- PE 150

- Pages

- Private Credit Archive

Private Credit Section

1/15/2025

🏦 Private Credit Corner

Private Credit: Europe focus

Private credit in Europe has undergone a dramatic transformation over the past few years, emerging as a dominant force in transaction financing. Between 2020 and 2023, the share of transactions financed by private credit more than doubled, rising from 27% to 56%. This surge was driven by the inability of broadly syndicated markets to function effectively during periods of heightened economic uncertainty. Private credit, with its certainty of financing and bespoke structures, became the go-to solution for leveraged buyouts, bolt-on acquisitions, and refinancings. Borrowers found assurance in private credit’s ability to deliver financing at predictable terms, particularly in volatile market conditions where bank-arranged financing often posed risks of unexpected costs. Flexible lending structures further enhanced its appeal, allowing private equity sponsors to focus on value creation and operational improvements rather than simply leveraging assets

The resurgence of syndicated markets does not diminish private credit's newfound prominence. Instead, it highlights the complementary roles of public and private credit markets. While lower costs may draw some issuers back to syndicated solutions, private credit remains a critical tool for borrowers seeking tailored financing solutions. Direct lending offers the flexibility to structure deals that align with strategic growth plans, including delayed-draw features, deferred interest payments, and currency-matched financing. As European markets adapt to a new normal, private credit’s ability to provide certainty and customization ensures it will remain indispensable, thriving alongside the revived syndicated market to sustain the buyout industry and beyond.

1/8/2025

🏦 Private Credit Corner

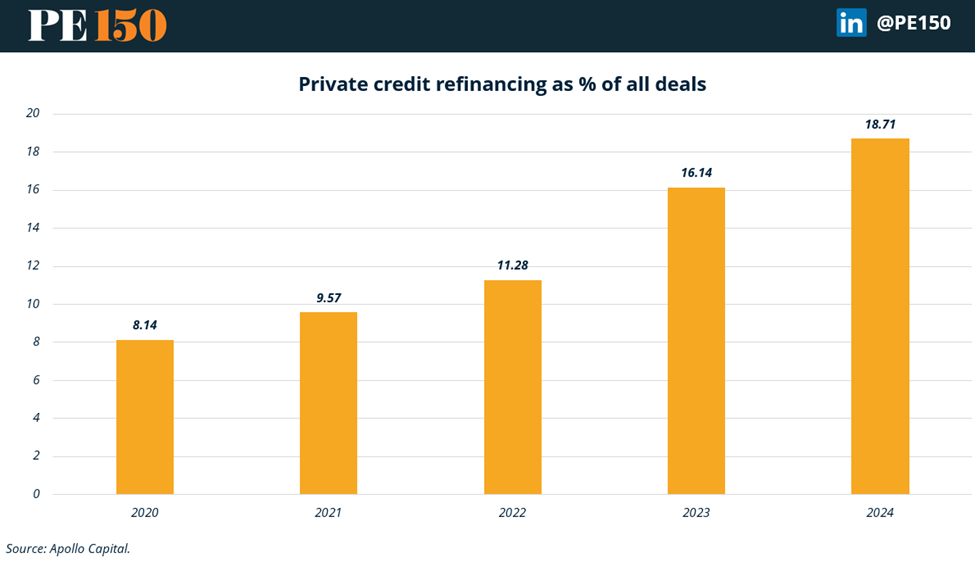

Private Credit Refinancing on the Rise

The growth of private credit refinancing is reshaping the private credit landscape, reflecting its increasing importance as a financing tool. In 2020, refinancing accounted for 8.14% of all private credit deals, but by 2024, this share is projected to climb to an impressive 18.71%,more than doubling in just four years. This rapid growth underscores the evolving dynamics in the financial ecosystem, as companies turn to private credit to manage looming debt maturities and restructure their obligations amid tightening traditional lending conditions. With private credit offering greater flexibility and speed compared to bank loans, it has become a lifeline for borrowers navigating uncertain macroeconomic conditions, including rising interest rates and constrained liquidity.

This trend highlights the unique role private credit plays in the modern financial system, particularly as traditional credit markets face challenges. Refinancing through private credit enables businesses to optimize their capital structures and maintain financial stability without the red tape often associated with other financing avenues. For private credit investors, the rising demand for refinancing offers compelling opportunities to deploy capital in lower-risk, interest-generating instruments. As this trend accelerates, private credit refinancing is poised to remain a dominant theme into 2025, further solidifying the asset class as a critical tool for corporate borrowers and a key pillar of private markets.

12/20/2024

🏦 Private Credit Corner

Private Credit Market Size and Regional Analysis

The private credit market has surged to $2.1 trillion in 2023, marking a significant leap from $1.84 trillion in 2022. This growth represents a 15% compound annual growth rate (CAGR) over the past decade, driven by demand for alternative financing options that offer flexible structures and attractive yields. North America remains the largest regional market, reaching $1.25 trillion in 2023—roughly 60% of the global total—while European private credit stands at $0.27 trillion, showing a 17% CAGR. The sector's “dry powder” reserves, or undeployed capital, have also grown to $0.49 trillion, reflecting investors’ readiness to seize new opportunities amid rising interest rates and tightening liquidity.

The private credit landscape showcases an evolving risk-reward balance, particularly when comparing average annual credit losses of 0.9% to those of other credit instruments like high-yield bonds (1.47%). Within this market, secured loans dominate deal types, accounting for 55.8% of transactions across various sectors, including software and healthcare. Meanwhile, fund investments remain largely segmented, with public pension funds contributing 19% of total commitments, leaving 35% of sources unidentified. Lastly, annual default rates for sponsored and non-sponsored leveraged loans have declined to 2.3% and 7.8%, respectively, underscoring improved performance in recent years.