- PE 150

- Posts

- 80% of Buyout Growth Comes from North America, Plus a £7.4B Deal

80% of Buyout Growth Comes from North America, Plus a £7.4B Deal

Breaking down the regional concentration of buyout expansion and the major transaction signaling continued momentum.

Good morning, ! Today we're covering LP skepticism around continuation funds, liquidity risks emerging in private credit, North America powering the global buyout rebound, and EQT’s £7.4B bet on UK water infrastructure.

Juniper Square breaks down why new fund formats are changing what best-in-class operations looks like for PE GPs — and why more firms are moving beyond fragmented tools and legacy service models toward a fund operations partner: one connected operating model that combines software, data, and embedded expertise to improve visibility, control, and investor experience. Read the full breakdown →

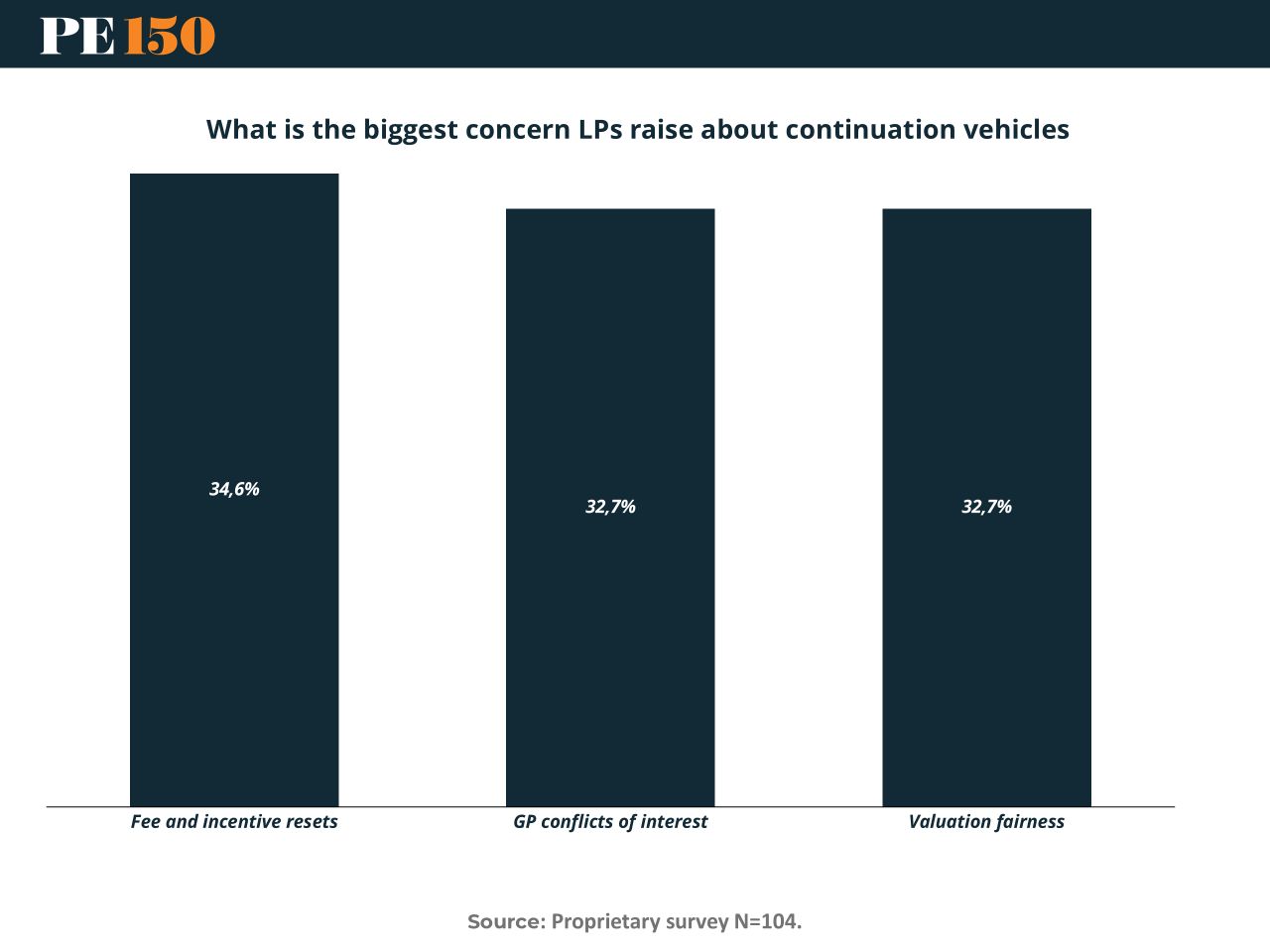

MICROSURVEY

LPs skepticism continues

In our proprietary survey of 104 private markets professionals, the concerns cluster tightly around three issues. 34.6% of respondents pointed to fee and incentive resets as the biggest red flag. Another 32.7% cited GP conflicts of interest, while 32.7% flagged valuation fairness.

The takeaway is revealing. LP skepticism is less about the existence of continuation vehicles and more about how economics and governance are structured. When a GP sells an asset from one fund to another vehicle it controls, three questions immediately surface. Are fees being reset in a way that benefits the manager more than the LP? Is the GP incentivized to sell or to hold? And most critically, is the price truly market tested.

For sponsors, the implication is clear. The continuation vehicle market will keep expanding as exit timelines stretch, but credibility will hinge on process discipline. Independent fairness opinions, competitive buyer participation, and transparent fee terms are no longer optional. They are the price of LP trust. (More)

PRIVATE CREDIT CORNER

Liquidity Mismatch Comes Into Focus

Private credit stress is rising in headlines, but the data tells a more nuanced story. Default rates in the Morningstar LSTA Leveraged Loan Index remain contained relative to past cycles. As of early 2026, the trailing twelve month default rate for below investment grade loans sits near 5.5%, compared with 3.4% in comparable corporate bonds. The chart reinforces the point. Defaults today are well below the 2009 peak above 10% and far from systemic territory.

The pressure is appearing elsewhere. About 21% of Software and Services loans now trade below 80 cents on the dollar, and roughly $25 billion of speculative rated software debt sits in that discounted bucket. That pricing reflects investor caution around refinancing risk rather than widespread payment failures.

Private credit risk right now is less about borrower collapse and more about liquidity structure. Loans typically mature in 3 to 7 years, yet many retail oriented funds offer frequent redemption windows. In a $2 trillion market that mismatch matters. For sponsors and allocators the playbook is clear. Focus on senior secured loans, diversify sector exposure, and avoid vehicles promising liquidity that the underlying assets cannot realistically deliver. (More)

PRESENTED BY JUNIPER SQUARE

New fund formats call for a new operating model: fund operations partner.

Our report on the rise of new fund formats shows a clear shift: operating cadence is increasing, investor workflows are getting more complex, and expectations are moving toward to “always-on.”

That’s why leading PE firms are shifting to a fund operations partner model: one system of record + embedded expertise to run fundraising, investor operations, reporting, and administration with consistent data.

Juniper Square combines purpose-built software + expert fund administration services into a single connected operating model, delivering clearer visibility, fewer failure points, and a modern investor experience.

Read the full breakdown in the report.

Supporting our sponsors supports our free newsletters. Please support our sponsors!

REGIONAL FOCUS

North America Powers the Buyout Rebound

The global buyout recovery is underway — but it has a clear geographic leader.

Global buyout deal value is projected to rise from roughly $600B in 2024 to nearly $900B in 2025, signaling a meaningful rebound after two subdued years. Yet the growth is heavily concentrated: North America accounts for roughly 80% of the increase.

The driver? The return of megadeals valued at $10B+. As financing markets stabilize and private credit liquidity expands, large-cap sponsors are once again executing complex, multi-billion-dollar buyouts.

By comparison, Europe contributes about 8% of global growth, while Asia-Pacific adds roughly 9%, reflecting more gradual recoveries.

The takeaway: the global rebound isn’t broad-based yet — it’s megadeal-led, with North America firmly at the center of private equity’s recovery. (More)

DEAL OF THE WEEK

EQT Makes a £7.4B Bet on UK Water

EQT has agreed to acquire a 42% stake in Kelda Holdings, the parent company of Yorkshire Water, marking one of the largest recent investments in Britain’s embattled water sector. Singapore’s sovereign wealth fund GIC will also hold 42%, while Australia’s TCorp increases its stake to 16%.

The timing is notable. UK water utilities are under heavy political and regulatory scrutiny as ageing infrastructure, sewage spills, and rising debt levels spark public backlash. Yorkshire Water alone carries £7.4B in net debt against a regulatory capital value of roughly £10B, highlighting the financial pressure across the sector.

EQT will also support the company’s balance sheet by contributing to a ~£600M loan repayment due before March 2027, injecting fresh equity rather than restructuring debt.

Strategically, the move underscores why infrastructure investors still favor regulated utilities. Yorkshire Water serves 5.5M people and 139,000 businesses in northern England, making water services a stable, long duration cash flow asset despite political noise.

The bigger message: when sectors face scrutiny and leverage stress, private capital often steps in. Infrastructure specialists like EQT are betting that operational improvements and fresh capital can turn public pressure into long term value creation. (More)

FUND OPS - Presented by Juniper Square

Continuation Funds: The Liquidity Engineering Era

Private equity didn’t invent continuation funds because they were elegant. It invented them because exits stopped working. Global PE exits peaked at $1.7T in 2021, then fell to $808B in 2022 and $751B in 2023, leaving a backlog of mature assets and LPs waiting for distributions. With IPO markets selective and strategic buyers disciplined on price, sponsors needed another mechanism to generate liquidity without selling at compressed valuations.

The shift is visible in exit data. Continuation vehicle volume rose from $26B in 2020 to $63B in 2024, with $41B already completed in H1 2025. More importantly, their role in the exit ecosystem has expanded rapidly. These structures represented just 5% of sponsor backed exits in 2020, but now account for 19% in H1 2025.

Continuation funds are no longer a niche secondaries tool. They are becoming a standard exit pathway.

Capital formation confirms the institutionalization. Fundraising increased from less than $1B in 2015 to $52.9B in 2025, while the number of vehicles scaled to roughly 100 funds annually.

Fund Ops Insight:

Continuation vehicles are quietly reshaping the operating model of private equity firms. Instead of managing a simple lifecycle of raise → deploy → exit, GPs are now managing asset transfers across vehicles. That introduces new operational demands around fairness opinions, valuation governance, LP elections, and transaction conflicts.

The implication is clear. In a world of slower exits and longer holding periods, fund operations has become the infrastructure that enables liquidity engineering.

Get the new Juniper Square report to see why new fund formats are changing what best-in-class GP operations looks like. Get the report →

Supporting our sponsors supports our free newsletters. Please support our sponsors!

“In the short run, the market is a voting machine, but in the long run, it is a weighing machine.”

Benjamin Graham