- PE 150

- Posts

- 58% of LPs Cap Continuation Funds—Is the Trade Getting Crowded?

58% of LPs Cap Continuation Funds—Is the Trade Getting Crowded?

Demand Is There, But Discipline Is Rising

Good morning, ! Today we're covering continuation funds hitting LP allocation limits, private credit’s illiquidity stress test, LATAM’s fundraising consolidation toward established GPs, and the rise of complex capital-structure deals reshaping traditional buyouts.

Juniper Square shares how Avanath Capital Management modernized operations as fund complexity increased — replacing fragmented processes with a more connected operating model across fund accounting, reporting, and investor servicing. See how one GP reduced friction, improved visibility, and strengthened the investor experience with infrastructure built to scale. Read the Avanath story →

MICROSURVEY

Continuation Funds Hit a Participation Ceiling

Continuation vehicles are no longer a question of adoption. They are a question of limits.

The data is telling. 58% of LPs cap exposure at under 10% of their portfolio, while only 22% are willing to allocate more than 25% . That is not resistance. It is controlled acceptance.

The shift matters. GPs increasingly rely on continuation funds to manufacture liquidity in a market where exits remain inconsistent. But LP behavior suggests these vehicles are being treated as tactical tools, not strategic allocations. In other words, LPs will play, but they will not overplay.

This creates a subtle but important constraint. As more assets are funneled into GP led processes, competition for LP capital inside continuation funds will intensify. Not every deal will clear, and average assets will struggle to get done at attractive pricing.

Bottom line: continuation funds are scaling fast, but LP appetite is not infinite. The winners will be managers who bring truly differentiated assets. Everyone else risks discovering that liquidity solutions still require buyers. (More)

PRIVATE CREDIT CORNER

Private Credit: Illiquidity as Feature, Not Flaw (yet)

Recent headlines have cast private credit as a potential source of systemic risk, citing redemption gates, opacity, and parallels to past crises. While these concerns are not unfounded, they often misinterpret the structural design of the asset class. Private credit is built on long-duration capital funding long-duration assets, making illiquidity an intentional feature, not a weakness. Redemption limits, frequently portrayed as signs of distress, are in fact risk management mechanisms that prevent forced asset sales and preserve portfolio value.

The real risk lies in liquidity bottlenecks if investors simultaneously seek withdrawals, particularly in semi-liquid structures. However, unlike banks, private credit does not rely on short-term funding mismatches, reducing the likelihood of classic run dynamics. Moreover, growing diversification—especially through asset-backed finance—is improving resilience. (More)

PRESENTED BY JUNIPER SQUARE

How one GP modernized operations for a more complex fund structure

As firms expand into new fund structures, increase investor counts, and face heightened reporting expectations, the operating model either scales with them or becomes the constraint.

Avanath Capital Management reached that inflection point. As their platform grew, so did the complexity across fund accounting, reporting, and investor servicing. Rather than adding more manual processes or stitching together additional systems, they modernized their infrastructure with Juniper Square.

See how Avanath:

Unified fund and investor data on a single platform

Reduced reconciliation and reporting friction

Increased visibility across teams

Strengthened the investor experience through connected operations

The outcome wasn’t just efficiency; it was operational resilience.

Supporting our sponsors supports our free newsletters. Please support our sponsors!

REGIONAL FOCUS

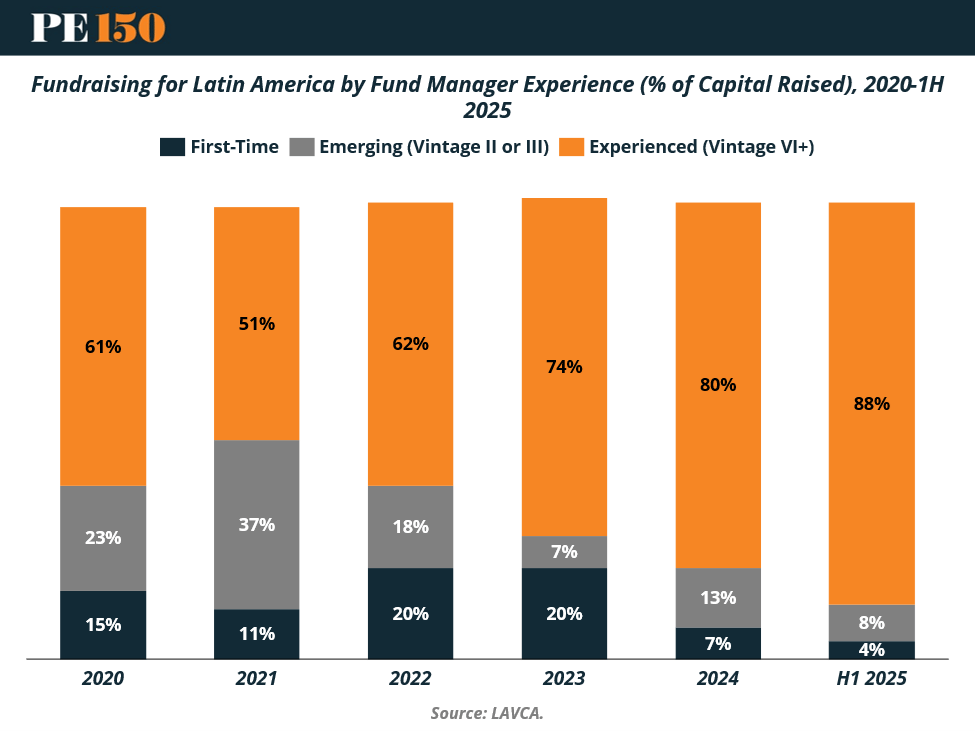

LATAM’s Fundraising Funnel Narrows

In Latin America, LP capital is increasingly flowing to those who’ve “been there, done that.”

From 2020 to 1H 2025, Experienced GPs (Vintage VI+) saw their share of fundraising climb from 61% to 88%—a decisive shift toward track record over potential.

Emerging managers briefly surged in 2021 (37%), but have since fallen to single digits, while First-Time funds now capture just ~4%.

Why it matters: A higher-rate environment has made risk tolerance scarce. LPs are doubling down on known operators, prioritizing execution certainty and re-ups over new relationships.

The bottom line: The market is diversifying by strategy, but consolidating by manager—raising the bar for anyone outside the incumbent circle. (More)

DEAL OF THE WEEK

Apollo’s $3.7B Japan Bet Is Really a Balance Sheet Reset

Apollo Global Management is acquiring Nippon Sheet Glass in a deal valued at approximately $3.7 billion, marking its largest private equity investment in Japan to date.

This is not a traditional buyout. It is a capital structure intervention. Apollo is injecting roughly $1.04 billion of new equity, while lenders are converting about ¥140 billion of debt into equity to stabilize a balance sheet carrying over ¥570 billion in total debt. The transaction effectively deleverages the company while resetting ownership and positioning it for growth.

The underlying bet is twofold. First, that operational improvement plus balance sheet repair can unlock value in a structurally sound but financially constrained business. Second, that end markets such as architectural glass, automotive glazing, and solar will provide secular tailwinds.

Zoom out, and the deal says more about Japan than glass. Corporate governance reforms and a growing willingness to restructure have turned Japan into one of the few markets seeing both deal volume and value expansion. For sponsors, it is becoming a playground for complex, lender driven transactions rather than clean auctions.

Why it matters: This is private equity leaning into distress without calling it distress. Expect more deals where capital solutions replace traditional buyouts, especially in markets where leverage has quietly become the real asset for sale. (More)

Fund Ops Corner

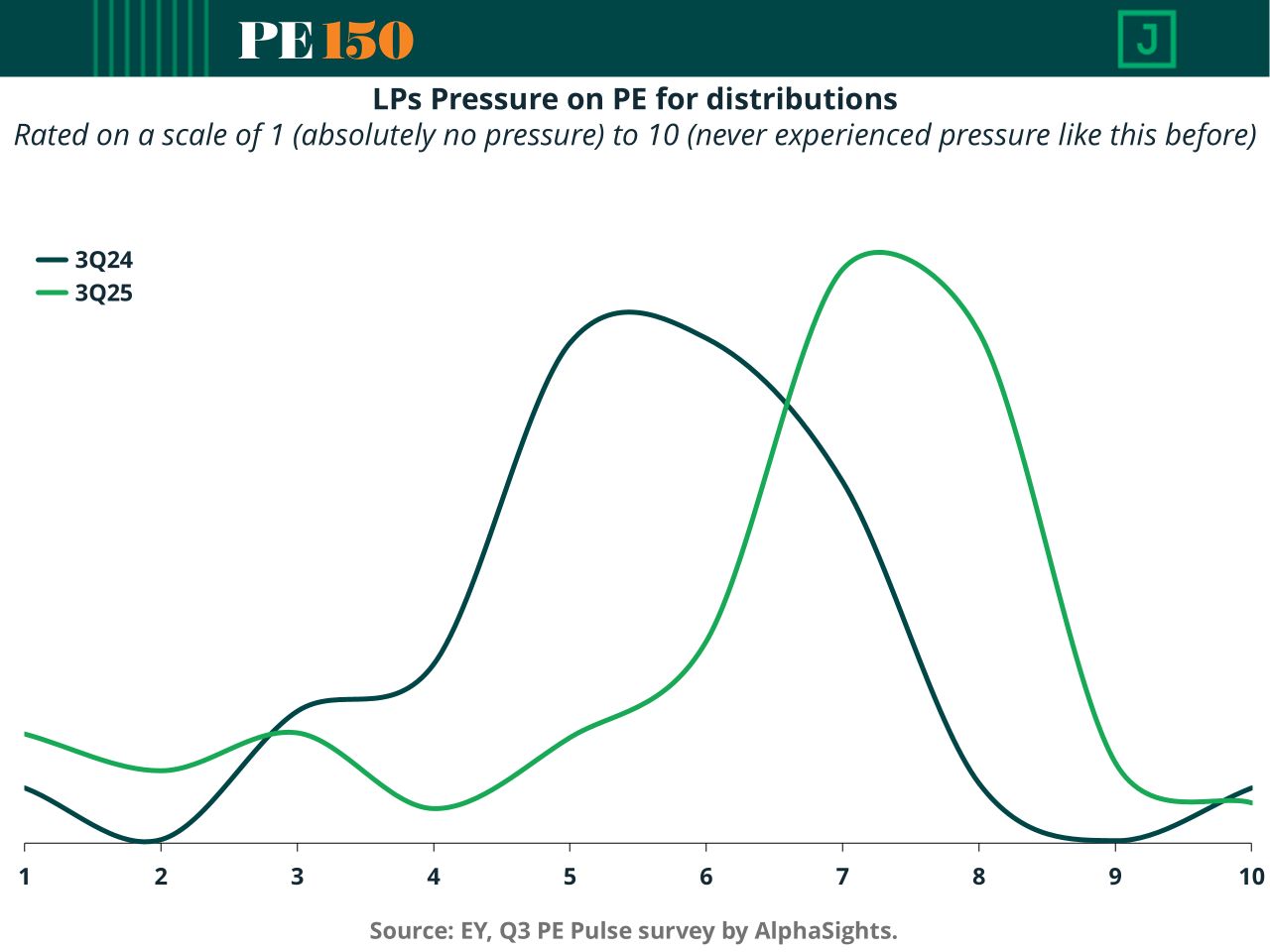

Liquidity Pressure Is Forcing Operational Reinvention

Private equity is still working through a structural exit bottleneck. Exit value peaked at $1.7T in 2021 and remains roughly half that level despite a modest recovery. The result: a buildup of aging assets and delayed realizations, putting pressure on DPI delivery.

At the same time, valuation gaps persist. Buyers are underwriting with higher discount rates, while GPs are anchored to prior entry multiples—creating friction across traditional exit routes.

This is colliding with rising LP liquidity pressure. Sentiment has shifted toward the 6–8 range, signaling a clear demand for distributions. The denominator effect and muted cash flows mean LPs need capital returned—not just paper gains.

What This Means for Fund Ops

GPs are increasingly engineering liquidity, not waiting for it. Continuation vehicles are now a core tool—allowing partial exits while retaining upside.

But operationally, this raises the bar:

Full re-underwriting of assets (as if new deals)

Enhanced valuation governance and conflict management

More complex LP elections and rollover mechanics

Greater coordination across IR, legal, and fund accounting

Bottom Line

Liquidity constraints are turning fund operations into a strategic function. With exits no longer binary, GPs must actively manage timing, structure, and capital recycling.

Read the Avanath story to see how one GP modernized operations for a more complex fund structure. Read the story →

Supporting our sponsors supports our free newsletters. Please support our sponsors!

"Success is walking from failure to failure with no loss of enthusiasm."

Winston Churchill