signals a gradual normalization process, driven by persistent inflation pressures and a reassessment of domestic economic conditions. However, despite this increase in long-term yields, Japan’s policy rate remains anchored near zero, indicating that the normalization process is still incomplete and cautious.

In contrast, the United States presents a fully restrictive monetary stance. With a 10-year yield around 4.3% and a central bank policy rate exceeding 5%, the U.S. reflects an economy where inflation remains a primary concern and monetary authorities are committed to maintaining tight financial conditions. This divergence between short-term policy rates and long-term yields also suggests that markets anticipate eventual easing, but not imminently. The persistence of elevated yields underscores the resilience of economic activity and the stickiness of inflation, particularly in services.

Europe offers a slightly different dynamic. Germany, often considered the benchmark for eurozone sovereign debt, shows a 10-year yield near 2.5%, closely aligned with Japan’s recent levels. However, its central bank rate is significantly higher, around 4.5%. This indicates a more advanced tightening cycle, where policy has already moved decisively into restrictive territory. The United Kingdom follows a similar pattern, with a 10-year yield above 4% and a policy rate above 5%, reflecting both inflation concerns and structural pressures in its domestic economy, including housing and labor market constraints.

The juxtaposition of these economies reveals a key insight: the global interest rate environment is no longer synchronized. Instead, it is fragmented, with each major economy responding to its own inflation trajectory, fiscal conditions, and structural constraints. This fragmentation has profound implications for global capital allocation.

One of the most immediate consequences is the shifting direction of capital flows. For years, low yields in Japan encouraged investors to seek higher returns abroad, particularly in U.S. and European assets. As Japanese yields rise, even modestly, this dynamic begins to reverse. Domestic assets become more attractive, potentially prompting repatriation of capital. This shift can exert upward pressure on global yields, particularly in markets that have benefited from sustained foreign demand.

Currency markets are equally sensitive to these changes. Interest rate differentials have long been a primary driver of exchange rates. A narrowing gap between Japanese and U.S. yields, for example, could support a stronger yen, altering trade competitiveness and affecting global supply chains. Similarly, persistent rate differentials in favor of the U.S. dollar may continue to attract capital inflows, reinforcing its strength despite growing fiscal concerns.

Another critical dimension is the role of inflation expectations. Across all major economies, inflation remains the central variable shaping monetary policy. Recent data releases, including consumer price indices and broader inflation measures, have shown mixed signals. While headline inflation may be moderating in some regions, core inflation—particularly in services—remains elevated. This creates a policy dilemma: easing too soon risks reigniting inflation, while maintaining restrictive conditions for too long could dampen growth.

Central banks are navigating this uncertainty with a data-dependent approach. Policy decisions are increasingly contingent on incoming economic indicators, including labor market conditions, wage growth, and consumer spending. This has introduced a higher degree of volatility into financial markets, as expectations shift rapidly in response to new data.

Bond markets, in particular, are undergoing a repricing of risk. The era of ultra-low yields is ending, and investors are demanding higher compensation for holding long-term debt. This reflects not only inflation risks but also concerns about fiscal sustainability, especially in economies with high debt levels. Rising yields increase borrowing costs for governments, which in turn can constrain fiscal policy and amplify economic slowdowns.

In this context, Japan’s transition is especially significant. As one of the largest holders of global financial assets, any shift in its domestic yield environment has outsized effects. Even incremental changes in Japanese yields can influence global liquidity conditions, reinforcing the interconnected nature of modern financial markets.