- PE 150

- Posts

- Continuation Vehicles: Private Equity’s New Exit Architecture

Continuation Vehicles: Private Equity’s New Exit Architecture

Private equity has entered an era where traditional exits can no longer be taken for granted.

Private equity has entered an era where traditional exits can no longer be taken for granted. Higher interest rates, selective buyers, inconsistent IPO markets, and longer hold periods have forced sponsors to rethink how value is realized. In that environment, continuation vehicles have moved from niche secondary market structures to one of the most important innovations in modern private capital.

Originally designed as a flexible solution for holding top performing assets beyond a fund’s life, continuation vehicles now serve a broader purpose. They provide liquidity to existing investors, allow GPs to retain ownership of prized companies, and create new entry points for secondary buyers seeking concentrated exposure to mature assets. What was once considered a workaround is increasingly becoming a standard feature of portfolio management.

Yet rapid growth has brought sharper scrutiny. Investors are asking harder questions around valuation fairness, fee structures, conflicts of interest, and portfolio concentration. As continuation vehicles become more common, the debate is no longer whether they belong in private equity. It is whether managers can execute them with enough discipline, transparency, and alignment to justify their growing role.

This report examines that shift through five key data points, highlighting where adoption is accelerating, where LP boundaries remain firm, and what continuation vehicles may mean for the future of private equity exits.

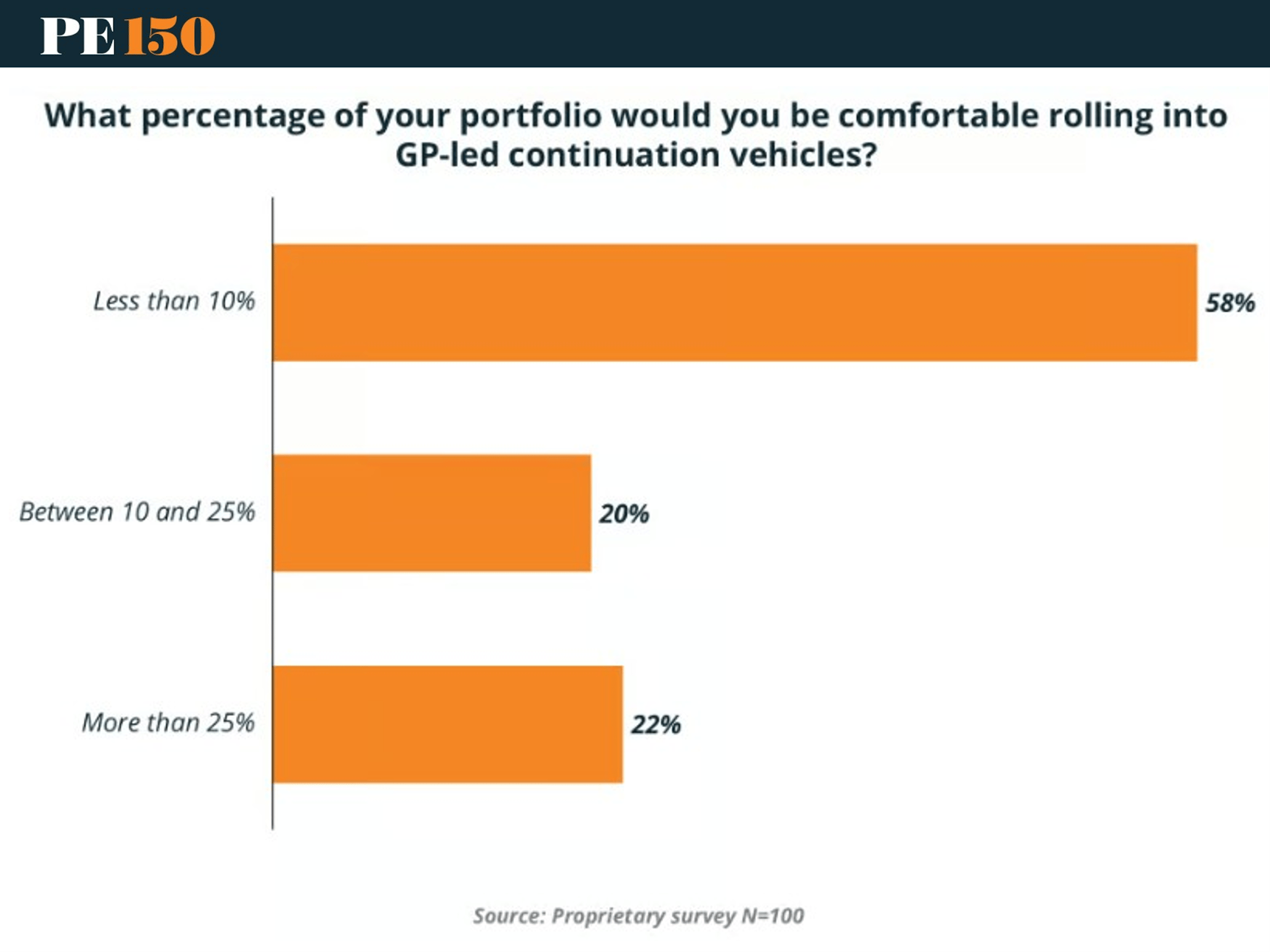

Capped, Not Closed: LP Appetite for Continuation Vehicles Has Clear Limits

Continuation vehicles have moved from niche liquidity solution to mainstream portfolio management tool, but this chart makes one point unmistakably clear: investor support remains conditional. While the market has grown rapidly in recent years, most LPs are still unwilling to allocate large portions of their portfolio to GP led structures. Adoption is increasing, but concentration risk remains a central concern.

The survey shows that 58% of respondents would only feel comfortable rolling less than 10% of their portfolio into GP led continuation vehicles. That is the dominant response by a wide margin. Meanwhile, only 20% would accept allocations between 10% and 25%, and 22% would support exposure above 25%. In practical terms, most investors appear open to the strategy, but only within tightly controlled portfolio limits.

This signals a maturing but still trust sensitive market. LPs increasingly recognize the utility of continuation vehicles for retaining high quality assets and generating liquidity, yet they are still drawing boundaries around scale. For GPs, the next phase of market growth will likely depend less on awareness and more on proving alignment, valuation discipline, governance strength, and repeatable performance outcomes.

Detailed Analysis

The majority favors limited exposure

With 58% selecting less than 10%, the prevailing LP mindset is diversification first, concentration second.Continuation vehicles are accepted, but not yet core allocations

Investors appear comfortable treating them as tactical sleeves rather than strategic portfolio anchors.Only a minority support aggressive exposure

Just 22% would allocate more than 25%, suggesting conviction exists but is far from universal.Governance remains critical

LP hesitation often centers around conflicts of interest, pricing fairness, and process transparency.Track record matters more than marketing

Managers with successful prior continuation deals are likely to win larger future allocations.Portfolio construction discipline is shaping demand

Many LPs already have exposure through primary funds, co investments, and secondaries, limiting appetite for another concentrated private markets sleeve.Large managers may benefit most

Established sponsors with scale, data, and institutional credibility are better positioned to overcome LP allocation caps.Future growth likely comes gradually

If continuation vehicles continue to deliver returns and cleaner liquidity outcomes, the under 10% comfort threshold may rise over time.Implication for GPs

Sponsors should underwrite fundraising expectations realistically and position vehicles as selective solutions rather than permanent capital substitutes.

Bottom line

The market is open for business, but LPs still want guardrails.

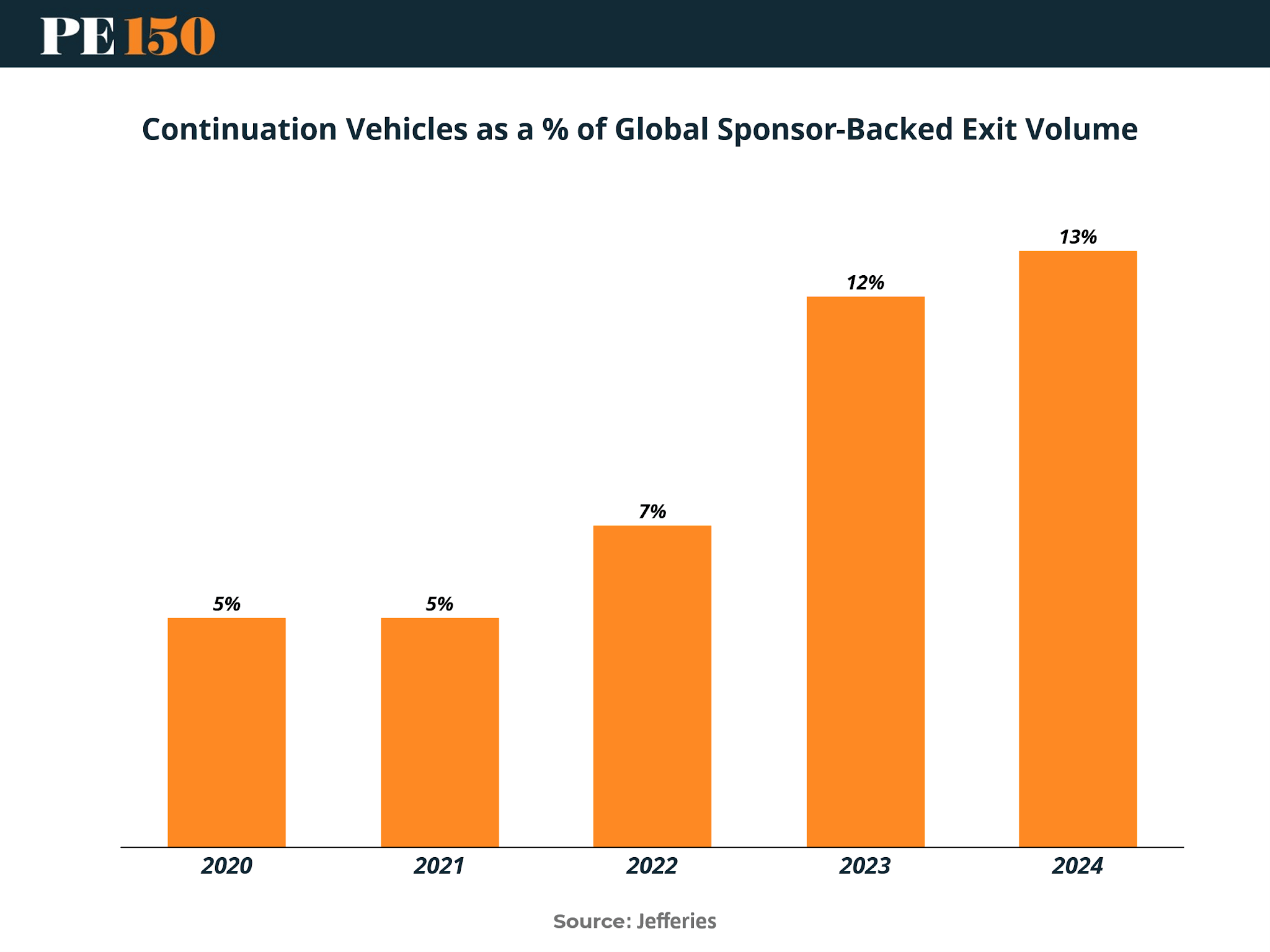

From Niche Tool to Exit Mainstay: Continuation Vehicles Are Reshaping Private Equity Liquidity

This chart captures one of the most important structural shifts in private equity exits over the last five years. Continuation vehicles were once viewed as opportunistic solutions used selectively during difficult market conditions. Today, they are becoming an increasingly normalized component of sponsor exit strategy, especially in an environment where traditional sale processes and IPO markets remain inconsistent.

The data shows continuation vehicles represented just 5% of global sponsor backed exit volume in both 2020 and 2021. That figure then climbed to 7% in 2022, before accelerating sharply to 12% in 2023 and 13% in 2024. In only four years, continuation vehicles more than doubled their share of sponsor backed exits. That level of growth signals far more than cyclical demand. It suggests permanent behavioral change across sponsors, LPs, and secondary buyers.

For private equity firms, continuation vehicles are no longer merely defensive liquidity tools. They are now active portfolio management instruments that allow GPs to hold prized assets longer, generate partial liquidity, and reset ownership structures without surrendering upside. As exit markets remain selective, this share of volume could continue rising, particularly among high quality assets that sponsors are reluctant to sell outright.

Detailed Analysis

Market share has more than doubled

Growth from 5% in 2020 to 13% in 2024 reflects one of the fastest expanding segments in private equity exits.Acceleration began after 2022

The jump from 7% to 12% in one year suggests adoption accelerated as financing markets tightened and M&A slowed.Continuation vehicles are now mainstream

At 13% of sponsor backed exit volume, the structure is no longer fringe or occasional.Sponsors prefer holding winners longer

Many GPs use these vehicles to retain top performing assets beyond the original fund life.Traditional exits remain challenged

Limited IPO windows, valuation gaps, and slower strategic M&A have created demand for alternative monetization routes.LP behavior has evolved

Investors are increasingly willing to choose between liquidity today or rolling into future upside.Secondary capital is fueling expansion

Dedicated secondaries funds and institutional buyers have provided the capital base needed to scale the market.Quality bias likely exists

Stronger assets are more likely to enter continuation vehicles, while weaker companies still face harder sale processes.Governance scrutiny will rise with scale

As volumes grow, pricing fairness, conflicts management, and process transparency become even more important.Strategic implication for GPs

Future exit planning may begin with multiple pathways, where continuation vehicles sit beside sale and IPO options from day one.

Bottom line

Continuation vehicles are no longer the backup plan. They are becoming part of the primary exit playbook.

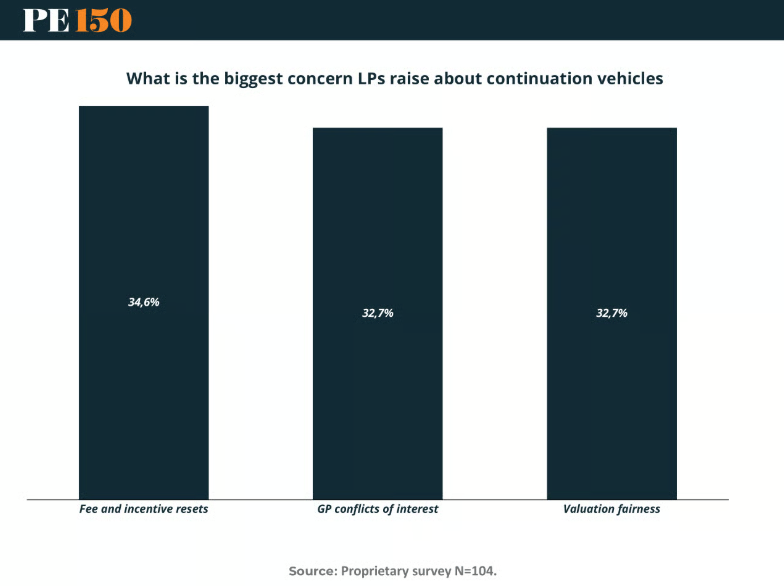

Trust, Not Structure, Is the Real Constraint on Continuation Vehicle Growth

Continuation vehicles are often discussed as innovative liquidity tools, but this chart highlights a more important reality: the biggest barriers to adoption are not mechanical, they are relational. LP hesitation is driven less by whether the structure works and more by whether the process feels fair. As continuation vehicles scale, trust has become the real currency of the market.

The survey results are strikingly balanced. 34.6% of respondents cite fee and incentive resets as their biggest concern, making it the leading issue by a narrow margin. 32.7% point to GP conflicts of interest, while another 32.7% identify valuation fairness as the primary concern. No single category dominates, which suggests LP skepticism is broad based rather than isolated to one technical issue.

For sponsors, the implication is clear. Raising capital for continuation vehicles is no longer just about asset quality or transaction execution. It increasingly depends on governance design, economics alignment, and independent credibility. The managers that institutionalize transparency and fairness will have a significant competitive edge as the market matures.

Detailed Analysis

Fees rank as the top concern

With 34.6% selecting fee and incentive resets, LPs are closely scrutinizing whether managers are being paid twice on the same asset.Conflicts remain front and center

32.7% worry about GPs acting as both seller and buyer in the same transaction.Valuation fairness is equally important

Another 32.7% fear assets may be transferred at prices that favor one party over another.No issue is materially smaller than the others

The narrow spread between responses suggests LP concerns are multidimensional.Economic alignment matters more than ever

Investors want clear evidence that continuation vehicles improve outcomes for all stakeholders, not only sponsors.Independent processes can unlock trust

Third party fairness opinions, competitive bidding, and LP advisory committee oversight can reduce friction.Repeat sponsors face higher scrutiny

Managers launching multiple vehicles may be judged more heavily on consistency and governance history.Sophisticated LPs are becoming more selective

Many institutions support the strategy in principle but reject poorly structured transactions.Future fundraising may bifurcate

Top tier managers with transparent processes may see strong demand, while weaker operators struggle.Strategic implication for GPs

The next generation of continuation vehicles must be designed as governance products, not just liquidity products.

Bottom line

LP resistance is not anti-continuation vehicle. It is anti misalignment.

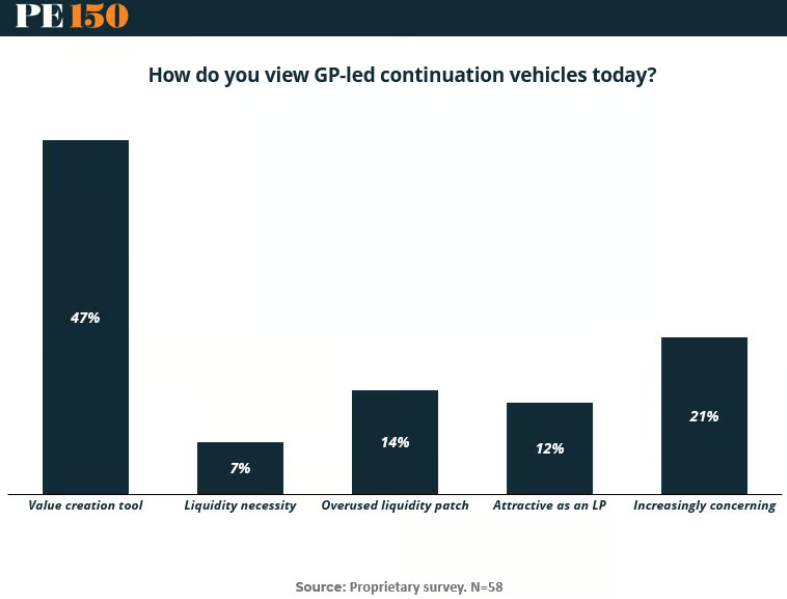

From Skepticism to Strategy: Continuation Vehicles Have Entered the Mainstream

This chart reveals how dramatically market perception has evolved. GP led continuation vehicles were once viewed primarily as emergency solutions used when sponsors could not exit assets through traditional channels. Today, respondents increasingly recognize them as legitimate strategic tools capable of extending ownership in strong companies, creating liquidity, and preserving upside.

The clearest signal is that 47% of respondents now view continuation vehicles as a value creation tool, making it the largest category by a wide margin. By contrast, only 7% still see them mainly as a liquidity necessity. However, skepticism has not disappeared. 21% describe them as increasingly concerning, while 14% view them as an overused liquidity patch. Another 12% consider them attractive as an LP, suggesting growing investor openness to participating in these transactions.

The broader takeaway is that continuation vehicles are moving through the classic lifecycle of financial innovation. They have shifted from niche workaround to accepted strategy, but rapid adoption has introduced new questions around discipline, quality control, and governance. The market now accepts the concept, but it is becoming more selective about execution.

Detailed Analysis

Value creation is now the dominant narrative

With 47% selecting this category, respondents increasingly believe continuation vehicles can enhance returns rather than simply solve liquidity problems.Legacy stigma is fading

Only 7% still classify them primarily as a liquidity necessity, indicating a major reputational shift.Concern remains meaningful

21% saying increasingly concerning shows that growth has also triggered caution.Signs of market saturation are emerging

14% labeling them an overused liquidity patch suggests some investors believe sponsors may be relying on the structure too frequently.LP appetite is developing

12% viewing them as attractive as an LP indicates investors are beginning to see these deals as investment opportunities, not just exit events.Execution quality now matters more than structure

Since the concept is more accepted, differentiation will come from pricing, governance, and asset quality.Top tier sponsors likely benefit most

Established managers with premium assets can position vehicles as strategic hold solutions rather than forced transactions.Weaker sponsors may face skepticism

Managers using continuation vehicles to delay difficult exits may reinforce negative perceptions.The market is entering phase two

Early growth was about adoption. The next phase will be about standards, discipline, and repeatability.Strategic implication for LPs

Investors should evaluate continuation vehicles case by case, separating high quality asset extensions from cosmetic liquidity engineering.

Bottom line

Continuation vehicles have won acceptance, but not unconditional trust.

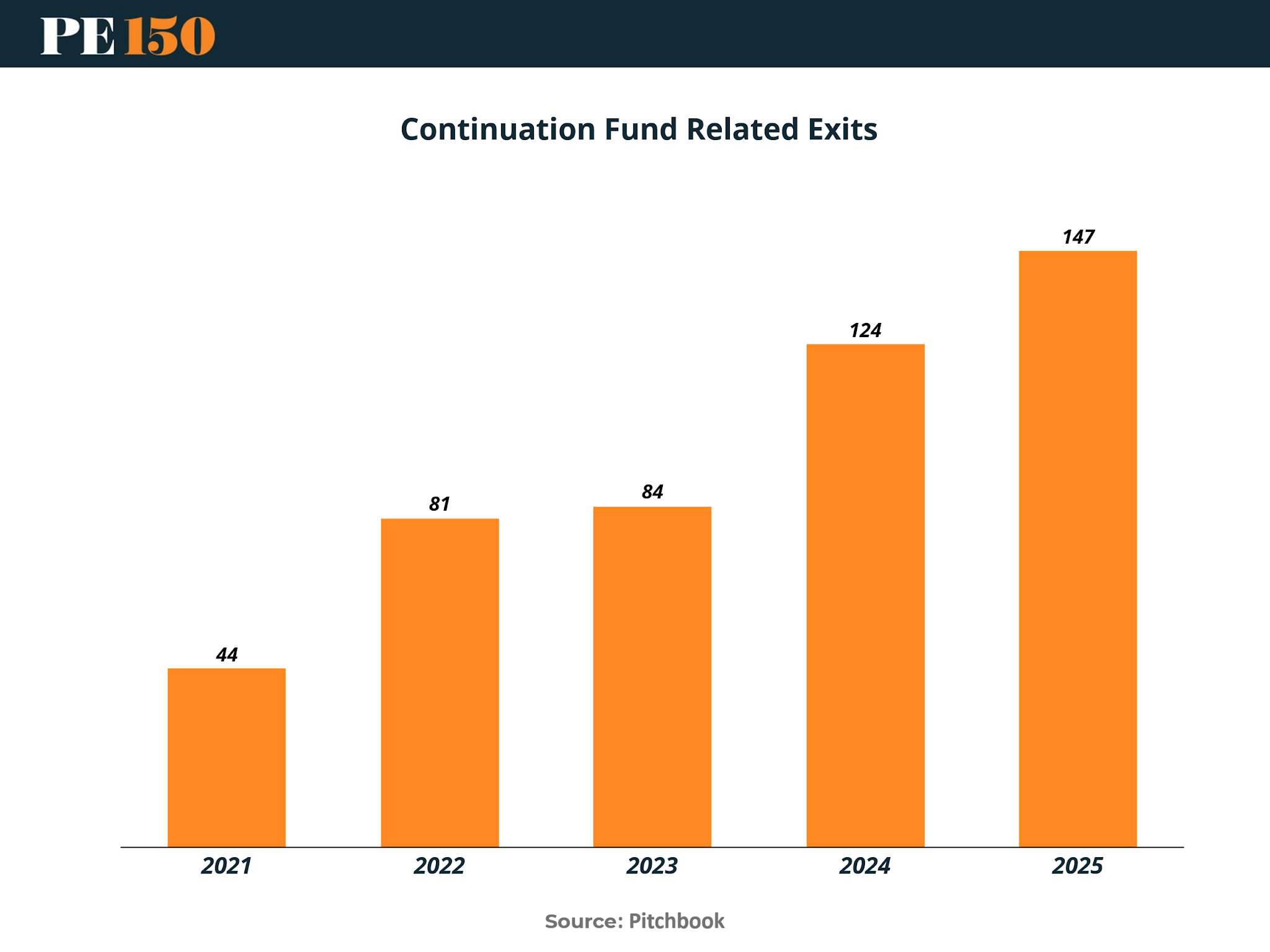

The Exit Valve Is Now a Market: Continuation Funds Are Scaling at Speed

This chart shows how quickly continuation funds have evolved from a specialized transaction type into a meaningful channel for private equity exits. What was once used selectively for exceptional assets is now becoming a repeatable mechanism for sponsors seeking liquidity, longer hold periods, and control over timing in an uncertain exit environment.

The numbers tell a compelling story. Continuation fund related exits rose from 44 in 2021 to 81 in 2022, then edged higher to 84 in 2023 before accelerating sharply to 124 in 2024 and 147 in 2025. Over the full period, transaction volume more than tripled. The brief moderation in 2023 now appears less like a slowdown and more like a pause before the next growth leg.

This trend reflects structural demand on both sides of the market. Sponsors need alternatives to delayed IPOs and selective M&A buyers, while secondary investors are increasingly willing to fund concentrated, high conviction deals. Continuation funds are no longer a temporary response to market stress. They are becoming embedded infrastructure within the private equity ecosystem.

Detailed Analysis

Transaction volume has more than tripled

Growth from 44 exits in 2021 to 147 in 2025 signals rapid institutionalization of the strategy.Momentum remained resilient despite 2023 pause

The modest move from 81 to 84 suggests demand held steady before reaccelerating.2024 marked a breakout year

Jumping to 124 exits indicates broader adoption by sponsors and buyers.2025 confirms durability

Reaching 147 suggests continuation funds are sustaining momentum rather than peaking.Exit bottlenecks are driving usage

Limited IPO windows and cautious acquirers continue to push sponsors toward alternative monetization routes.High quality assets are staying private longer

Many sponsors prefer transferring strong businesses into new vehicles rather than selling prematurely.Secondary capital has matured significantly

Dedicated investors now have the scale and expertise to underwrite single asset and concentrated continuation deals.Fund life management is changing

Continuation funds allow GPs to align hold periods with asset potential instead of arbitrary fund timelines.Competitive advantage may shift to process quality

As volume rises, governance, pricing transparency, and LP communication will separate leading sponsors from the rest.LPs face a strategic choice

Sell for liquidity today or roll into a new vehicle for additional upside.

Bottom line

Continuation funds have moved beyond niche status. They are now a core exit lane for modern private equity.

Conclusion

The data suggests continuation vehicles are no longer an emerging trend. They are now a structural component of the private equity ecosystem. Exit volumes tied to these vehicles continue to rise, investor perception has become more constructive, and sponsors increasingly view them as tools for value creation rather than emergency liquidity solutions.

At the same time, enthusiasm is clearly measured. LPs remain cautious about over allocation, and concerns around economics, conflicts, and pricing remain central. That combination of growing adoption and persistent skepticism is healthy. It signals a market maturing through discipline rather than unchecked expansion.

Looking ahead, continuation vehicles are likely to remain a permanent part of the exit toolkit, sitting alongside strategic sales, sponsor to sponsor transactions, and public listings. The firms that succeed will not simply be those with the best assets, but those that can structure transactions with transparency, fairness, and clear investor alignment.

In private equity’s next chapter, continuation vehicles may prove to be more than an alternative exit route. They may become the model for how ownership duration, liquidity, and value creation are balanced in a more complex market.

Sources & References

PE150. Continuation vehicles value creation tool or liquidity patch. https://www.pe150.com/p/continuation-vehicles-value-creation-tool-or-liquidity-patch

PE150. Continuation funds hit a participation ceiling. https://www.pe150.com/p/continuation-funds-hit-a-participation-ceiling

PE150. Continuation vehicles LP Skepticism.https://www.pe150.com/p/continuation-vehicles-lp-skepticism-is-about-structure-not-strategy

HIG. Making sense of continuation vehicles.https://hig.com/news/making-sense-of-continuation-vehicles/

Kroll. Secondary Market Evolution.https://www.kroll.com/en/publications/transaction-opinions/secondary-market-evolution-continuation-funds-alternative-traditional-exits

Chronograph. The Rise of Continuation Funds.https://www.chronograph.pe/the-rise-of-continuation-funds-a-deep-dive/